Uncategorized

No, the Stablecoin Bill Isn’t Built for Billionaires

Sen. Elizabeth Warren (MA-D) recently sounded the alarm over new proposals on stablecoin legislation, claiming they’d give Elon Musk a “clear runway” to control U.S. money and payments.

If that sounds overly-dramatic, it’s because it is.

Here’s what these bills actually do: the GENIUS Act and the STABLE Act aim to create responsible guardrails for stablecoins, ensuring consumer protection and financial stability while encouraging innovation. Far from handing the keys to a single billionaire, they lay out clear standards so that no one — the world’s richest man or otherwise — can dominate payment infrastructure by sidestepping important safeguards.

At their core, stablecoins are digital assets designed to maintain a constant value—most commonly tied to the U.S. dollar and backed by a basket of reserves. However, the transparency and composition of an issuer’s dollar reserves may vary, which some regulatory proposals aim to clarify.

By definition, dollar-denominated stablecoins reinforce the dollar’s role in the global economy rather than undermining it. Contrary to the claim that these bills would allow one person to “print money,” the GENIUS Act and STABLE Act are chiefly about setting minimum reserve, auditing, and licensing standards for stablecoin issuers. The fundamental idea is to ensure transparent, fully backed stablecoins under a clear regulatory regime, not to let a tech titan mint unbacked currency at will.

Stablecoins offer innovations the legacy financial system has long struggled to provide: efficient, low-cost transfers, potentially faster settlements, and ability to instantly execute transactions that can fuel new financial products. They can be sent globally in near-real time, lowering barriers and giving everyday users more autonomy over their money, whether that be for remittances or payments for everyday purchases.

The size of the global stablecoin ecosystem is notable and is forcing traditional financial entities into the market. The growth in transaction volumes is hard to ignore; they climbed to $710 billion in February, compared with $521 billion in the same month last year.

This future of finance is an upgrade over traditional infrastructure, which is dominated by large financial institutions that often dictate costs and limit options for smaller players. By replacing cumbersome, expensive intermediaries, stablecoins empower consumers to transact more directly, preserving their privacy and autonomy without sacrificing efficiency.

Stablecoins also bolster national security and support the U.S. dollar’s global dominance. The U.S. dollar’s position as the world’s reserve currency provides significant geopolitical and economic advantages. With the rise of alternative financial systems, including foreign-issued digital assets, the United States must ensure that emerging technologies remain dollar-denominated.

If innovators cannot operate within the U.S. under clear rules, they may turn to foreign jurisdictions, effectively weakening the dollar’s role. Encouraging stablecoin issuers to hold traditional U.S. treasuries as backing — rather than synthetic or foreign-issued substitutes — helps maintain steady demand for U.S. debt instruments and keeps the dollar anchored at the heart of global finance.

At the same time, other countries are exploring strategies to reassert the dollar in ways that loop out American influence — so-called “de-dollarization” plans where foreign governments structure their trades and bonds in dollar equivalents without the traditional oversight or support of U.S. institutions.

If we do not modernize our own financial infrastructure, we risk losing control over the direction of dollar-based innovation. Providing a predictable regulatory framework for stablecoins helps encourage developers and businesses to keep building on U.S. soil, ensuring that America remains at the forefront of this next wave of finance.

Both the GENIUS Act and STABLE Act propose guardrails to ensure stablecoin issuers meet baseline requirements for consumer protection and operational soundness. While each may have its strengths and weaknesses, they reflect a growing effort in Congress to produce thoughtful, bipartisan legislation.

Such legislation would reduce uncertainty, spur responsible innovation, and promote healthy competition in the digital asset marketplace. By clarifying legal obligations around reserve composition, auditing, and anti-money laundering practices, these bills aim to foster an environment where stablecoins can thrive under proper oversight — protecting consumers, upholding financial stability, and supporting national security interests.

Elon Musk’s interest in digital payments, as with any ambitious project, highlights the larger trend: private sector initiatives are moving rapidly, sometimes outpacing existing laws. Establishing solid regulatory foundations for stablecoins is the first step in ensuring that emerging ventures — whether they come from tech entrepreneurs or established financial giants—must operate within rules that protect the public and preserve vital U.S. interests.

Proper legislation isn’t about letting a billionaire corner the market. It’s about providing certainty and accountability so that when a product like “X Money” or another innovative payment system inevitably comes along, it must meet rigorous standards for consumer protection and financial stability.

The future of money is poised to be more digital, transparent, and open. By embracing stablecoin legislation, Congress can strengthen the role of the U.S. dollar, foster innovation at home, and ensure that our financial system remains safe, secure, and competitive. That outcome serves everyday consumers, fortifies national security, and preserves America’s economic leadership in a rapidly evolving world.

Ethereum is in the midst of a paradox. Even as ether hit record highs in late August, decentralized finance (DeFi) activity on Ethereum’s layer-1 (L1) looks muted compared to its peak in late 2021. Fees collected on mainnet in August were just $44 million, a 44% drop from the prior month.

Meanwhile, layer-2 (L2) networks like Arbitrum and Base are booming, with $20 billion and $15 billion in total value locked (TVL) respectively.

This divergence raises a crucial question: are L2s cannibalizing Ethereum’s DeFi activity, or is the ecosystem evolving into a multi-layered financial architecture?

AJ Warner, the chief strategy officer of Offchain Labs, the developer firm behind layer-2 Arbitrum, argues that the metrics are more nuanced than just layer-2 DeFi chipping at the layer 1.

In an interview with CoinDesk, Warner said that focusing solely on TVL misses the point, and that Ethereum is increasingly functioning as crypto’s “global settlement layer,” a foundation for high-value issuance and institutional activity. Products like Franklin Templeton’s tokenized funds or BlackRock’s BUIDL product launch directly on Ethereum L1 — activity that isn’t fully captured in DeFi metrics but underscores Ethereum’s role as the bedrock of crypto finance.

Ethereum as a layer-1 blockchain is the secure but relatively slow and expensive base network. Layer-2s are scaling networks built on top of it, designed to handle transactions faster and at a fraction of the cost before ultimately settling back to Ethereum for security. That’s why they’ve become so appealing to traders and builders alike. Metrics like TVL, the amount of crypto deposited in DeFi protocols, highlight this shift, as activity is moved to L2s where lower fees and quicker confirmations make everyday DeFi far more practical.

Warner likens Ethereum’s place in the ecosystem to a wire transfer in traditional finance: trusted, secure and used for large-scale settlement. Everyday transactions, however, are migrating to L2s — the Venmos and PayPals of crypto.

“Ethereum was never going to be a monolithic blockchain with all the activity happening on it,” Warner told CoinDesk. Instead, it’s meant to anchor security while enabling rollups to execute faster, cheaper and more diverse applications.

Layer 2s, which have exploded over the last few years because they are seen as the faster and cheaper alternative to Ethereum, enable whole categories of DeFi that don’t function as well on mainnet. Fast-paced trading strategies, like arbitraging price differences between exchanges or running perpetual futures, don’t work well on Ethereum’s slower 12-second blocks. But on Arbitrum, where transactions finalize in under a second, those same strategies become possible, Warner explained. This is apparent, as Ethereum has had fewer than 50 million transactions over the last month, compared to Base’s 328 million transactions and Arbitrum’s 77 million transactions, according to L2Beat.

Builders also see L2s as an ideal testing ground. Alice Hou, a research analyst at Messari, pointed to innovations like Uniswap V4’s hooks, customizable features that can be iterated far more cheaply on L2s before going mainstream. For developers, quicker confirmations and lower costs are more than a convenience: they expand what’s possible.

“L2s provide a natural playground to test these kinds of innovations, and once a hook achieves breakout popularity, it could attract new types of users who engage with DeFi in ways that weren’t feasible on L1,” Hou said.

But the shift isn’t just about technology. Liquidity providers are responding to incentives. Hou said that data shows smaller liquidity providers increasingly prefer L2s where yield incentives and lower slippage amplify returns. Larger liquidity providers, however, still cluster on Ethereum, prioritizing security and depth of liquidity over bigger yields.

")

Interestingly, while L2s are capturing more activity, flagship DeFi protocols like Aave and Uniswap still lean heavily on mainnet. Aave has consistently kept about 90% of its TVL on Ethereum. With Uniswap however, there’s been an incremental shift towards L2 activity.

")

Another factor accelerating L2 adoption is user experience. Wallets, bridges and fiat on-ramps increasingly steer newcomers directly to L2s, Hou said. Ultimately, the data suggests the L1 vs. L2 debate isn’t zero-sum.

As of September 2025, about a third of L2 TVL still comes bridged from Ethereum, another third is natively minted, and the rest comes via external bridges.

“This mix shows that while Ethereum remains a key source of liquidity, L2s are also developing their own native ecosystems and attracting cross-chain assets,” Hou said.

Ethereum thus as a base layer appears to be cementing itself as the secure settlement engine for global finance, while rollups like Arbitrum and Base are emerging as execution layers for fast, cheap and creative DeFi applications.

“Most payments I make use something like Zelle or PayPal… but when I bought my home, I used a wire. That’s somewhat parallel to what’s happening between Ethereum layer one and layer twos,” Warner of Offchain Labs said.

Read more: Ethereum DeFi Lags Behind, Even as Ether Price Crossed Record Highs

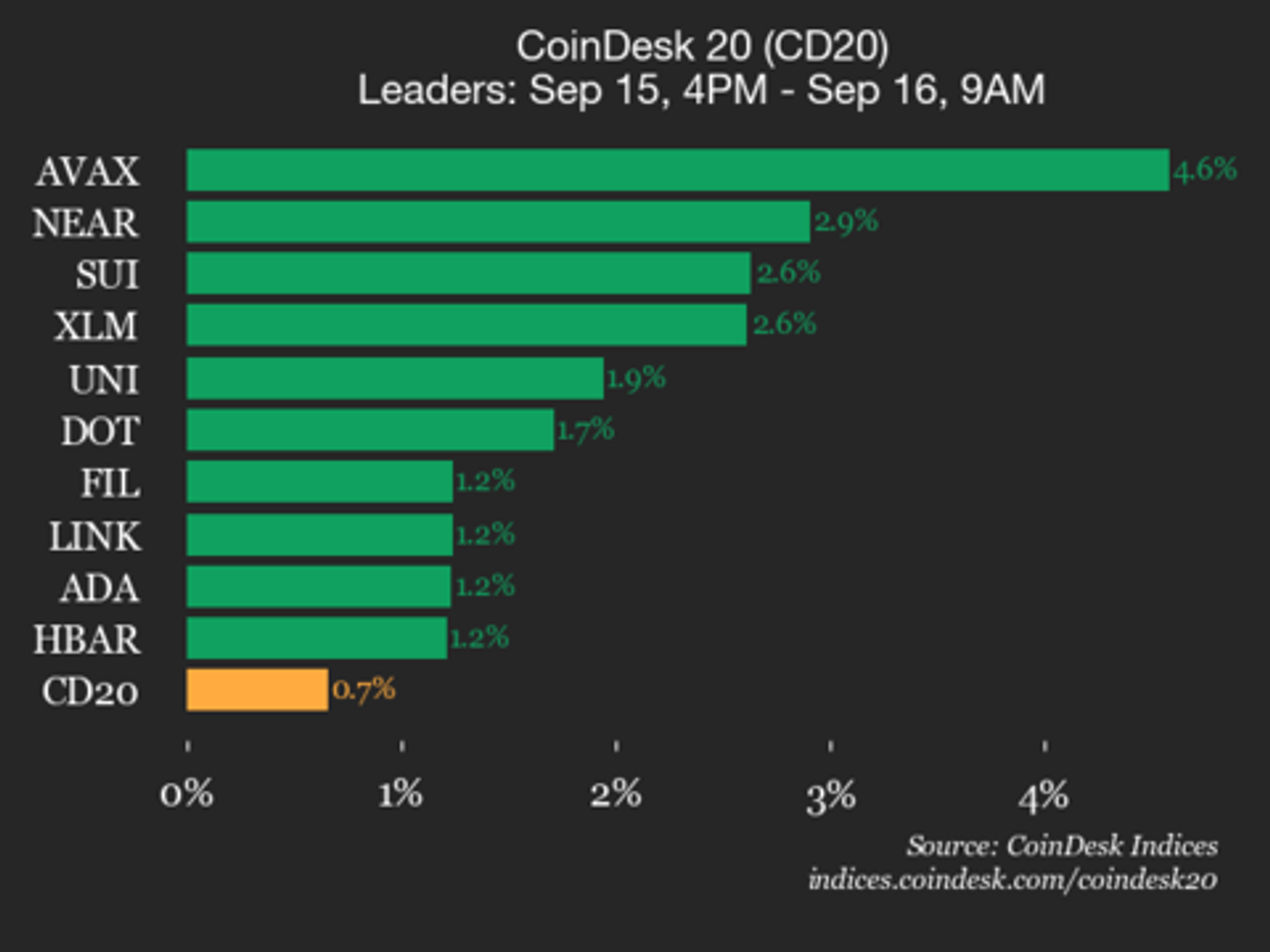

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 4267.12, up 0.7% (+27.81) since 4 p.m. ET on Monday.

Eighteen of 20 assets is trading higher.

Leaders: AVAX (+4.6%) and NEAR (+2.9%).

Laggards: AAVE (-0.9%) and BCH (-0.2%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

The digital banking arm of Spanish financial giant Santander Group, Openbank, opened cryptocurrency trading for customers in Germany, with plans to add its home market in the next few weeks.

The new service allows users to buy, sell and hold five popular cryptocurrencies: bitcoin (BTC), ether (ETH), litecoin (LTC), polygon (MATIC) and cardano (ADA), according to a press release. The cryptocurrencies are available alongside stocks, ETFs and investment funds.

Customers can trade without moving funds to an external platform, keeping all investments in one place under Santander’s umbrella, the bank said.

“By incorporating the main cryptocurrencies into our investment platform, we are responding to the demand of some of our customers,” said Coty de Monteverde, head of crypto at Grupo Santander.

The bank charges a 1.49% fee per transaction, with a 1 euro ($1.2) minimum, and does not include custody fees. The bank said it plans to add more cryptocurrencies and new features, such as crypto-to-crypto conversions, in coming months.

Santander Private Bank was back in 2023 making headlines when it started letting clients with accounts in Switzerland trade BTC and ETH. It selected crypto safekeeping technology firm Taurus for custody.

Is Ethereum’s DeFi Future on L2s? Liquidity, Innovation Say Perhaps Yes

CoinDesk 20 Performance Update: Avalanche (AVAX) Gains 4.6% as Index Moves Higher

Santander’s Openbank Starts Offering Crypto Trading in Germany, Spain Coming Soon

-

Business11 месяцев ago

Business11 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion11 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment11 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment11 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment11 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Business11 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment11 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton

-

Entertainment11 месяцев ago

Disney\’s live-action Aladdin finally finds its stars