Uncategorized

Tokenized Stocks Aren’t Working (Yet)

One of the hallmarks of new technology is that, at first, it’s often worse than the one it replaces. I remember sitting in my apartment sometime in the late-1990s and spending a weekend ripping my CDs into MP3s only to get a hard-drive crash and lose all my data on Sunday night. I had a “why am I doing this” moment, and many of the early buyers of tokenized stocks are feeling the same way. And then I repeated the process the following weekend, because I’m a slow learner.

If digital music had started and then ended with Napster and my Rio PMP-300 (because IYKYK) then we could all forget about it. But it didn’t. It got better and now it’s just what we do. So is the pattern we will see with tokenized stocks.

Tokenized stocks today are a notably inferior product to the traditional market offering. I looked through the terms and conditions of eight different on-chain services offering tokenized assets to get a good understanding of what is available. Most are available in the E.U., one is available globally excluding the U.S. and one is available in the U.S. only.

While these can all be considered good efforts, most platforms offering these stocks restrict them in many ways that are tedious and show the underlying infrastructure isn’t really crypto-native yet. The restrictions that exist so far mostly appear to be the result of efforts to comply with as yet not-fully-defined regulations or shortcomings in the underlying markets (such as a lack of weekend hours).

Read more: Paul Brody — Ethereum Has Already Won

For most platforms, trading is available 24 hours a day, but only five days a week. Many tokens carry geographic restrictions and have “know your customers” (KYC)/permissioning restrictions on transfers. These token offerings rarely have voting rights, some do not permit dividends, and most do not allow tokens to be used in any decentralized finance (DeFi) services either.

Stock trading on-chain today is rudimentary and if it were to end here, it would be a tiny market restricted to a limited number of customers who do not have access to major equity markets. Slowly but surely, however, I think we will overcome many of these limitations.

Limits overcome

Take KYC, for example. Though KYC rules are unlikely to go away, as they become standardized, instead of being restricted to trading with a tiny group of people who are using the exact same vendor and partner running the same KYC process, all the small liquidity pools will become interoperable, effectively becoming a larger liquidity pool. And with deeper liquidity will come market-makers willing to support 24×7 trading without any pricing penalty. Increasing regulatory maturity will probably enable voting rights, dividends, and the automation of withholding taxes as well.

All these steps will, in time, make tokenized stock trading largely comparable to traditional stock trading. If we go back to the music analogy that’s okay, but hardly a compelling reason to switch. It will appeal to those who have limited access to stocks today, but if you have on-chain assets and verified KYC, chances are good you can already obtain a bank account and a brokerage account. This means that parity with existing offerings will not be compelling.

We can already see where on-chain offerings are going, and it’s more than parity. The recent Robinhood announcement of a Layer-2 network on Ethereum included the promise of tokenized access to private companies such as SpaceX and OpenAI. Beyond that, the ability to plug on-chain assets into DeFi services and use them as collateral or lend them out for added return will bring many users into the market.

Lastly, I think there is the potential to truly transform corporate governance. Despite several hundred years of experience, shareholder governance leaves a lot to be desired. Many owners fail to exercise any of their rights. It’s hardly surprising given we can barely keep up with real politics. But, with smart contracts, the ability to delegate your voting rights to experts you trust opens a whole new world of informed governance.

Early adoption is often driven by users with unique needs and a tolerance for risk. This is a perfect example of the whole crypto ecosystem, including users who have accumulated assets outside of the entire traditional financial system.

But, over time, we’re going to get from “because we can” to something much better. And, when that happens, the current $3-4 trillion in crypto assets and a few hundred billion in stablecoins will be dwarfed by the $200+ trillion in stocks and bonds that can come on-chain. It’s only a matter of time.

Disclaimer: These are the personal views of the author and do not represent the views of EY.

Strategy (MSTR), the world’s largest corporate owner of bitcoin (BTC), appeared to miss out on capitalizing on last week’s market rout to purchase the dip in prices.

According to Monday’s press release, the firm bought 220 BTC at an average price of $123,561. The company used the proceeds of selling its various preferred stocks (STRF, STRK, STRD), raising $27.3 million.

That purchase price was well above the prices the largest crypto changed hands in the second half of the week. Bitcoin nosedived from above $123,000 on Thursday to as low as $103,000 on late Friday during one, if not the worst crypto flash crash on record, liquidating over $19 billion in leveraged positions.

That move occurred as Trump said to impose a 100% increase in tariffs against Chinese goods as a retaliation for tightening rare earth metal exports, reigniting fears of a trade war between the two world powers.

At its lowest point on Friday, BTC traded nearly 16% lower than the average of Strategy’s recent purchase price. Even during the swift rebound over the weekend, the firm could have bought tokens between $110,000 and $115,000, at a 7%-10% discount compared to what it paid for.

With the latest purchase, the firm brought its total holdings to 640,250 BTC, at an average acquisition price of $73,000 since starting its bitcoin treasury plan in 2020.

MSTR, the firm’s common stock, was up 2.5% on Monday.

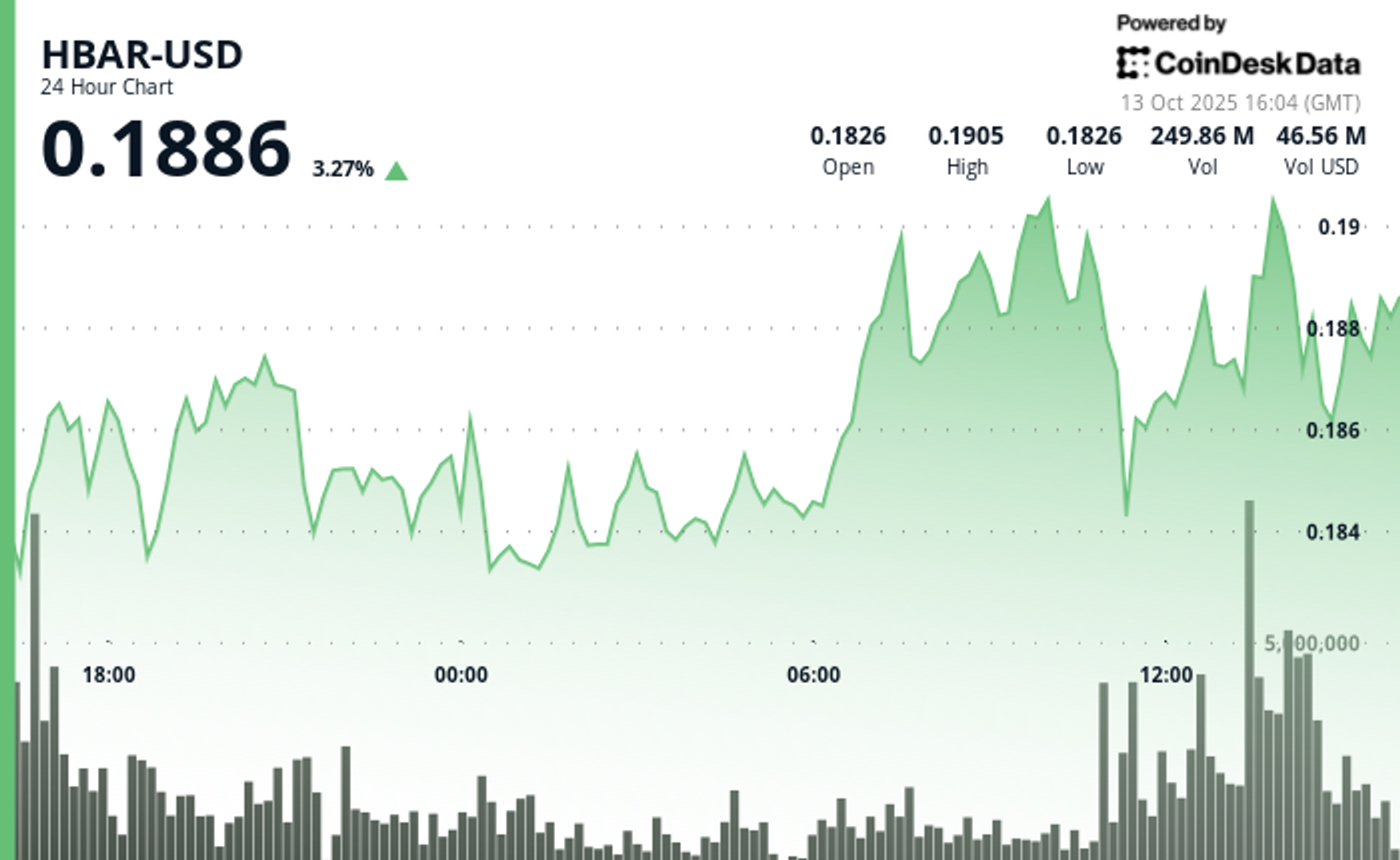

HBAR (Hedera Hashgraph) experienced pronounced volatility in the final hour of trading on Oct. 13, soaring from $0.187 to a peak of $0.191—a 2.14% intraday gain—before consolidating around $0.190.

The move was driven by a dramatic surge in trading activity, with a standout 15.65 million tokens exchanged at 13:31, signaling strong institutional participation. This decisive volume breakout propelled the asset beyond its prior resistance range of $0.190–$0.191, establishing a new technical footing amid bullish momentum.

The surge capped a broader 23-hour rally from Oct. 12 to 13, during which HBAR advanced roughly 9% within a $0.17–$0.19 bandwidth. This sustained upward trajectory was characterized by consistent volume inflows and a firm recovery from earlier lows near $0.17, underscoring robust market conviction. The asset’s ability to preserve support above $0.18 throughout the period reinforced confidence among traders eyeing continued bullish action.

Strong institutional engagement was evident as consecutive high-volume intervals extended through the breakout window, suggesting renewed accumulation and positioning for potential continuation. HBAR’s price structure now shows resilient support around $0.189–$0.190, signaling the possibility of further upside if momentum persists and broader market conditions remain favorable.

")

Technical Indicators Highlight Bullish Sentiment

- HBAR operated within a $0.017 bandwidth (9%) spanning $0.174 and $0.191 throughout the previous 23-hour period from 12 October 15:00 to 13 October 14:00.

- Substantial volume surges reaching 179.54 million and 182.77 million during 11:00 and 13:00 sessions on 13 October validated positive market sentiment.

- Critical resistance materialized at $0.190-$0.191 thresholds where price movements encountered persistent selling activity.

- The $0.183-$0.184 territory established dependable support through volume-supported bounces.

- Extraordinary volume explosion at 13:31 registering 15.65 million units signaled decisive breakout event.

- High-volume intervals surpassing 10 million units through 13:35 substantiated significant institutional engagement.

- Asset preserved support above $0.189 despite moderate profit-taking activity.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

The crypto market staged a recovery on Monday following the weekend’s $500 billion bloodbath that resulted in a $10 billion drop in open interest.

Bitcoin (BTC) rose by 1.4% while ether (ETH) outperformed with a 2.5% gain. Synthetix (SNX, meanwhile, stole the show with a 120% rally as traders anticipate «perpetual wars» between the decentralized trading venue and HyperLiquid.

Plasma (XPL) and aster (ASTER) both failed to benefit from Monday’s recovery, losing 4.2% and 2.5% respectively.

Derivatives Positioning

- The BTC futures market has stabilized after a volatile period. Open interest, which had dropped from $33 billion to $23 billion over the weekend, has now settled at around $26 billion. Similarly, the 3-month annualized basis has rebounded to the 6-7% range, after dipping to 4-5% over the weekend, indicating that the bullish sentiment has largely returned. However, funding rates remain a key area of divergence; while Bybit and Hyperliquid have settled around 10%, Binance’s rate is negative.

- The BTC options market is showing a renewed bullish lean. The 24-hour Put/Call Volume has shifted to be more in favor of calls, now at over 56%. Additionally, the 1-week 25 Delta Skew has risen to 2.5% after a period of flatness.

- These metrics indicate a market with increasing demand for bullish exposure and upside protection, reflecting a shift away from the recent «cautious neutrality.»

- Coinglass data shows $620 million in 24 hour liquidations, with a 34-66 split between longs and shorts. ETH ($218 million), BTC ($124 million) and SOL ($43 million) were the leaders in terms of notional liquidations. Binance liquidation heatmap indicates $116,620 as a core liquidation level to monitor, in case of a price rise.

Token Talk

By Oliver Knight

- The crypto market kicked off Monday with a rebound in the wake of a sharp weekend leverage flush. According to data from CoinMarketCap, the total crypto market cap climbed roughly 5.7% in the past 24 hours, with volume jumping about 26.8%, suggesting those liquidated at the weekend are repurchasing their positions.

- A total of $19 billion worth of derivatives positions were wiped out over the weekend with the vast majority being attributed to those holding long positions, in the past 24 hours, however, $626 billion was liquidated with $420 billion of that being on the short side, demonstrating a reversal in sentiment, according to CoinGlass.

- The recovery has been tentative so far; the dominance of Bitcoin remains elevated at about 58.45%, down modestly from recent highs, which implies altcoins may still lag as capital piles back into safer large-cap names.

- The big winner of Monday’s recovery was synthetix (SNX), which rose by more than 120% ahead of a crypto trading competition that will see it potentially start up «perpetual wars» with HyperLiquid.

Strategy Bought $27M in Bitcoin at $123K Before Crypto Crash

HBAR Rises Past Key Resistance After Explosive Decline

Crypto Markets Today: Bitcoin and Altcoins Recover After $500B Crash

-

Business12 месяцев ago

Business12 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion12 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment12 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment12 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment12 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Uncategorized4 месяца ago

Uncategorized4 месяца agoRobinhood Launches Micro Bitcoin, Solana and XRP Futures Contracts

-

Business12 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment12 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton