Uncategorized

How the Hype for HyperLiquid’s Vault Evaporated on Concerns Over Centralization

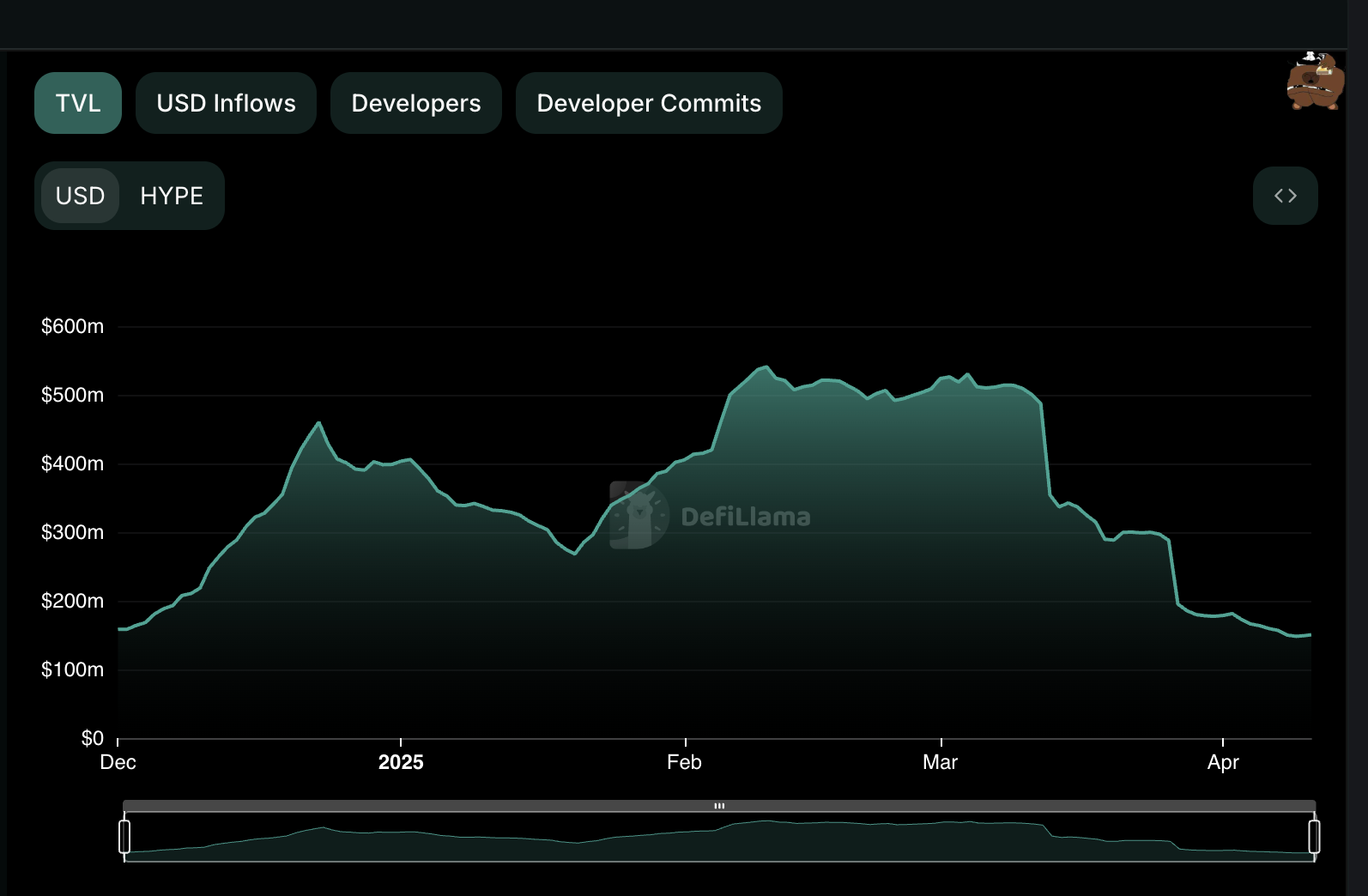

Just two months ago, the total value of funds locked (TVL) on HyperLiquid, a decentralized derivatives exchange (DEX) that allows traders to generate returns by staking to a shared vault, sat at a record $540 million.

Now, users are fleeing, TVL has slumped to $150 million and the yield has dropped to a measly 1%, in many cases, less than they’d get if they stashed their cash in a bank account.

At issue is an exploit that saw one user manipulate the price of a token called JELLY and force the vault, known as Hyperliquidity Provider, into a loss. But the negative PNL wasn’t the reason for the exodus. Rather it was HyperLiquid’s response, which led to concerns about how decentralized the protocol actually was, and whether it was acting exactly like the centralized exchange model it tried to distance itself from.

For the manipulation, the user shorted JELLY on HyperLiquid, that is sold tokens they didn’t own. They also bought tokens on illiquid decentralized exchanges. The lack of liquidity tricked the pricing oracle to relay an inflated price to HyperLiquid, forcing HyperLiquid’s vault to inherit a toxic position via liquidation.

As the price of JELLY rose further because of the spot buying pressure, the PNL for HyperLiquid’s vault sank more heavily into the red. Eventually, the exchange force closed the JELLY market, settling it at $0.0095 as opposed to the $0.50 that was being fed to oracles via decentralized exchanges.

This meant that the negative PNL was wiped away and, on paper, the vault performed well throughout the saga. But the action raised concerns about the control of what’s meant to be a decentralized process. At the time, Newfound Research CEO Corey Hoffstein questioned the legality of HyperLiquid’s actions and social media descended into outrage.

Some believe that the exploit was a mistake on HyperLiquid’s part.

“The Jelly exploit on Hyperliquid wasn’t a fluke,» Jan Philipp Fritsche, managing director at Oak Security, told CoinDesk. «It was a textbook case of unpriced vega risk: when leveraged trading on volatile assets is allowed without properly accounting for how that volatility can drain the risk fund. The attacker opened massive opposing positions in JELLY, knowing that one side would collapse and the other would cash out.

«This isn’t theoretical. It happened. And it will happen again. We flagged this exact risk vector in audits before, but economic flaws often get ignored because they’re not technical. That’s a mistake,» Fritsche added.

In this case, the manipulator ended up with a small loss.

It’s worth pointing out that HyperLiquid attempted to remedy the centralization concerns, upgrading its system to a include an on-chain validator voting for asset delisting, which means that the exchange will not be able to remove like JELLY in future without validator consensus.

Volume remains steady as HYPE tumbles

While the vault suffered a major blow in terms of trust and branding, the exchange itself continues to tick along just fine in terms of trading volume. Over $70 billion worth of volume has been notched so far this month and it looks to be on track to break it’s January record of $197 billion.

Still, the exchange’s native token (HYPE), which was distributed to users in December, has failed to mimic the positive performance of the exchange, losing 60% of its value over the past four months with its market cap dwindling from $9.7 billion to $4.6 billion.

Canary Capital is looking to launch an exchange-traded fund (ETF) tracking the price of Tron’s native token, TRX, according to a filing.

The hedge fund submitted a Form S-1 for the Canary Staked TRX ETF with the Securities and Exchange Commission (SEC) on Friday. As the name suggests, the fund — if approved — would stake portions of its holdings.

This would be done through third-party providers, with BitGo acting as custodian for the assets. The fund would track TRX’s spot price using CoinDesk Indices calculations.

A proposed ticker as well as the management fee for the product have not been shared yet.

Issuers had initially filed applications for spot ethereum (ETH) ETFs with the staking feature included but removed them in an amended filing later in order to receive approval from the SEC on their proposals.

While the SEC under former Chair Gary Gensler was strictly against staking, issuers have grown more hopeful that they will be able to add the feature to their spot ether funds, among others, with the appointment of crypto-friendly Chair Paul Atkins.

A decision on a February request from Grayscale to allow staking in the Grayscale Ethereum Trust ETF (ETHE) and the Grayscale Ethereum Mini Trust ETF (ETH) was postponed by the regulator just a few days ago.

Uncategorized

Feds Mistakenly Order Estonian HashFlare Fraudsters to Self-Deport Ahead of Sentencing

Just four months ahead of their criminal sentencing for operating a $577 million cryptocurrency mining Ponzi scheme, the two Estonian founders of HashFlare were seemingly mistakenly ordered to self-deport by the U.S. Department of Homeland Security (DHS) — an instruction that directly contradicted a court order for the men to remain in Washington state until they are sentenced in August.

In a joint letter to the court last week, lawyers for Sergei Potapenko and Ivan Turogin told District Judge Robert Lasnik of the Western District of Washington that both men had received “disturbing communications” from DHS ordering them to leave the country immediately.

“It is time for you to leave the United States,” an email to Potapenko and Turogin dated April 11 read. “DHS is terminating your parole. Do not attempt to remain in the United States — the federal government will find you. Please depart the United States immediately.”

The email, included with the letter filed last week, threatened both men with “criminal prosecution, civil fines, and penalties and any other lawful options available to the federal government” if they stayed in the country. It resembles emails that undocumented immigrants and U.S. citizens alike have received over the past few days.

Ironically, Potapenko and Turogin are not in the U.S. of their own volition — they were extradited from their native Estonia at the request of the U.S. Department of Justice in 2022 on an 18-count indictment tied to their HashFlare scheme. Though they initially pleaded not guilty to all charges, in February they both pleaded guilty to one count of conspiracy to commit wire fraud, which carries a maximum sentence of 20 years in prison, and agreed to forfeit over $400 million in assets. They have both been in the Seattle area on bond since last July.

“Although there is nothing Ivan and Sergei would want more than to immediately go home, they understood that they are also under Court order to remain in King County,” wrote Mark Bini, a partner at Reed Smith LLP and lead counsel for Potenko, wrote in the pair’s joint letter to the court. Bini did not respond to CoinDesk’s request for comment.

In his letter, Bini said DHS’s emails had caused both Potapenko and Turogin «significant anxiety.”

“We and our clients have all seen recent news. Immigration authorities make mistakes, and individuals who should not be in custody end up in custody, sometimes even deported to places where they should not be deported,” Bini wrote.

Six days after Bini’s letter to the judge, the DOJ filed its own letter with the court saying that prosecutors had coordinated with DHS’s Homeland Security Investigations (HSI) division and secured a year-long deferral to the self-deportation order.

“This should provide ample time for the sentencing to take place,” the prosecution’s letter said.

DHS did not respond to CoinDesk’s request for comment.

Potapenko and Turogin are slated to be sentenced on August 14 in Seattle. Their lawyers have said that they will request to be sentenced to time served, meaning no additional time in prison, and to be sent home to Estonia “immediately.”

Following last week’s tariff-caused drama, this was a relatively quiet week in crypto. Bitcoin remained stable around $84k. The CoinDesk 20, which tracks about 80% of the market, was up about 4% in the last seven days — i.e. nothing historic.

Still, plenty happened. On Tuesday, much of crypto went offline because of a tech issue at AWS, showing how the decentralized economy isn’t always that decentralized. Shaurya Malwa reported the news early. Bitcoin and other major cryptos slipped on bad news for Nvidia, Omkar Godbole reported.

Mantra, a project focused on real world assets, lost 90% of its value. Explanations varied (the company said it was due to “force liquidations” exchanges).

Meanwhile, EigenLayer, a restaking leader, rolled out a “slashing” feature meant to address security concerns (Sam Kessler reported). OKX, a major exchange, announced plans to set up in California following a $500 million settlement with the SEC over claims it operated previously in the U.S. without a money transmitter license. Cheyenne Ligon had that story.

In less good news, Kraken laid off “hundreds” of staff ahead of an expected IPO. And Coinbase became embroiled in a “front running controversy” linked to a curiously named token on its Base L2. Privacy advocates reacted with alarm to rumors that Binance was about to delist Zcash following a long decline in the value of privacy coins.

In D.C. news, Jesse Hamilton reported on a new wave of crypto lobbyists flooding the capital. Some asked if there are now too many trade groups and whether they really all could be effective.

Friends With Benefits, a buzzy social club for creative technologists, launched a new program to build Web3 products for music, film, publishing and other fun activities. (I wrote that one.)

Of course, there was plenty happening in the economy and markets (Trump’s disgust for Fed chair Powell fed into the unease). But, in crypto, it was pretty much business as usual. Fortunes won, fortunes lost, fortunes deferred.

Canary Capital Files for Tron ETF With Staking Capabilities

Feds Mistakenly Order Estonian HashFlare Fraudsters to Self-Deport Ahead of Sentencing

CoinDesk Weekly Recap: EigenLayer, Kraken, Coinbase, AWS

-

Fashion6 месяцев ago

Fashion6 месяцев agoThese \’90s fashion trends are making a comeback in 2017

-

Entertainment6 месяцев ago

The final 6 \’Game of Thrones\’ episodes might feel like a full season

-

Fashion6 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment6 месяцев ago

The old and New Edition cast comes together to perform

-

Sports6 месяцев ago

Phillies\’ Aaron Altherr makes mind-boggling barehanded play

-

Business6 месяцев ago

Uber and Lyft are finally available in all of New York State

-

Entertainment6 месяцев ago

Disney\’s live-action Aladdin finally finds its stars

-

Sports6 месяцев ago

Steph Curry finally got the contract he deserves from the Warriors