Uncategorized

The Risks of Overbuilding Crypto Infrastructure

The Web3 ecosystem is often regarded as the next infrastructure of the internet. However, nearly 10 years after the release of the Ethereum white paper, we have very few mainstream applications running on that infrastructure. Meanwhile, we continue to see the emergence of new infrastructure building blocks everywhere: L1, L2, and L3 blockchains, rollups, ZK layers, DeFi protocols, and many others. While we might be building the future of the internet with Web3, there is little doubt that we are overbuilding the infrastructure layer. Currently, the ratio between infrastructure and applications in Web3 has no parallels in the history of technology markets.

Why is this happening? Simply because it’s profitable to build infrastructure in Web3.

Web3 defies some of the conventional market adoption patterns in tech infrastructure, creating both a rapid path to profitability and unique risks for its evolution. To explore this thesis further, we must understand how value is typically created in infrastructure technology trends, how Web3 diverges from this norm, and the risks posed by overbuilding infrastructure.

The Infrastructure-Application Value Creation Cycle in Tech Markets

Traditionally, value creation in tech markets fluctuates between the infrastructure and application layers, finding a dynamic balance between the two.

Take the Web1 era as an example. Companies such as Cisco, IBM, and Sun Microsystems powered the infrastructure layer of the internet. But, even during those early days, applications like Netscape and AOL emerged to capture significant value. The Web2 era was driven by cloud infrastructure, which then triggered SaaS and social platforms, catalyzing the creation of new cloud infrastructure.

More recently, trends like generative AI began as an infrastructure play with model builders, but applications such as ChatGPT, NotebookLM, and Perplexity quickly captured momentum. This, in turn, drove the creation of new infrastructure to support a new generation of AI applications — a cycle that is likely to continue for several iterations.

This constant value-creation balance between application and infrastructure layers has been a hallmark of technology markets, making Web3 a notable anomaly. But why is this imbalance so evident in Web3?

The Infrastructure Casino

The main difference between Web3 and its predecessors is the rapid path to capital formation and liquidity in infrastructure projects. In Web3, infrastructure projects typically launch tokens that become tradable on exchanges, providing substantial liquidity for investors, teams, and communities. This contrasts with traditional markets, where investor liquidity is typically realized through company acquisitions or public offerings, both of which usually take considerable time. Most venture capital firms operate on a ten-year investment cycle or longer. While rapid capital formation is one of the benefits of Web3, it often misaligns team incentives, discouraging long-term value creation.

This «infrastructure casino» is a risky pattern in Web3 because it incentivizes builders and investors to prioritize infrastructure projects over applications. After all, who needs applications when L2 tokens can achieve multibillion-dollar valuations in just a few years with minimal usage? This approach presents several challenges, and many of them are subtle and difficult to address.

The Challenges of Overbuilding Web3 Infrastructure

1) Building Without Adoption Feedback

Perhaps the most significant risk of overbuilding infrastructure in Web3 is the lack of market feedback from applications built on top of that infrastructure. Applications represent the ultimate expression of consumer and business use cases and regularly guide new use cases in infrastructure. Without application feedback, Web3 risks building infrastructure for “imaginary” use cases that are disconnected from market reality.

2) Extreme Liquidity Fragmentation

The launch of new Web3 infrastructure ecosystems is one of the main contributors to liquidity fragmentation in the space. New blockchains often require billions of dollars to bootstrap liquidity and attract tier 1 DeFi projects to their ecosystems. Over the past few months, the creation of new L1 and L2 blockchains has outpaced the influx of new capital into the market. As a result, capital in Web3 is more fragmented than ever, creating significant adoption challenges.

3) Inevitable, Increasing Complexity

Have you tried using some of the wallets, dApps, and bridges for newer blockchains? The user experience is typically difficult. Tech infrastructure naturally grows more complex and sophisticated over time. Applications built on that infrastructure typically abstract away this complexity for end users. However, in Web3 — where there is a lack of application development — users are left to interact with increasingly complex blockchains, leading to friction in adoption.

4) Limited Developer Communities

If Web3 infrastructure has outpaced capital formation, then the challenge is even greater when it comes to developer communities. dApps are built by developers, and creating new developer communities is always a challenge. Most new Web3 infrastructure projects operate with very limited developer communities because they pull talent from the same existing pool, which is simply not large enough to sustain the vast amount of infrastructure being built.

5) Widening Gap with Web2

A side effect of overbuilding infrastructure in Web3 — without app adoption — is the widening adoption gap with Web2. Trends such as generative AI are powering a new generation of Web2 apps and redefining sectors like SaaS and mobile. Instead of tapping into this momentum, the predominant trend in Web3 continues to be building more blockchains.

Ending the Vicious Circle

Launching L1 and L2 blockchains is a profitable business for investors and development teams, but that doesn’t necessarily translate into long-term benefits for the Web3 ecosystem. Web3 is still in its early stages, and while more infrastructure building blocks are certainly needed, most of the industry is currently building infrastructure without market feedback.

That market feedback typically comes from applications using the infrastructure — but such applications are largely absent in Web3. Most usage of Web3 infrastructure comes from other Web3 infrastructure projects. We continue to build infrastructure, launch tokens, and raise capital, but we are effectively flying blind.

Solana SOL jumped about 5% Monday morning amid rumors that a SOL Staking exchange-trade fund (ETF) by Rex Shares and Osprey Funds could start trading on the market as soon as Wednesday.

The token later fell back slightly, now trading up about 2.3% over the past 24 hours at $157 at press time.

A spokesperson for Osprey confirmed to CoinDesk that the «fund will launch Wednesday,» following a post on X by the automated headline account «Unfolded.»

Just last week, Rex filed a letter with the Securities and Exchange Commission (SEC) asking whether comments had been resolved for their filing. Later that day, the asset manager posted on X that the ETF was “coming soon,” suggesting that the SEC had no further comments.

The REX-Osprey SOL+Staking ETF would be the first of its kind in the U.S. Several issuers are still awaiting approval for a spot SOL ETF which would likely also include staking capabilities.

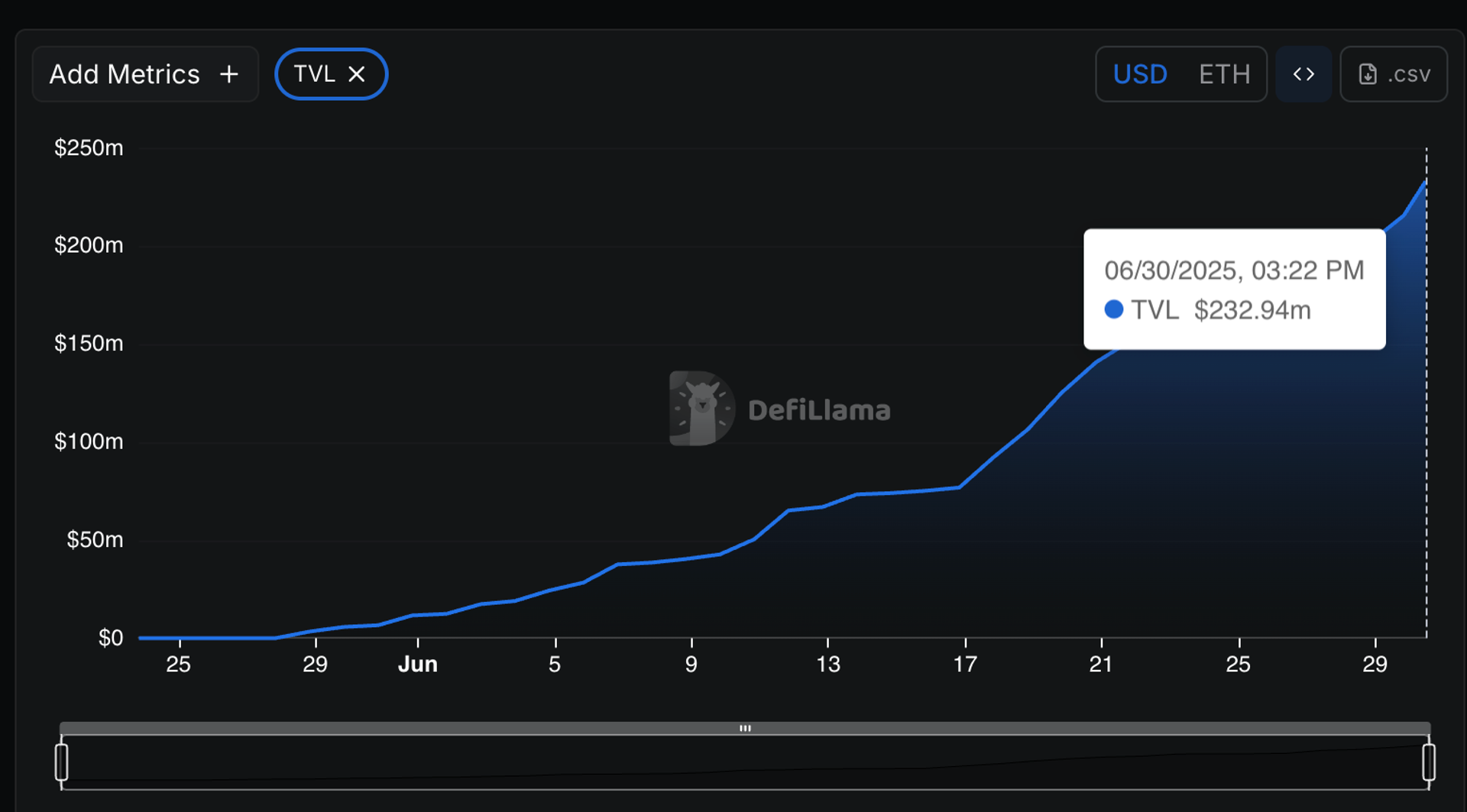

Self described ‘DeFi-first’ layer-2 blockchain Katana has launched its mainnet after receiving $232 million in pre-deposits.

Deposits flooded in after Katana was revealed to the public less than a month ago. DefiLlama data shows that deposited jumped from $75M to $2320M between June 1 and June 30.

Depositors will receive randomized reward NFTs called Krates, as well as a share of 70 million KAT tokens, Katana’s native token. Upon launch, yield farmers will be able earn more KAT by staking on platforms like Morpho and Sushi.

The blockchain aims to solve one of DeFi’s largest problems: Liquidity.

A lack of liquidity can lead to a multitude of issues including slippage, inefficient pricing and unsustainable yields.

Some of the mechanisms Katana will use to solve that the issues is VaultBridge, which is a product that enables yield generation on deposited assets on Ethereum, as well as chain-owned liquidity (CoL), which allows Katana to retain 100% of net sequencer fees and convert them into liquidity reserves.

«Katana represents the endgame for how blockchains create value in DeFi,» Marc Boiron, co-contributor of Katana said in a press release.

The launch coincides with yield farming incentives including token rewards for liquidity providers on Morpho and Sushi.

Despite being based on Ethereum, Katana is blockchain agnostic so users can generate a yield on blockchains like Solana through Katana’s collaboration with Jito, a liquid staking protocol.

UPDATE (June 30, 2025, 17:46 UTC): Updates to reflect new numbers in pre-deposits.

On July 30, 2025, we will be celebrating a decade since Ethereum launched on mainnet. Inarguably, one of the biggest milestones in this industry’s short life.

When it launched as the world’s first smart contract platform, this was obviously something entirely new and a completely new way of thinking about software. Instead of renting access to someone else’s platform that could change the rules or lock you out at any moment, one could – in theory – now participate in systems that belonged to everyone and no one, where the rules were written in code and couldn’t be arbitrarily changed by a CEO’s whim. Users would own their date, and software would be maintained and managed by a network rather than a boardroom. The consequences seemed pretty utopian.

However, nearly ten years on from Ethereum’s launch and the dreams of a Web3 version of Amazon, eBay, Facebook or TikTok haven’t arrived, and are nowhere on the horizon.

Gavin Wood, Ethereum co-founder, and his vision of “Web3” envisaged exactly that. Joe Lubin, the renowned founder of Consensys, said that “Ethereum will have that same pervasive influence on our communications and our entire information infrastructure.»

The libertarian journalist Jim Epstein predicted a year after Ethereum’s launch that “the same types of services offered by companies like Facebook, Google, eBay, and Amazon will be provided instead by computers distributed around the globe.”

Vitalik Buterin himself envisaged Ethereum “law, cloud storage, prediction markets, trading decentralized hosting, [hosting] your own currency,” in his 2014 Bitcoin Miami speech, where he announced Ethereum to the world. “Perhaps even Skynet,” the fictional artificial neural network from the Terminator films. He has described the platform he created as both a threat and an opportunity to platforms like Facebook and Twitter back in 2021.

The Scale Problem

The barrier to achieving this vision is scale. The most successful consumer applications today serve hundreds of millions of users. Instagram processes more than 1 billion photo uploads daily. eBay handles roughly 17 billion dollars in transactions each quarter. Facebook’s messaging platforms process trillions of messages annually.

Ethereum processes about 14 transactions per second, and Solana can handle over 1000. Instagram handles over 1 billion photo uploads daily. eBay processes 17 billion dollars in transactions quarterly. The math doesn’t work.

Let’s entertain the decentralized eBay example for a moment. A truly decentralized eBay would demand far more than simple payments. Every listing creation or update would require onchain transactions for item metadata, pricing, and condition details. Auctions would need automatic bidding resolution with time-locked smart contracts. Escrow systems would have to hold funds until delivery confirmation, with DAO arbitration for disputes.

User reputation systems would require immutable rating storage tied to wallet addresses. Inventory management would need real-time stock tracking, possibly through tokenized goods. Shipping confirmations would demand oracle integration for delivery proofs. Marketplace fees and tax royalties would need smart contract enforcement. Optional identity verification systems would require decentralized credential management. Each interaction would multiply the transaction load exponentially beyond what current infrastructure could support.

It goes without saying that this would require a blockchain of unprecedented speed and throughput. Frankly, a decade after Ethereum, the infrastructure just hasn’t been there to support it.

The Economics Don’t Work

The business model hasn’t always made sense either. Modern applications need massive scale to generate revenue that covers development costs. Furthermore, layer 2 solutions fragment users across platforms, where (for example) Arbitrum users can’t directly interact with Polygon applications. This defeats the purpose of building unified global computing.

This isn’t theoretical. OpenSea struggled with profitability despite dominating NFT trading with high-value transactions & fee-tolerant users. If you can’t profit from selling digital art to crypto enthusiasts paying hundreds in fees, how do you build a marketplace for used goods? The economics are even worse for lower-value transactions that define mainstream commerce. A decentralized social network charging $5 per post would be dead on arrival.

Gaming applications that require a few dollars in transaction fees for every item trade won’t attract players who expect the same for free elsewhere. So far, the only viable on-chain businesses have been those that can extract massive value from relatively few users – essentially high-stakes financial applications and speculative trading.

The Calvary Is Coming

The industry accepted a false tradeoff: security and decentralization, or functionality and scale, but not both. But transaction throughput has steadily increased (and will continue to) across networks as the technology matures. We can now achieve massive scale even with proof of work chains, maintaining the security and decentralization that made blockchain revolutionary in the first place (rather than the premature embrace of proof of stake that compromised these principles).

Zero-knowledge proofs allow users to prove transaction validity locally, submitting only small cryptographic proofs that are aggregated recursively and in parallel by a network of provers. Networks can process millions of transactions without every node verifying each one individually. When users prove their own transactions, the marginal cost of adding an additional transaction approaches zero, and blockchains can finally support the economics that mainstream applications require.

But ten years on, it’s clear that the vision once laid out by the futurists of Web3 has moved at a disappointing pace. Let’s hope the next decade moves a little faster – and, fingers crossed – our blockchains too.

First Solana ETF to Hit the Market This Week; SOL Price Jumps 5%

Katana Mainnet Goes Live as Pre-Deposits Hit $232M

Why Are There No Big DApps on Ethereum?

-

Business9 месяцев ago

Business9 месяцев ago3 Ways to make your business presentation more relatable

-

Entertainment9 месяцев ago

10 Artists who retired from music and made a comeback

-

Fashion9 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment9 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Business9 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment9 месяцев ago

Disney\’s live-action Aladdin finally finds its stars

-

Entertainment9 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Tech9 месяцев ago

5 Crowdfunded products that actually delivered on the hype