Uncategorized

Tornado of Administrative Overreach: Challenging Sanctions of Crypto Mixing Services

Cryptocurrency transactions are often anonymous, but they’re not private. In fact, they’re quite public. Anyone with the right technical know-how can see every transaction ever made on most publicly accessible blockchains.

This radical transparency and traceability has made it easier (contrary to popular belief) for law enforcement to track stolen and laundered cryptocurrency across various transactions. But it has also made it easier for criminal crypto actors to trace certain transactions, and — by collecting enough data points — recognize the real-world identity of crypto users who would otherwise remain anonymous.

Dramatic stories abound about violent home invasions targeting those with large cryptocurrency holdings or hackers targeting those who donate to controversial causes. More mundanely, those who accept cryptocurrency as payment for goods or services might not want the person paying them to know their entire on-chain financial history with only a few clicks.

Recognizing these realities, crypto-mixing services sprung to life. The technical details can differ dramatically, but essentially these services act as intermediaries, mixing together crypto transactions to make them more difficult, if not impossible, to track. Some mixing services actually take custody of the cryptocurrency, mix the funds together, and then distribute them to pre-determined places. Others rely instead on smart contracts (pre-written computer code) to do this for them. Created in 2019, popular crypto-mixing service Tornado Cash falls into this latter category.

For the same reasons these services appeal to legitimate users (privacy and making transactions harder to track), they also appeal to criminals and hostile foreign state actors such as North Korea. Knowing this, the Treasury Department’s Office of Foreign Assets Control (OFAC) imposed sanctions that would prohibit “U.S. persons” from engaging in transactions with, or using, some of these mixing services, including Tornado Cash.

But does OFAC have the authority to do this, particularly when it comes to smart-contract-based services such as Tornado Cash?

In two similar lawsuits — one pending in the Fifth Circuit and one pending in the Eleventh Circuit — a series of plaintiffs are arguing that it does not, saying that OFAC’s decision involves “an unprecedented exercise of [its] authority.” To understand why, we need to back up and understand precisely what Congress has said.

For starters, it makes sense that Americans wouldn’t want criminals or foreign adversaries using the U.S. financial system to accomplish their nefarious goals. So, Congress empowered the president to use a panoply of broad economic tools to stop them from doing so. The president in turn delegated his authority to impose and exercise these economic sanctions to the Secretary of the Treasury who in turn delegated much of the responsibility to OFAC for implementing them.

As relevant here, Congress passed two laws that authorize the president and those to whom he has delegated authority, to act. The International Emergency Economic Powers Act (IEEPA) empowers the chief executive (who has delegated his authority all the way down to OFAC) to block “any property in which any foreign country or a national thereof has any interest” when certain other specified conditions are met. Another act, the North Korea Sanctions and Policy Enhancement Act, allows the president to sanction the “property and interest in property” of “any person” who engaged in specified conduct.

While national security concerns pervade the cases challenging OFAC’s actions, fundamentally the cases are about statutory interpretation. What do the terms “person,” “property,” and “interest in property” mean in plain English so that courts can decide whether Congress gave the President — and OFAC — the power to impose sanctions on Tornado Cash?

In the wake of the U.S. Supreme Court’s Loper Bright decision, courts must decide for themselves what these terms mean without giving deference to the agency’s interpretation.

Of course, the plaintiffs in these lawsuits argue that these aren’t obscure technical terms. And they argue that “text, precedent, and history” support their position that OFAC exceeded its authority in placing the Tornado Cash entity it designated on the sanctions list — largely because of how Tornado Cash operates and is structured.

They argue, essentially, that OFAC didn’t properly identify any person — which can include an entity (though they argue there isn’t one in this case) — didn’t properly identify any property because the open-source immutable smart contracts (computer code) at issue here aren’t capable of being owned, and didn’t properly identify any interest in property, as traditionally understood to mean a “legal or equitable claim to or right in property.”

In part, this stems from the fact that there’s confusion over what exactly constitutes “Tornado Cash.” While the government referred to an amalgamation of entities and individuals, the plaintiffs say that “[n]obody besides the government call these people ‘Tornado Cash’” and others instead typically use Tornado Cash to refer to the smart contracts underlying the mixing service.

Essentially, there’s the (Ethereum) blockchain on which the smart contracts run , the developers who initially programmed the smart contracts, the smart contracts themselves, and a decentralized autonomous organization (DAO) that has many members that vote and takes actions related to the smart contracts but that doesn’t own or control the smart contracts themselves since they are unchangeable open-source software code.

The plaintiffs say that by allowing OFAC to break free from the traditional widely accepted understanding of “person,” “property,” and “interest in property,” OFAC’s “sanctions authority would be nearly limitless.” The plaintiffs say that if OFAC’s sanctions are allowed to stand, “every American citizen may be prohibited from executing those lines of code to make political donations, start business ventures, or develop new software features.” They also make clear that OFAC “cannot ban Americans from transacting only with fellow Americans or with their own property,” yet they say that’s exactly what has happened here.

Both district courts considering these issues disagreed and found that OFAC had acted lawfully in imposing the sanctions. At a recent oral argument in the Fifth Circuit case, however, the appellate judges seemed skeptical. And the appellate judges in the Eleventh Circuit case asked tough questions too.

Due process and First Amendment concerns have been brought up in varying degrees in both cases. There’s also questions about what role, if any, the rule of lenity and the Major Questions Doctrine should play. And, even more to the point, there’s questions with larger implications for the crypto community such as whether a smart contract (computer code) can be a unilateral contract and whether a DAO standing alone can be thought of as an unincorporated association or even a general partnership with liability for some or all of its members.

With all of these lingering questions, one thing is clear: Congress should be the entity to respond to the changing circumstances brought about by new technology rather than an administrative agency such as OFAC. Current law shouldn’t be stretched in new and novel ways beyond its proper bounds to fit new circumstances.

On that much, we should all agree. Otherwise, OFAC and other agencies will continue to assert even more constitutionally questionable authority.

Strategy (MSTR), the world’s largest corporate owner of bitcoin (BTC), appeared to miss out on capitalizing on last week’s market rout to purchase the dip in prices.

According to Monday’s press release, the firm bought 220 BTC at an average price of $123,561. The company used the proceeds of selling its various preferred stocks (STRF, STRK, STRD), raising $27.3 million.

That purchase price was well above the prices the largest crypto changed hands in the second half of the week. Bitcoin nosedived from above $123,000 on Thursday to as low as $103,000 on late Friday during one, if not the worst crypto flash crash on record, liquidating over $19 billion in leveraged positions.

That move occurred as Trump said to impose a 100% increase in tariffs against Chinese goods as a retaliation for tightening rare earth metal exports, reigniting fears of a trade war between the two world powers.

At its lowest point on Friday, BTC traded nearly 16% lower than the average of Strategy’s recent purchase price. Even during the swift rebound over the weekend, the firm could have bought tokens between $110,000 and $115,000, at a 7%-10% discount compared to what it paid for.

With the latest purchase, the firm brought its total holdings to 640,250 BTC, at an average acquisition price of $73,000 since starting its bitcoin treasury plan in 2020.

MSTR, the firm’s common stock, was up 2.5% on Monday.

