Uncategorized

Will Argentinian President Milei’s Crypto ‘Fiasco’ be a Deathblow for Memecoin Craze?

The latest frenzy that started with U.S. President Donald Trump’s TRUMP memecoin launch and saw traders making and losing millions within minutes, might have finally come crashing down with the LIBRA token fiasco.

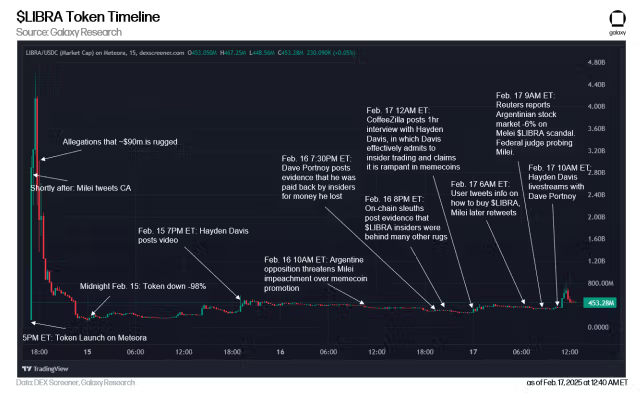

LIBRA, a Solana-based project that President of Argentina Javier Milei tweeted about on Feb. 14, saw its market cap rise as high as $4.5 billion and then fall more than 80% within a couple of hours as insiders cashed out, leaving many bag holders with massive losses.

The story became an international and political incident over the weekend when in the last couple of days, Milei deleted his original tweet, denied his endorsement and accused the political opposition of mischief. This eventually led to talks of his impeachment and created uncertainty in the Argentinian stock market. Then came an explosive twist to the story.

On Tuesday, CoinDesk broke the news that a key player behind the LIBRA token had bragged about buying access to Argentine President Javier Milei’s inner circle months before the memecoin’s scandalous launch and crash.

Although these kinds of kerfuffle for a memecoin are not unusual, how this happened and what followed after the apparent «rug pull» highlighted the risk of unchecked crypto trading and the potential for a reputational hit for the memecoin sector as a whole.

«The LIBRA episode represents what is a potential point of oversaturation for the memecoin space,» said Toronto-based crypto platform FRNT Financial. «At this point, the novelty of new projects, after TRUMP and MELANIA, and now LIBRA, has largely worn off.»

«Additionally, the reputational consequences for these assets may be significant. Having said that, it appears that this episode is likely to continue playing out as new details emerge. At this point, memecoins are synonymous with ‘pump and dump’ schemes,» FRNT contended.

This incident, along with other memecoin-related events that led to many retail traders losing money, may nudge the community to make more of an effort to police itself.

«The entire $LIBRA memecoin fiasco over the weekend should serve as a reminder that all of us in the DeFi community have a responsibility to make this space safer for users,» said Chris Chung, founder of Solana-based swap platform Titan.

How the ‘fiasco’ happened

The whole Milei and LIBRA episode played out within the span of a few days, starting on Feb. 14.

As explained by Galaxy Research’s Alex Thorn, the token launched on that fateful day on a Solana-based DeX Meteora, with Milei’s initial post (now deleted) on social media platform X saying that the aim of the token was to help the growth of the Argentinian economy — a big endorsement for a memecoin.

Once the token price reached its peak of $4.4 billion within hours, the insiders started dumping their holdings immediately, making nearly $100 million, according to onchain analysts.

The next day, Milei deleted his original post, sending a shockwave within the memecoin community, that saw many similar tokens, such as TRUMP, MILANIA, and others, sell out fast. Meanwhile, Solana, the blockchain the token was built on, also saw its native token, SOL, fall.

In his new post, Milei claimed he wasn’t aware of the details of the project and accused the political opposition of mischief, making the situation a game of politics. By that time, the token had erased around $4.5 billion of retail capital in seven hours. Currently, the market cap sits around just above half a million, according to CoinMarketCap data.

The same day, names of a few key opinion leaders (KOL) came up, including Barstool’s Dave Portnoy, Threadguy, Hayden Davis and Faze Banks, who were involved in one way or another with the project. Portnoy said he was an early investor and was refunded his money, further spreading the controversy that insiders benefitted from the LIBRA fiasco. Davis, meanwhile, revealed that he was behind both the LIBRA and MELANIA memecoins and said the Argentinian token incident was «not a rug pull,» rather «It’s just a plan gone miserably wrong.»

The next day, the Argentinian opposition threatened Milei with impeachment over the incident. On Feb. 17, Ben Chow, co-founder of DeX Meteora, where LIBRA had launched, resigned over the controversy. Chow was also a co-founder of Solana-based trading aggregator Jupiter. The same day Argentina’s stock market collapsed almost 6% on a report of a probe on Milei.

Read more: LIBRA Apparent Rug Pull Is Latest ‘Sordid Episode’ Emerging From Solana’s Memecoin Complex: Galaxy

On Feb. 18, CoinDesk broke the news that Davis claimed in text messages that he could «control» Milei because of payments he had been making to Karina Milei, a powerful figure in Milei’s government, and the president’s sister.

‘Setback for crypto’

What will happen to Milei and all the involved parties is still unknown. However, if FTX’s spectacular blowout is anything to go by, there might still be a lot more to untangle in this story.

What it does highlight is that the memecoin drama that has become a game of split-second profit and losses, in this cycle, might be at a crossroads. As institutional investors are betting big on bitcoin and ether with the launch of exchange-traded funds, making those assets more TradFi friendly and stable, the memecoin sector has stuck out as the ugly duckling of the crypto space, and this incident may sour retail participation.

«Overall, this entire story is a real setback for the crypto space,» Chung said. «If we want to attract new retail users, this is not the way to do it.»

Welcome back to TechCrunch Mobility, your hub for all things “future of transportation.”

Over the last two years, Nvidia has used its ballooning fortunes to invest in over 100 AI startups. Here are the giant semiconductor’s largest investments.

Cerca is a dating app that sets users up with mutual friends.

Elon Musk vs. the regulators

Nvidia’s AI empire: A look at its top startup investments

Dating app Cerca will show how Gen Z really dates at TechCrunch Disrupt 2025

-

Business12 месяцев ago

Business12 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion12 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment12 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment12 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment12 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Uncategorized4 месяца ago

Uncategorized4 месяца agoRobinhood Launches Micro Bitcoin, Solana and XRP Futures Contracts

-

Business12 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment12 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton