Uncategorized

Bank of Canada Identifies Technical Path for Retail CBDC in New Research Paper

The Bank of Canada took a significant step in exploring the technical feasibility of a digital Canadian dollar, proposing a specific system designed for a retail central bank digital currency (CBDC) focused on simple, everyday payments, according to a new research paper.

The central bank’s research team examined OpenCBDC 2PC, a model developed in collaboration with the Massachusetts Institute of Technology’s Digital Currency Initiative. This design prioritizes privacy, speed and decentralization by allowing users to hold digital funds directly, much like digital cash.

The new research comes after the Bank of Canada said it is shifting its focus away from a retail CBDC last year, saying that it was prepared if the people of the nation decide such a product is needed in the future.

Privacy issues

A major focus of the report is privacy, which isn’t a big surprise because CBDCs have sparked debate around the world, in part on concerns they could enable state surveillance of financial activity. Unlike cash, which is anonymous, a CBDC could theoretically allow a central authority to track every transaction.

The report suggested that the system separates personal identity from transaction data, allowing non-registered users to hold funds in self-custodied wallets. The users could then transact without sharing their identity with a bank or payment processor. Even for registered users, the central bank would not have access to identifying information or transaction histories.

The report goes further, proposing enhanced protection by potentially using cryptographic techniques such as zero-knowledge proofs to obscure transaction amounts from the core infrastructure. These features collectively offer a level of privacy that the authors say could exceed that of current electronic payment systems.

Bitcoin-like structure

In contrast to traditional banking systems, where money is stored in user accounts, the report suggests a design that uses «unspent transaction outputs» (UTXOs) — a structure more commonly associated with Bitcoin.

The system processes transactions in two steps: updating a core ledger and transferring funds from one user’s wallet to another. This approach supports real-time settlement and offers a higher degree of privacy from both banks and government institutions.

Challenges

While the report lays out a detailed technical solution to a potential digital Canadian dollar, it also identifies potential hurdles.

One of the main hurdles is that integrating the proposed architecture with existing retail payment infrastructure could require substantial technical upgrades, including in the way point-of-sale terminals handle digital cash-like transfers.

Additionally, while the system is scalable in theory, performance dips during audits and system recovery operations need further engineering work to meet production-grade standards.

The paper clearly states that this is not a commitment to launch a CBDC. However, the findings lay out a concrete technical foundation for what such a system could look like— one that balances user privacy, institutional control, and operational resilience.

Whether the central bank will implement it remains a question, given the controversy surrounding CBDC. However, the timing of the report could be right as Canada’s new prime minister, Mark Carney, was quoted in his 2021 book as a supporter of CBDCs.

«The most likely future of money is a central bank stablecoin, known as a central bank digital currency or CBDC,” he wrote in his book.

Ethereum is in the midst of a paradox. Even as ether hit record highs in late August, decentralized finance (DeFi) activity on Ethereum’s layer-1 (L1) looks muted compared to its peak in late 2021. Fees collected on mainnet in August were just $44 million, a 44% drop from the prior month.

Meanwhile, layer-2 (L2) networks like Arbitrum and Base are booming, with $20 billion and $15 billion in total value locked (TVL) respectively.

This divergence raises a crucial question: are L2s cannibalizing Ethereum’s DeFi activity, or is the ecosystem evolving into a multi-layered financial architecture?

AJ Warner, the chief strategy officer of Offchain Labs, the developer firm behind layer-2 Arbitrum, argues that the metrics are more nuanced than just layer-2 DeFi chipping at the layer 1.

In an interview with CoinDesk, Warner said that focusing solely on TVL misses the point, and that Ethereum is increasingly functioning as crypto’s “global settlement layer,” a foundation for high-value issuance and institutional activity. Products like Franklin Templeton’s tokenized funds or BlackRock’s BUIDL product launch directly on Ethereum L1 — activity that isn’t fully captured in DeFi metrics but underscores Ethereum’s role as the bedrock of crypto finance.

Ethereum as a layer-1 blockchain is the secure but relatively slow and expensive base network. Layer-2s are scaling networks built on top of it, designed to handle transactions faster and at a fraction of the cost before ultimately settling back to Ethereum for security. That’s why they’ve become so appealing to traders and builders alike. Metrics like TVL, the amount of crypto deposited in DeFi protocols, highlight this shift, as activity is moved to L2s where lower fees and quicker confirmations make everyday DeFi far more practical.

Warner likens Ethereum’s place in the ecosystem to a wire transfer in traditional finance: trusted, secure and used for large-scale settlement. Everyday transactions, however, are migrating to L2s — the Venmos and PayPals of crypto.

“Ethereum was never going to be a monolithic blockchain with all the activity happening on it,” Warner told CoinDesk. Instead, it’s meant to anchor security while enabling rollups to execute faster, cheaper and more diverse applications.

Layer 2s, which have exploded over the last few years because they are seen as the faster and cheaper alternative to Ethereum, enable whole categories of DeFi that don’t function as well on mainnet. Fast-paced trading strategies, like arbitraging price differences between exchanges or running perpetual futures, don’t work well on Ethereum’s slower 12-second blocks. But on Arbitrum, where transactions finalize in under a second, those same strategies become possible, Warner explained. This is apparent, as Ethereum has had fewer than 50 million transactions over the last month, compared to Base’s 328 million transactions and Arbitrum’s 77 million transactions, according to L2Beat.

Builders also see L2s as an ideal testing ground. Alice Hou, a research analyst at Messari, pointed to innovations like Uniswap V4’s hooks, customizable features that can be iterated far more cheaply on L2s before going mainstream. For developers, quicker confirmations and lower costs are more than a convenience: they expand what’s possible.

“L2s provide a natural playground to test these kinds of innovations, and once a hook achieves breakout popularity, it could attract new types of users who engage with DeFi in ways that weren’t feasible on L1,” Hou said.

But the shift isn’t just about technology. Liquidity providers are responding to incentives. Hou said that data shows smaller liquidity providers increasingly prefer L2s where yield incentives and lower slippage amplify returns. Larger liquidity providers, however, still cluster on Ethereum, prioritizing security and depth of liquidity over bigger yields.

")

Interestingly, while L2s are capturing more activity, flagship DeFi protocols like Aave and Uniswap still lean heavily on mainnet. Aave has consistently kept about 90% of its TVL on Ethereum. With Uniswap however, there’s been an incremental shift towards L2 activity.

")

Another factor accelerating L2 adoption is user experience. Wallets, bridges and fiat on-ramps increasingly steer newcomers directly to L2s, Hou said. Ultimately, the data suggests the L1 vs. L2 debate isn’t zero-sum.

As of September 2025, about a third of L2 TVL still comes bridged from Ethereum, another third is natively minted, and the rest comes via external bridges.

“This mix shows that while Ethereum remains a key source of liquidity, L2s are also developing their own native ecosystems and attracting cross-chain assets,” Hou said.

Ethereum thus as a base layer appears to be cementing itself as the secure settlement engine for global finance, while rollups like Arbitrum and Base are emerging as execution layers for fast, cheap and creative DeFi applications.

“Most payments I make use something like Zelle or PayPal… but when I bought my home, I used a wire. That’s somewhat parallel to what’s happening between Ethereum layer one and layer twos,” Warner of Offchain Labs said.

Read more: Ethereum DeFi Lags Behind, Even as Ether Price Crossed Record Highs

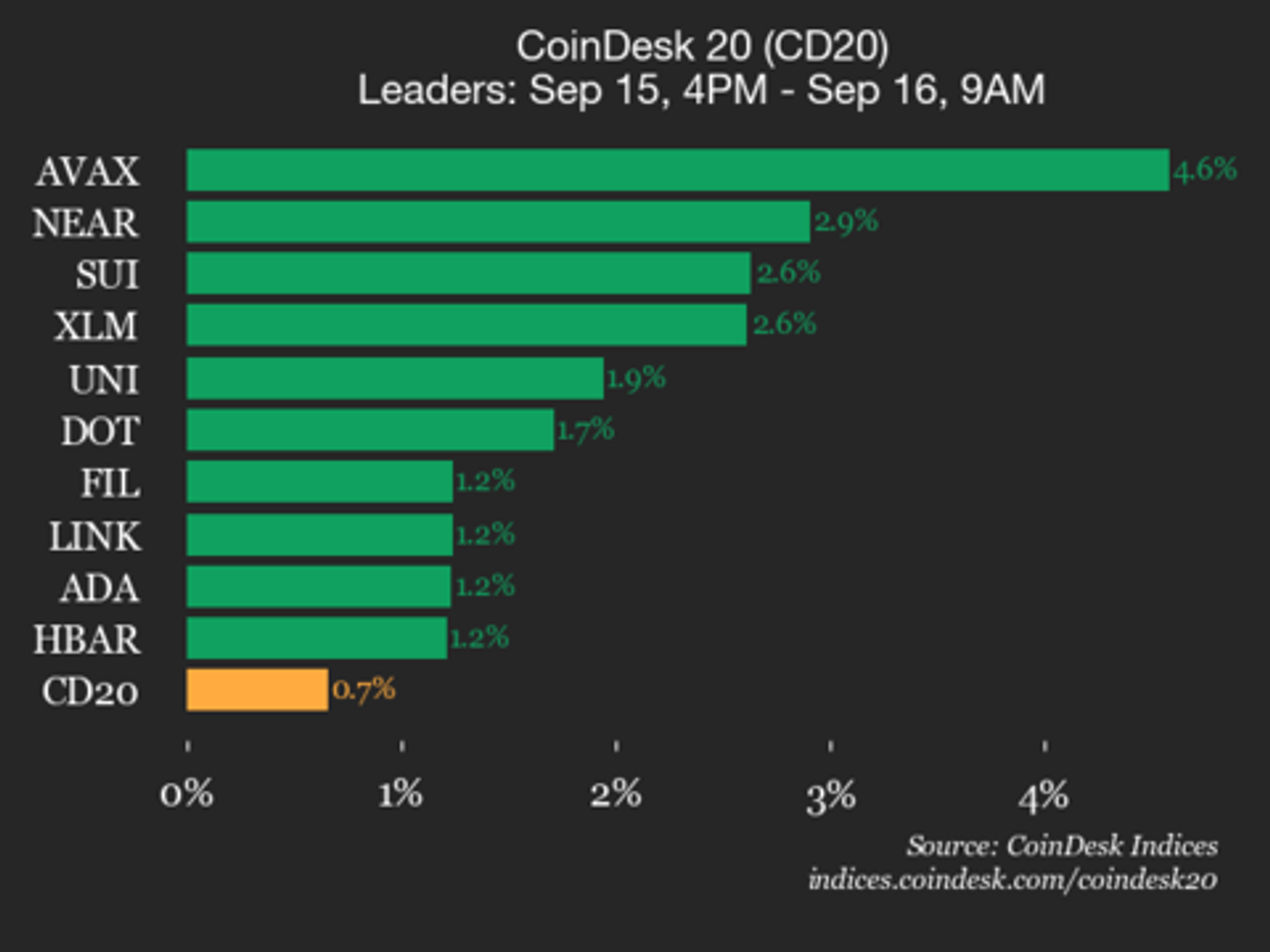

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 4267.12, up 0.7% (+27.81) since 4 p.m. ET on Monday.

Eighteen of 20 assets is trading higher.

Leaders: AVAX (+4.6%) and NEAR (+2.9%).

Laggards: AAVE (-0.9%) and BCH (-0.2%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

The digital banking arm of Spanish financial giant Santander Group, Openbank, opened cryptocurrency trading for customers in Germany, with plans to add its home market in the next few weeks.

The new service allows users to buy, sell and hold five popular cryptocurrencies: bitcoin (BTC), ether (ETH), litecoin (LTC), polygon (MATIC) and cardano (ADA), according to a press release. The cryptocurrencies are available alongside stocks, ETFs and investment funds.

Customers can trade without moving funds to an external platform, keeping all investments in one place under Santander’s umbrella, the bank said.

“By incorporating the main cryptocurrencies into our investment platform, we are responding to the demand of some of our customers,” said Coty de Monteverde, head of crypto at Grupo Santander.

The bank charges a 1.49% fee per transaction, with a 1 euro ($1.2) minimum, and does not include custody fees. The bank said it plans to add more cryptocurrencies and new features, such as crypto-to-crypto conversions, in coming months.

Santander Private Bank was back in 2023 making headlines when it started letting clients with accounts in Switzerland trade BTC and ETH. It selected crypto safekeeping technology firm Taurus for custody.

Is Ethereum’s DeFi Future on L2s? Liquidity, Innovation Say Perhaps Yes

CoinDesk 20 Performance Update: Avalanche (AVAX) Gains 4.6% as Index Moves Higher

Santander’s Openbank Starts Offering Crypto Trading in Germany, Spain Coming Soon

-

Business11 месяцев ago

Business11 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion11 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment11 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment11 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment11 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Business11 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment11 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton

-

Entertainment11 месяцев ago

Disney\’s live-action Aladdin finally finds its stars