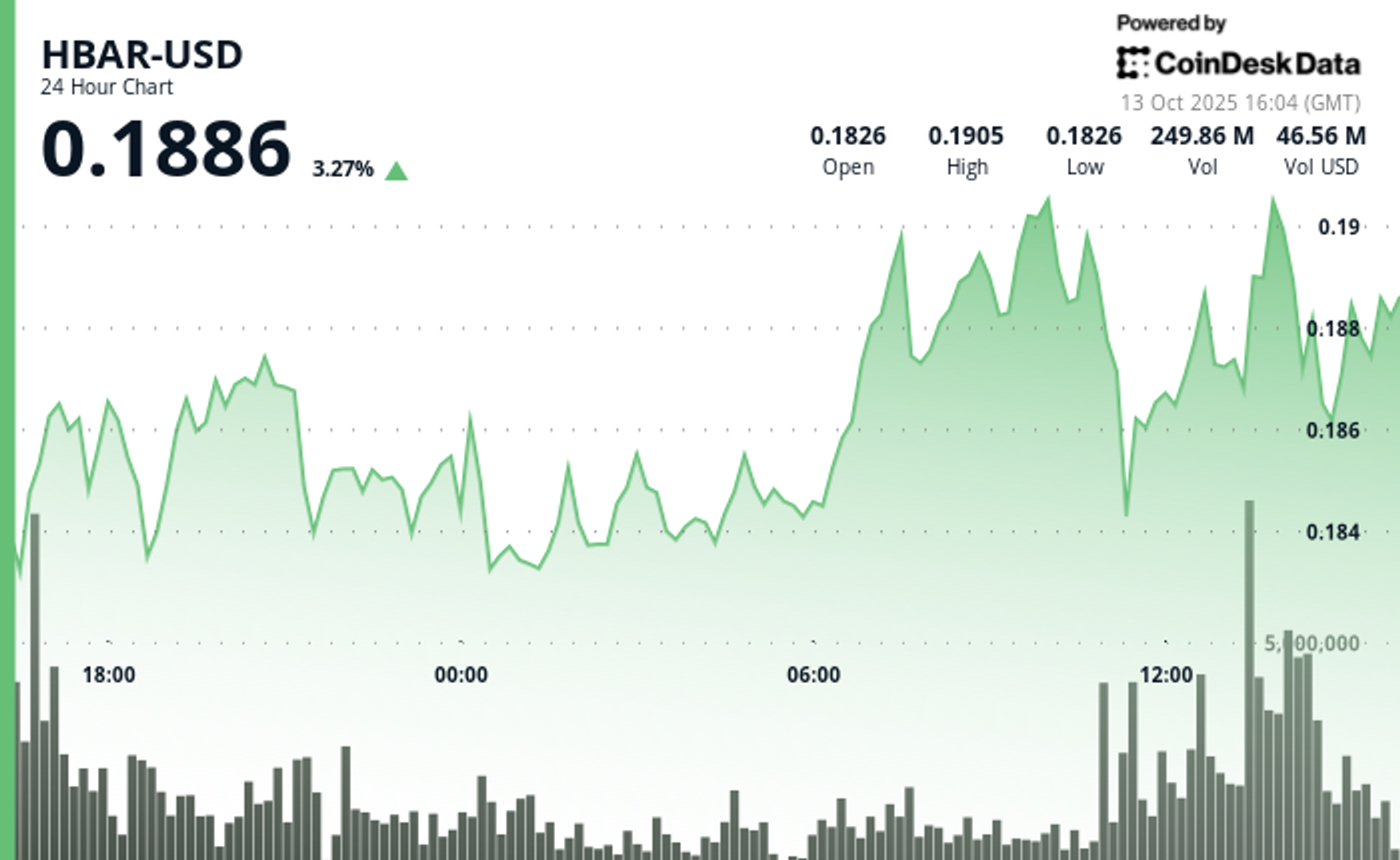

HBAR (Hedera Hashgraph) experienced pronounced volatility in the final hour of trading on Oct. 13, soaring from $0.187 to a peak of $0.191—a 2.14% intraday gain—before consolidating around $0.190.

The move was driven by a dramatic surge in trading activity, with a standout 15.65 million tokens exchanged at 13:31, signaling strong institutional participation. This decisive volume breakout propelled the asset beyond its prior resistance range of $0.190–$0.191, establishing a new technical footing amid bullish momentum.

The surge capped a broader 23-hour rally from Oct. 12 to 13, during which HBAR advanced roughly 9% within a $0.17–$0.19 bandwidth. This sustained upward trajectory was characterized by consistent volume inflows and a firm recovery from earlier lows near $0.17, underscoring robust market conviction. The asset’s ability to preserve support above $0.18 throughout the period reinforced confidence among traders eyeing continued bullish action.

Strong institutional engagement was evident as consecutive high-volume intervals extended through the breakout window, suggesting renewed accumulation and positioning for potential continuation. HBAR’s price structure now shows resilient support around $0.189–$0.190, signaling the possibility of further upside if momentum persists and broader market conditions remain favorable.

")

Technical Indicators Highlight Bullish Sentiment

- HBAR operated within a $0.017 bandwidth (9%) spanning $0.174 and $0.191 throughout the previous 23-hour period from 12 October 15:00 to 13 October 14:00.

- Substantial volume surges reaching 179.54 million and 182.77 million during 11:00 and 13:00 sessions on 13 October validated positive market sentiment.

- Critical resistance materialized at $0.190-$0.191 thresholds where price movements encountered persistent selling activity.

- The $0.183-$0.184 territory established dependable support through volume-supported bounces.

- Extraordinary volume explosion at 13:31 registering 15.65 million units signaled decisive breakout event.

- High-volume intervals surpassing 10 million units through 13:35 substantiated significant institutional engagement.

- Asset preserved support above $0.189 despite moderate profit-taking activity.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

The crypto market staged a recovery on Monday following the weekend’s $500 billion bloodbath that resulted in a $10 billion drop in open interest.

Bitcoin (BTC) rose by 1.4% while ether (ETH) outperformed with a 2.5% gain. Synthetix (SNX, meanwhile, stole the show with a 120% rally as traders anticipate «perpetual wars» between the decentralized trading venue and HyperLiquid.

Plasma (XPL) and aster (ASTER) both failed to benefit from Monday’s recovery, losing 4.2% and 2.5% respectively.

Derivatives Positioning

- The BTC futures market has stabilized after a volatile period. Open interest, which had dropped from $33 billion to $23 billion over the weekend, has now settled at around $26 billion. Similarly, the 3-month annualized basis has rebounded to the 6-7% range, after dipping to 4-5% over the weekend, indicating that the bullish sentiment has largely returned. However, funding rates remain a key area of divergence; while Bybit and Hyperliquid have settled around 10%, Binance’s rate is negative.

- The BTC options market is showing a renewed bullish lean. The 24-hour Put/Call Volume has shifted to be more in favor of calls, now at over 56%. Additionally, the 1-week 25 Delta Skew has risen to 2.5% after a period of flatness.

- These metrics indicate a market with increasing demand for bullish exposure and upside protection, reflecting a shift away from the recent «cautious neutrality.»

- Coinglass data shows $620 million in 24 hour liquidations, with a 34-66 split between longs and shorts. ETH ($218 million), BTC ($124 million) and SOL ($43 million) were the leaders in terms of notional liquidations. Binance liquidation heatmap indicates $116,620 as a core liquidation level to monitor, in case of a price rise.

Token Talk

By Oliver Knight

- The crypto market kicked off Monday with a rebound in the wake of a sharp weekend leverage flush. According to data from CoinMarketCap, the total crypto market cap climbed roughly 5.7% in the past 24 hours, with volume jumping about 26.8%, suggesting those liquidated at the weekend are repurchasing their positions.

- A total of $19 billion worth of derivatives positions were wiped out over the weekend with the vast majority being attributed to those holding long positions, in the past 24 hours, however, $626 billion was liquidated with $420 billion of that being on the short side, demonstrating a reversal in sentiment, according to CoinGlass.

- The recovery has been tentative so far; the dominance of Bitcoin remains elevated at about 58.45%, down modestly from recent highs, which implies altcoins may still lag as capital piles back into safer large-cap names.

- The big winner of Monday’s recovery was synthetix (SNX), which rose by more than 120% ahead of a crypto trading competition that will see it potentially start up «perpetual wars» with HyperLiquid.

Strategy Bought $27M in Bitcoin at $123K Before Crypto Crash

HBAR Rises Past Key Resistance After Explosive Decline

Crypto Markets Today: Bitcoin and Altcoins Recover After $500B Crash

-

Business12 месяцев ago

Business12 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion12 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment12 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment12 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment12 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Uncategorized4 месяца ago

Uncategorized4 месяца agoRobinhood Launches Micro Bitcoin, Solana and XRP Futures Contracts

-

Business12 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment12 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton