Uncategorized

The Future of Crypto Enforcement in the U.S.

Having served as the first chief of the SEC’s crypto unit from 2017 to 2019, I’m often asked what kind of crypto enforcement we should expect to see from the new administration. My first answer is that I do not know. My second answer is that I believe it will be different, but it will not disappear.

To anticipate the future of crypto enforcement, we should begin by reviewing the past.

The beginning

The SEC’s crypto enforcement unit was formed in 2017 during the first Trump Administration. The early focus was on one, fraud, and two, core capital raising events. Regulation of capital raising is the principal purpose of the Securities Act of 1933. When an investor gives money to an entrepreneur who will use it in a business to generate profit, the investor is entitled to certain information about the business. Early crypto investigations were focused on this fundraising activity, which was usually in the form of an unregistered initial coin offering (“ICO”). The idea was that many ICOs at that time were not so different in substance than equity or debt offerings, and should be regulated similarly.

The industry responded responsibly and now, crypto entrepreneurs often raise money in compliance with the federal securities laws. In one of several options, some offerings are exempt from SEC registration because they are limited to accredited investors. The entrepreneurs then use the capital to build a blockchain protocol or other crypto product. Once built, sales of tokens probably are not securities offerings because people are not buying tokens as an investment in someone’s business. Even if there is hope for profit, that profit would come from the activities of the buyers and other participants, not the efforts of a central business manager.

The last four years

During the last four years, the SEC has focused more of its enforcement activity on secondary markets such as centralized trading platforms and decentralized protocols. It is less clear how the federal securities laws apply to these markets. These transactions generally do not involve a central entrepreneur collecting money from investors and using it in a business. Instead, there are thousands or even millions of crypto participants interacting with each other, sometimes anonymously via autonomous software. Token buyers might not know who sold them tokens and there may be no central actor that’s key to future success. Federal district courts have reached different conclusions and there are reports that the SEC might drop one of these key cases.

More broadly, enforcement became the dominant focus of SEC regulation. The SEC doubled the size of the crypto unit, creating new supervisory and trial attorney positions. It spent years and a tremendous amount of resources litigating several non-fraud cases. Many additional non-unit lawyers worked on crypto investigations, and crypto appeared to be the main focus of SEC enforcement.

This approach did not generate useful guidance to the industry. Many SEC rules have technical aspects that are incompatible with the anonymous decentralized ledger that is blockchain technology. Under the enforcement approach of recent years, the very premise of the technology was treated not as a feature, but as a bug. The result was existential enforcement risk to a burgeoning industry and economic activity being pushed offshore.

The future

I do not believe the crypto industry wants a Wild West of no regulation. They want a sensible rulebook that makes compliance feasible, and they also want regulators to crack down on fraud. No legitimate actor benefits from fraud in the industry.

What does this mean for the next four years of enforcement?

First, enforcement is just one component of regulation. We likely will see increased resources dedicated to the other parts of effective regulation — new guidance and rules that offer an achievable regulatory framework. Acting SEC Chairman Mark Uyeda recently announced a new crypto task force for developing a “sensible regulatory path,” and Commissioner Hester Peirce, who will lead the task force, included in her objectives “preserv[ing] industry’s ability to offer products and services.” The dedicated crypto unit also has been reduced in size and repurposed to cyber and emerging technologies, with many staff returning to general enforcement duties.

Second, we could see a renewed focus on fighting fraud. The Commission did not stop bringing crypto fraud cases during the last four years, but many headline cases were non-fraud regulatory disputes. That might change; as Commissioner Peirce said in her objectives speech, “We do not tolerate liars, cheaters, and scammers.”

Third, once there is a new rulebook, we can expect the SEC to enforce those rules. That will take time. We might see a transition period, with some non-fraud cases but more focus on writing the new rulebook. Once adopted, enforcement of that rulebook could come after a fair notice period for the industry to adapt to it.

Conclusion

I expect SEC crypto enforcement to continue, but with different priorities. Investor protection will be balanced with the SEC’s co-equal mandates of facilitating capital formation and maintaining orderly markets. The crypto industry is filled with good actors who want to be compliant; they just need a rulebook that makes compliance achievable. A renewed approach will allow the industry to grow without abandoning investor protection.

The SEC has been the most assertive crypto regulator so far, but it is not alone. Other federal agencies may emerge as co-equal regulatory leaders, either through legislation or otherwise, especially if the SEC no longer takes the position that every cryptocurrency (except Bitcoin) is a security. Some state authorities have been active in crypto, and that likely will continue or even increase.

A client recently reminded me that there will be another election in four years. The new regulatory approach, and the industry’s business and product decisions, must be durable. If they are not, the renewed approach to crypto over the next four years could be undone as easily as that of the last four years.

Strategy (MSTR), the world’s largest corporate owner of bitcoin (BTC), appeared to miss out on capitalizing on last week’s market rout to purchase the dip in prices.

According to Monday’s press release, the firm bought 220 BTC at an average price of $123,561. The company used the proceeds of selling its various preferred stocks (STRF, STRK, STRD), raising $27.3 million.

That purchase price was well above the prices the largest crypto changed hands in the second half of the week. Bitcoin nosedived from above $123,000 on Thursday to as low as $103,000 on late Friday during one, if not the worst crypto flash crash on record, liquidating over $19 billion in leveraged positions.

That move occurred as Trump said to impose a 100% increase in tariffs against Chinese goods as a retaliation for tightening rare earth metal exports, reigniting fears of a trade war between the two world powers.

At its lowest point on Friday, BTC traded nearly 16% lower than the average of Strategy’s recent purchase price. Even during the swift rebound over the weekend, the firm could have bought tokens between $110,000 and $115,000, at a 7%-10% discount compared to what it paid for.

With the latest purchase, the firm brought its total holdings to 640,250 BTC, at an average acquisition price of $73,000 since starting its bitcoin treasury plan in 2020.

MSTR, the firm’s common stock, was up 2.5% on Monday.

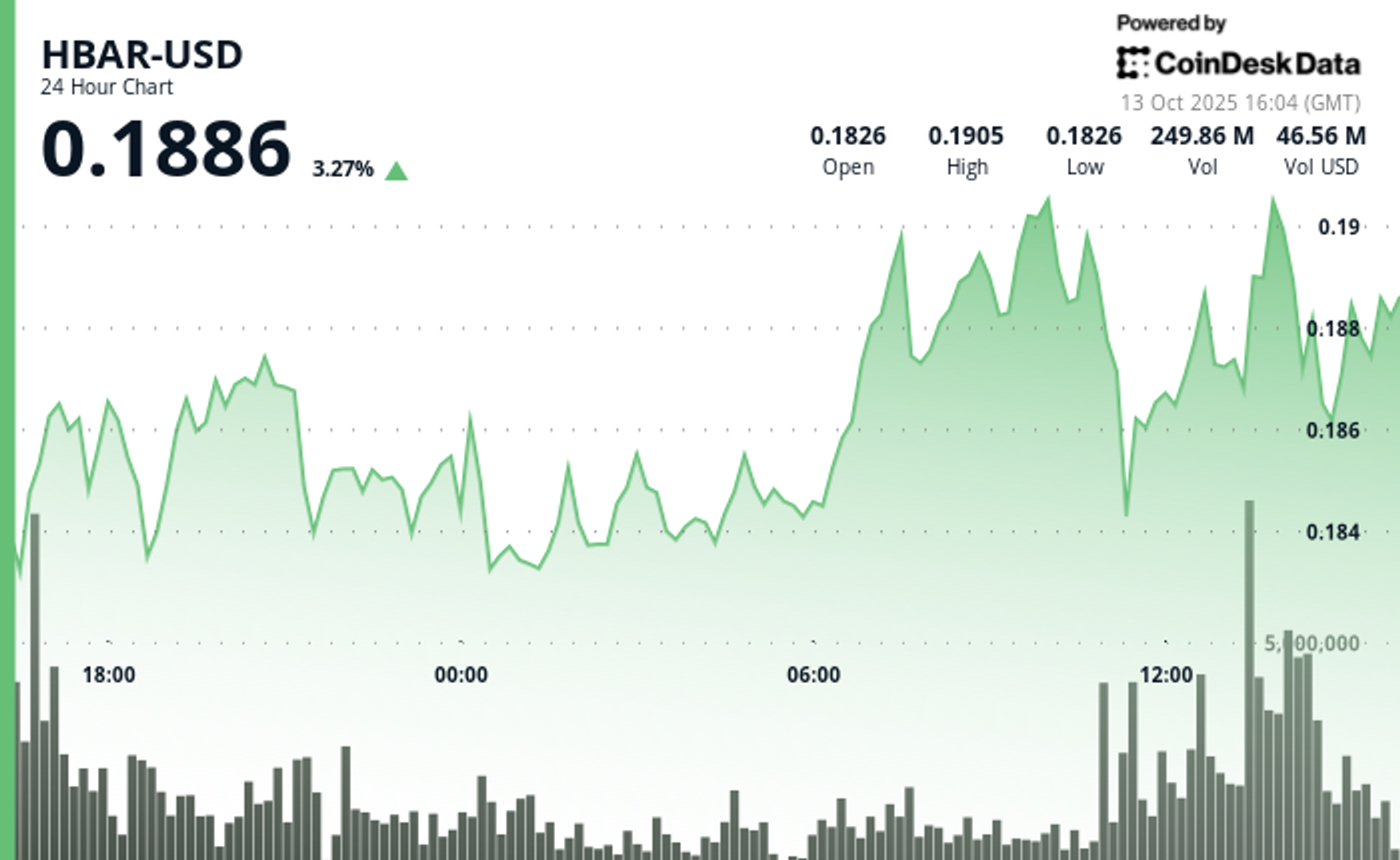

HBAR (Hedera Hashgraph) experienced pronounced volatility in the final hour of trading on Oct. 13, soaring from $0.187 to a peak of $0.191—a 2.14% intraday gain—before consolidating around $0.190.

The move was driven by a dramatic surge in trading activity, with a standout 15.65 million tokens exchanged at 13:31, signaling strong institutional participation. This decisive volume breakout propelled the asset beyond its prior resistance range of $0.190–$0.191, establishing a new technical footing amid bullish momentum.

The surge capped a broader 23-hour rally from Oct. 12 to 13, during which HBAR advanced roughly 9% within a $0.17–$0.19 bandwidth. This sustained upward trajectory was characterized by consistent volume inflows and a firm recovery from earlier lows near $0.17, underscoring robust market conviction. The asset’s ability to preserve support above $0.18 throughout the period reinforced confidence among traders eyeing continued bullish action.

Strong institutional engagement was evident as consecutive high-volume intervals extended through the breakout window, suggesting renewed accumulation and positioning for potential continuation. HBAR’s price structure now shows resilient support around $0.189–$0.190, signaling the possibility of further upside if momentum persists and broader market conditions remain favorable.

")

Technical Indicators Highlight Bullish Sentiment

- HBAR operated within a $0.017 bandwidth (9%) spanning $0.174 and $0.191 throughout the previous 23-hour period from 12 October 15:00 to 13 October 14:00.

- Substantial volume surges reaching 179.54 million and 182.77 million during 11:00 and 13:00 sessions on 13 October validated positive market sentiment.

- Critical resistance materialized at $0.190-$0.191 thresholds where price movements encountered persistent selling activity.

- The $0.183-$0.184 territory established dependable support through volume-supported bounces.

- Extraordinary volume explosion at 13:31 registering 15.65 million units signaled decisive breakout event.

- High-volume intervals surpassing 10 million units through 13:35 substantiated significant institutional engagement.

- Asset preserved support above $0.189 despite moderate profit-taking activity.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

The crypto market staged a recovery on Monday following the weekend’s $500 billion bloodbath that resulted in a $10 billion drop in open interest.

Bitcoin (BTC) rose by 1.4% while ether (ETH) outperformed with a 2.5% gain. Synthetix (SNX, meanwhile, stole the show with a 120% rally as traders anticipate «perpetual wars» between the decentralized trading venue and HyperLiquid.

Plasma (XPL) and aster (ASTER) both failed to benefit from Monday’s recovery, losing 4.2% and 2.5% respectively.

Derivatives Positioning

- The BTC futures market has stabilized after a volatile period. Open interest, which had dropped from $33 billion to $23 billion over the weekend, has now settled at around $26 billion. Similarly, the 3-month annualized basis has rebounded to the 6-7% range, after dipping to 4-5% over the weekend, indicating that the bullish sentiment has largely returned. However, funding rates remain a key area of divergence; while Bybit and Hyperliquid have settled around 10%, Binance’s rate is negative.

- The BTC options market is showing a renewed bullish lean. The 24-hour Put/Call Volume has shifted to be more in favor of calls, now at over 56%. Additionally, the 1-week 25 Delta Skew has risen to 2.5% after a period of flatness.

- These metrics indicate a market with increasing demand for bullish exposure and upside protection, reflecting a shift away from the recent «cautious neutrality.»

- Coinglass data shows $620 million in 24 hour liquidations, with a 34-66 split between longs and shorts. ETH ($218 million), BTC ($124 million) and SOL ($43 million) were the leaders in terms of notional liquidations. Binance liquidation heatmap indicates $116,620 as a core liquidation level to monitor, in case of a price rise.

Token Talk

By Oliver Knight

- The crypto market kicked off Monday with a rebound in the wake of a sharp weekend leverage flush. According to data from CoinMarketCap, the total crypto market cap climbed roughly 5.7% in the past 24 hours, with volume jumping about 26.8%, suggesting those liquidated at the weekend are repurchasing their positions.

- A total of $19 billion worth of derivatives positions were wiped out over the weekend with the vast majority being attributed to those holding long positions, in the past 24 hours, however, $626 billion was liquidated with $420 billion of that being on the short side, demonstrating a reversal in sentiment, according to CoinGlass.

- The recovery has been tentative so far; the dominance of Bitcoin remains elevated at about 58.45%, down modestly from recent highs, which implies altcoins may still lag as capital piles back into safer large-cap names.

- The big winner of Monday’s recovery was synthetix (SNX), which rose by more than 120% ahead of a crypto trading competition that will see it potentially start up «perpetual wars» with HyperLiquid.

Strategy Bought $27M in Bitcoin at $123K Before Crypto Crash

HBAR Rises Past Key Resistance After Explosive Decline

Crypto Markets Today: Bitcoin and Altcoins Recover After $500B Crash

-

Business12 месяцев ago

Business12 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion12 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment12 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment12 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment12 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Uncategorized4 месяца ago

Uncategorized4 месяца agoRobinhood Launches Micro Bitcoin, Solana and XRP Futures Contracts

-

Business12 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment12 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton