Uncategorized

How to Make the United States the Crypto Capital of the World

Dear President-Elect Trump,

In your keynote address at the Bitcoin conference in Nashville last year, you pledged to make the United States the crypto capital of the world if re-elected for a second term. As you return to the presidential office this Monday, we write to you as practicing members of the crypto law bar to recommend regulatory policies that will help you to achieve that goal.

The United States, which rests on the same foundation of personal liberty as crypto, is naturally positioned to lead the world in its development. Unfortunately, U.S. regulators have until now refused to adapt existing laws to digital assets and the blockchains that underpin them (or even to explain why not), and created an unfavorable business environment that has driven many entrepreneurs and developers abroad.

To unleash American ingenuity and remedy this neglect of the blockchain industry, we propose that you pursue the below forward-looking policies across three areas: supporting U.S. companies; promoting crypto values such as privacy, disintermediation, and decentralization; and cultivating a favorable business environment domestically.

Supporting U.S.-Based Businesses

The crypto industry has produced a range of established and emerging use-cases, including digital gold, stablecoins, permissionless payments, decentralized finance, real world assets, decentralized physical infrastructure (DePIN), and many more. Many of them are being responsibly advanced in the United States by businesses such as Coinbase, Circle and Consensys, and by developers contributing to crypto’s open-source, decentralized infrastructure. To continue competing against their international rivals, these parties need clear rules of the road and proper regulatory guidance.

General Rules of the Road

Token issuance and secondary sales, which lie at the heart of the crypto economy, are subject to confusing and overlapping regulatory authority from the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC). Market structure legislation should clearly delineate the scope of jurisdiction among primary regulators and lay out when assets enter and exit that jurisdiction.

Here, Congress should resist giving the U.S. securities laws an overbroad application, as the SEC has done. Tokens powered by open-source software and consensus mechanisms that are otherwise minimally dependent on centralized actors are not securities because there is no legal relationship between token owners and an “issuer,” as understood by the securities laws. Similarly, crypto assets such as art NFTs (which are simply digital artwork) and non-investment activities, like staking and lending bitcoin, fall outside the securities laws.

Congress should be bold. That means not feeling bound by prior legislative efforts like FIT21 that were forged in an earlier political environment that have unintended consequences. It also means leveraging the regulatory experience of other nations, such as the European Union with its MiCA framework, while avoiding their pitfalls and charting a unique and dauntless path forward for the United States.

Specific Sectors

Besides advocating for general rules, your administration should urge Congress and the relevant agencies to address specific sectors due to their strategic importance to the crypto industry and the nation.

Stablecoins. Stablecoins, with a current market cap in excess of $200 billion, are the lifeblood of the digital asset ecosystem. Increasingly recognized under frameworks like the Stablecoin Standard and by state regulators, they warrant comprehensive legislation for their issuance and management, ensuring that they are transparently backed and do not threaten financial stability. Aside from benefitting consumers, regulatory support of stablecoins furthers national interests. Similar to Eurodollars, stablecoins, which are usually denominated in U.S. dollars, reinforce the dollar’s status as the global reserve currency and increase demand for U.S. treasuries, which issuers hold in reserve.

TradFi Integration. The unprecedented success unprecedented success of Bitcoin and Ethereum ETFs demonstrates that crypto has begun integrating with traditional finance. Regulatory policy should ensure a safe and orderly integration by giving consumers access to trusted custody services. This requires amending or rescinding prejudicial SEC accounting guidelines (for instance, SAB 121) and custody rules. But it should not stop there. Pro-innovation policy in this area should also promote the tokenization of securities representing traditional financial assets like stocks, bonds, or real estate as blockchain-based tokens. The resulting benefits, which include improved liquidity, fractional ownership, and faster settlement, would strengthen U.S. capital markets, ensuring they remain the most developed and innovative in the world.

DeFi. Decentralized finance has the potential to modernize the global financial system and to return value to ordinary Americans by removing costly financial intermediaries. You should not allow entrenched interests and alarmism to stop the United States from becoming the world’s leader in DeFi. In this regard, regulations aimed at centralized actors, such as exchanges and issuers, must be crafted in ways that avoid inadvertently capturing and paralyzing the still-nascent DeFi ecosystem.

Fostering Innovation through a Commitment to Crypto Values

If it is to promote crypto innovation, regulatory policy must show respect for crypto values, including privacy, disintermediation, and decentralization. Two key regulatory principles arise from this commitment. First, regulation should not impose greater burdens on crypto where traditional analogs exist. Second, regulation should evolve where traditional analogs are absent.

When To Treat Crypto the Same as Traditional Assets and Tools

The first principle impacts products like self-custody wallets, which enable users to hold and manage their own private keys. Because these tools are analogous to physical wallets used for personal asset management, they should not be treated any differently — namely, as financial intermediaries for purposes of regulatory surveillance and monitoring. You are not required to complete KYC before you can place cash in a physical wallet; the same should be true for storing tokens in your digital wallet.

Similar logic applies to the taxation of block rewards. Americans mining or validating blockchain transactions are creating new property, just like farmers growing crops in their fields. And yet, the IRS currently taxes them on that income. This differential treatment should be abolished.

When To Treat Crypto Differently

The second principle demands regulators resist placing crypto actors and activities into legacy frameworks that are incompatible with crypto. Doing so damages the crypto ecosystem, pushes the industry abroad, and erodes the Rule of Law.

Regrettably, this is the path that many U.S. regulators have chosen. The IRS

has begun treating crypto front-ends as “brokers” absent statutory authority. The Department of Justice has begun charging non-custodial wallet developers with unlicensed money-transmission violations despite its longstanding policy to the contrary. And the U.S. Treasury has sanctioned the smart contract of privacy mixer Tornado Cash even though it is neither a foreign person nor property, but merely code. (An appellate court overturned the sanction.)

Without diminishing the importance of the governmental interests at play (tax evasion, money laundering, and national security), we submit that the government’s approaches in each case are wrong as a matter of innovation policy, and we encourage your administration to reverse them.

Instead of regulating digital asset and blockchain businesses like traditional companies, we urge regulators to collaborate with this new technological paradigm and with our industry. For example, if government surveillance (KYC) in a decentralized environment is actually justified in certain instances, regulators can leverage blockchain-based credentials that are portable across protocols, give users control of their data (a benefit of Web3 architecture), and are aligned with the frictionless blockchain ecosystem. Similarly, they can marshal the programmability of tokens and smart contracts to exclude sanctioned parties from parts of the crypto economy.

Attracting Top Talent With a Welcoming Business Environment

To become the leading destination for top crypto talent, the U.S. must cultivate a favorable business environment. Your administration can begin this process on Day One.

End de-banking of crypto companies. Your administration should direct the FDIC and all other agencies involved with Operation Chokepoint 2.0 to immediately cease their unaccountable campaign aimed at de-banking the crypto industry.

Improve SEC rule-making and enforcement. You should instruct your SEC chair to overhaul that agency’s approach to crypto. Over the past four years, the SEC has consistently exceeded its authority by pursuing good faith industry leaders such as Coinbase and Consensys, regulating individual developers and users (in its exchange redefinition rulemaking), and launching enforcement actions against wallet providers. It is time for the SEC to correct this pernicious approach and begin engaging constructively with the crypto industry while focusing its efforts on preventing fraud rather than curbing financial speculation, which has benefits for innovation.

Roll back punitive tax rules. Your administration should roll back punitive tax rules that push entrepreneurs and developers abroad while leaving well-meaning taxpayers uncertain about how to calculate their tax bills. Low-hanging fruit improvements include the adoption of current expensing for software development; tax deferral for validation rewards and airdrops; a safe harbor for de minimis consumptive transactions (e.g. less than $5,000); a mark-to-market election for crypto investors and a repeal of IRS reporting regulations that treat websites as brokers. Congress should also repeal amendments to Section 6050I, which impose burdensome (and likely unconstitutional) reporting requirements on crypto transactions over $10,000.

Reduce unnecessary red tape. Consistent with the mission of the Department of Government Efficiency (D.O.G.E.), we urge your office to work with Congress and government agencies to reduce the unnecessary red tape restraining crypto and fintech. This includes simplifying or eliminating registration and reporting requirements for digital asset offerings that meet certain conditions, including providing essential investor disclosures. Congress should also consider legislating a unified federal framework for money transmission licensing that would bring clarity and efficiency to the broader fintech ecosystem.

***

In pursuing the above forward-looking policies, we encourage your administration to consult with industry leaders and remain sensitive to the transnational scope of the digital asset ecosystem. (We view your formation of a Crypto Council as a positive step in this direction.) We also recommend leveraging devices, such as regulatory sandboxes, that limit the risk of unintended regulatory consequences.

The time is ripe for the United States to begin asserting its global regulatory leadership. By ensuring that it does, your administration will be contributing to the country’s future economic prosperity and endorsing a technology that rests on deeply held American values and freedoms. You should seize the moment.

Sincerely,

Ivo Entchev, Olta Andoni, Stephen Rutenberg, Donna Redel

The following members of the Crypto Law Bar also signed this letter: Mike Bacina, Joe Carlasare, Eli Cohen, Mike Frisch, Jason Gottlieb, Eric Hess, Katherine Kirkpatrick, Dan McAvoy, John McCarthy, Margaret Rosenfeld, Gabriel Shapiro, Ben Snipes, Noah Spaulding, Andrea Tinianow, Jenny Vatrenko, Collin Woodward, and Rafael Yakobi.

The views represented and reflected upon herein are those of the signatories and not necessarily of their employers.

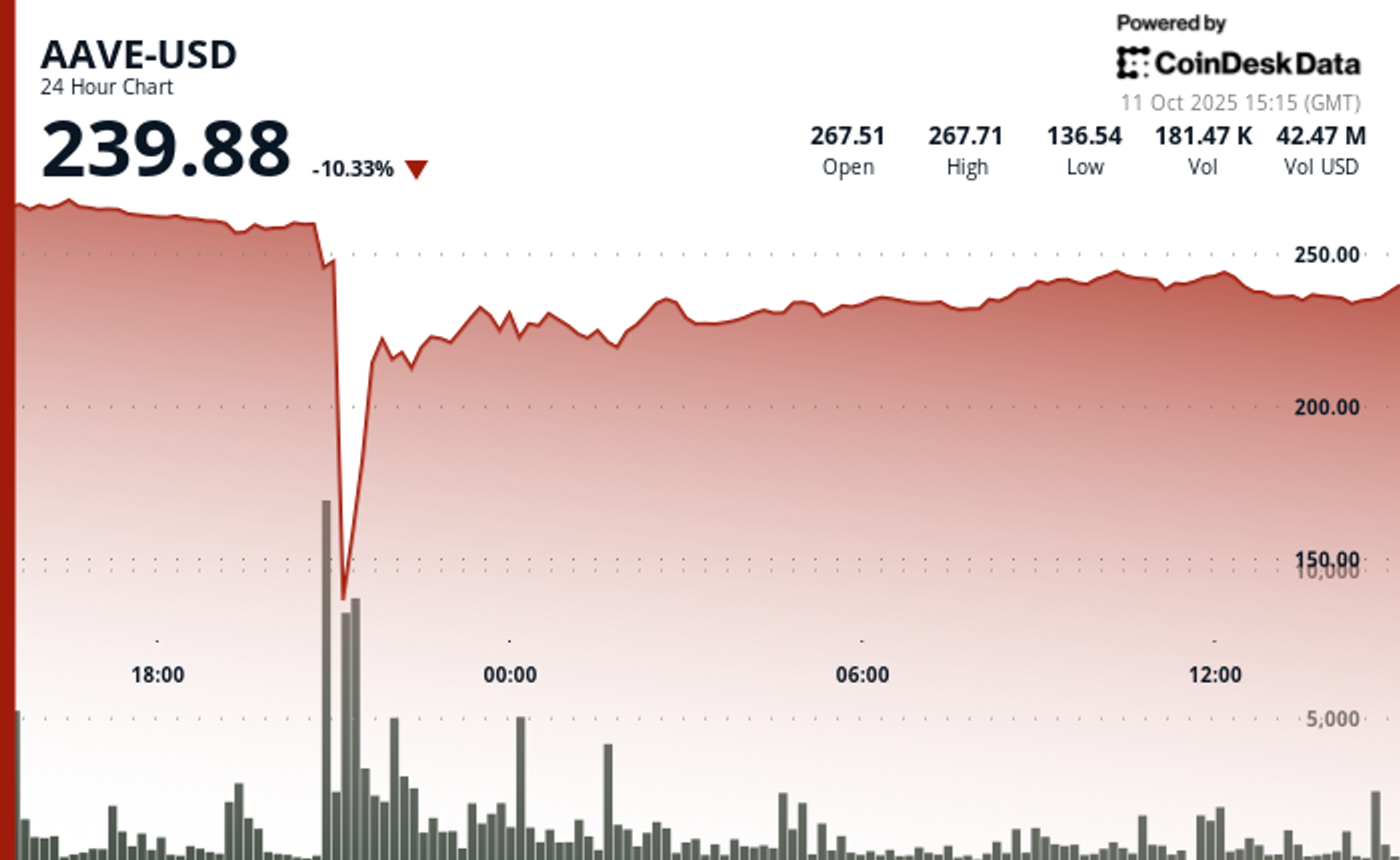

The native token of Aave (AAVE), the largest decentralized crypto lending protocol, was caught in the middle of Friday’s crypto flash crash while the protocol proved resilient in a historic liquidation cascade.

The token, trading at around $270 earlier in Friday, nosedived as much as 64% later in the session to touch $100, the lowest level in 14 months. It then staged a rapid rebound to near $240, still down 10% over the past 24 hours.

Stani Kulechov, founder of Aave, described Friday’s event as the «largest stress test» ever for the protocol and its $75 billion lending infrastructure.

The platform enables investors to lend and borrow digital assets without conventional intermediaries, using innovative mechanisms such as flash loans. Despite the extreme volatility, Aave’s performance underscores the evolving maturity and resilience of DeFi markets.

«The protocol operated flawlessly, automatically liquidating a record $180M worth of collateral in just one hour, without any human intervention,» Kulechov said in a Friday X post. «Once again, Aave has proven its resilience.»

Key price action:

- AAVE sustained a dramatic flash crash on Friday, declining 64% from $278.27 to $100.18 before recuperating to $240.09.

- The DeFi protocol demonstrated remarkable resilience with its native token’s 140% recovery from the intraday lows, underpinned by substantial trading volume of 570,838 units.

- Following the volatility, AAVE entered consolidation territory within a narrow $237.71-$242.80 range as markets digested the dramatic price action.

Technical Indicators Summary

- Price range of $179.12 representing 64% volatility during the 24-hour period.

- Volume surged to 570,838 units, substantially exceeding the 175,000 average.

- Near-term resistance identified at $242.80 capping rebound during consolidation phase.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

AI agents, software systems that use AI to pursue goals and complete tasks on behalf of users, are proliferating. Think of them as digital assistants that can make decisions and take actions towards goals you set without needing step-by-step instructions — from GPT-powered calendar managers to trading bots, the number of use cases is expanding rapidly. As their role expands across the economy, we have to build the right infrastructure that will allow these agents to communicate, collaborate and trade with one another in an open marketplace.

Big tech players like Google and AWS are building early marketplaces and commerce protocols, but that raises the question: will they aim to extract massive rents through walled gardens once more? Agents’ capabilities are clearly rising, almost daily, with the arrival of new models and architectures. What’s at risk is whether these agents will be truly autonomous.

Autonomous agents are valuable because they unlock a novel user experience: a shift from software as passive or reactive tools to active and even proactive partners. Instead of waiting for instructions, they can anticipate needs, adapt to changing conditions, and coordinate with other systems in real time, without the user’s constant input or presence. This autonomy in decision-making makes them uniquely suited for a world where speed and complexity outpace human decision-making.

Naturally, some worry about what greater decision-making autonomy means for work and accountability — but I see it as an opportunity. When agents handle repetitive, time-intensive tasks and parallelize what previously had to be done in sequence, they expand our productive capacity as humans — freeing people to engage in work that demands creativity, judgment, composition and meaningful connection. This isn’t make-believe, humanity has been there before: the arrival of corporations allowed entrepreneurs to create entirely new products and levels of wealth previously unthought of. AI agents have the potential to bring that capability to everyone.

On the intelligence side, truly autonomous decision-making requires AI agent infrastructure that is open source and transparent. OpenAI’s recent OSS release is a good step. Chinese labs, such as DeepSeek (DeepSeek), Moonshot AI (Kimi K2) and Alibaba (Qwen 3), have moved even quicker.

However, autonomy is not purely tied to intelligence and decision making. Without resources, an AI agent has little means to enact change in the real world. Hence, for agents to be truly autonomous they need to have access to resources and self-custody their assets. Programmable, permissionless, and composable blockchains are the ideal substrate for agents to do so.

Picture two scenarios. One where AI agents operate within a Web 2 platform like AWS or Google. They exist within the limited parameters set by these platforms in what is essentially a closed and permissioned environment. Now imagine a decentralized marketplace that spans many blockchain ecosystems. Developers can compose different sets of environments and parameters, therefore, the scope available to AI agents to operate is unlimited, accessible globally, and can evolve over time. One scenario looks like a toy idea of a marketplace, and the other is an actual global economy.

In other words, to truly scale not just AI agent adoption, but agent-to-agent commerce, we need rails that only blockchains can offer.

The Limits of Centralized Marketplaces

AWS recently announced an agent-to-agent marketplace aimed at addressing the growing demand for ready-made agents. But their approach inherits the same inefficiencies and limitations that have long plagued siloed systems. Agents must wait for human verification, rely on closed APIs and operate in environments where transparency is optional, if it exists at all.

To act autonomously and at scale, agents can’t be boxed into closed ecosystems that restrict functionality, pose platform risks, impose opaque fees, or make it impossible to verify what actions were taken and why.

Decentralization Scales Agent Systems

An open ecosystem allows for agents to act on behalf of users, coordinate with other agents, and operate across services without permissioned barriers.

Blockchains already offer the key tools needed. Smart contracts allow agents to perform tasks automatically, with rules embedded in code, while stablecoins and tokens enable instant, global value transfers without payment friction. Smart accounts, which are programmable blockchain wallets like Safe, allow users to restrict agents in their activity and scope (via guards). For instance, an agent may only be allowed to use whitelisted protocols. These tools allow AI agents not only to behave expansively but also to be contained within risk parameters defined by the end user. For example, this could be setting spending limits, requiring multi-signatures for approvals, or restricting agents to whitelisted protocols.

Blockchain also provides the transparency needed so users can audit agent decisions, even when they aren’t directly involved. At the same time, this doesn’t mean that all agent-to-agent interactions need to happen onchain. E.g. AI agents can use offchain APIs with access constraints defined and payments executed onchain.

In short, decentralized infrastructure gives agents the tools to operate more freely and efficiently than closed systems allow.

It’s Already Happening Onchain

While centralized players are still refining their agent strategies, blockchain is already enabling early forms of agent-to-agent interaction. Onchain agents are already exhibiting more advanced behavior like purchasing predictions and data from other agents. And as more open frameworks emerge, developers are building agents that can access services, make payments, and even subscribe to other agents — all without human involvement.

Protocols are already implementing the next step: monetization. With open marketplaces, people and businesses are able to rent agents, earn from specialized ones, and build new services that plug directly into this agent economy. Customisation of payment models such as subscription, one-off payments, or bundled packages will also be key in facilitating different user needs. This will unlock an entirely new model of economic participation.

Why This Distinction Matters

Without open systems, fragmentation breaks the promise of seamless AI support. An agent can easily bring tasks to completion if it stays within an individual ecosystem, like coordinating between different Google apps. However, where third-party platforms are necessary (across social, travel, finance, etc), an open onchain marketplace will allow agents to programmatically acquire the various services and goods they need to complete a user’s request.

Decentralized systems avoid these limitations. Users can own, modify, and deploy agents tailored to their needs without relying on vendor-controlled environments.

We’ve already seen this work in DeFi, with DeFi legos. Bots automate lending strategies, manage positions, and rebalance portfolios, sometimes better than any human could. Now, that same approach is being applied as “agent legos” across sectors including logistics, gaming, customer support, and more.

The Path Forward

The agent economy is growing fast. What we build now will shape how it functions and for whom it works. If we rely solely on centralized systems, we risk creating another generation of AI tools that feel useful but ultimately serve the platform, not the person.

Blockchain changes that. It enables systems where agents act on your behalf, earn on your ideas, and plug into a broader, open marketplace.

If we want agents that collaborate, transact, and evolve without constraint, then the future of agent-to-agent marketplaces must live onchain.

More than 1,000 wallets on Hyperliquid were completely liquidated during the recent violent crypto sell-off, which erased over $1.23 billion in trader capital on the platform, according to data from its leaderboard.

In total, 6,300 wallets are now in the red, with 205 losing over $1 million each according to the data, which was first spotted by Lookonchain. More than 1,000 accounts saw losses of at least $100,000.

The wipeout came as crypto markets reeled from a global risk-off event triggered by U.S. President Donald Trump’s announcement of a 100% additional tariff on Chinese imports.

The move spooked investors across asset classes and sent cryptocurrency prices tumbling. Bitcoin briefly dropped below $110,000 and ether fell under $3,700, while the broader market as measured by the CoinDesk 20 (CD20) index dropped by 15% at one point.

The broad sell-off led to over $19 billion in liquidations over a 24 hours period, making it the largest single-day liquidation event in crypto history by dollar value. According to CoinGlass, the “actual total” of liquidations is “likely much higher” as leading crypto exchange Binance doesn’t report as quickly as other platforms.

Leaderboard data reviewed by CoinDesk shows the top 100 traders on Hyperliquid gained $1.69 billion collectively.

In comparison, the top 100 losers dropped $743.5 million, leaving a net profit of $951 million concentrated among a handful of highly leveraged short sellers.

The biggest winner was wallet 0x5273…065f, which made over $700 million from short positions, while the largest loser, “TheWhiteWhale,” dropped $62.5 million.

Among the victims of the flush is crypto personality Jeffrey Huang, known online as Machi Big Brother, who once launched a defamation suit against ZachXBT, losing almost the entire value of his wallet, amounting to $14 million.

«Was fun while it lasted,» he posted on X.

Adding to the uncertainty, the ongoing U.S. government shutdown has delayed the release of key economic data. Without official indicators, markets are flying blind at a time when geopolitical risk is rising.

AAVE Sees 64% Flash Crash as DeFi Protocol Endures ‘Largest Stress Test’

Blockchain Will Drive the Agent-to-Agent AI Marketplace Boom

‘Largest Ever’ Crypto Liquidation Event Wipes Out 6,300 Wallets on Hyperliquid

-

Business12 месяцев ago

Business12 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion12 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment12 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment12 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment12 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Business12 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment12 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton

-

Entertainment12 месяцев ago

Disney\’s live-action Aladdin finally finds its stars