Uncategorized

Strategy Holders Might be at Risk From Michael Saylor’s Financial Wizardry

Is Strategy (MSTR) in trouble?

Led by Executive Chairman Michael Saylor, the firm formerly known as MicroStrategy has vacuumed up 506,137 bitcoin (BTC), currently worth roughly $44 billion at BTC’s current price near $87,000, in the span of about five years. To the casual observer, the company seems to have a magic, unlimited pool of funds from which to draw on to buy more bitcoin. But Strategy acquired a sizable chunk of its stash by issuing billions of dollars in equity and convertible notes (debt securities which can be converted into equity under special conditions), and more recently via the issuance of preferred stock, a type of equity that provides dividends to investors.

However, the price of bitcoin has been pushed down about 20% since peaking above $109,000 two months ago. And though such swings in prices are far from unusual, the particularly aggressive recent purchases by Saylor and team mean Strategy’s average acquisition price has risen to $66,000. The company is really only one more moderate swing down in price from being in the red on its buys.

Which begs the question: Could all of Strategy’s financial wizardry end up backfiring on the company should bitcoin keep heading lower?

“It’s highly unlikely that it results in a scenario where [Strategy] has to liquidate a bunch of bitcoin because it gets margin called,” Quinn Thompson, founder of crypto hedge fund Lekker Capital, told CoinDesk in an interview. “For the most part, the debt is very likely to be able to be refinanced for the convertible notes. And then [the firm] started issuing this perpetual preferred stock, which never has to be repaid.”

In other words, not only is there very little chance that Strategy could suffer the kind of blowup that shook over crypto firms and projects in 2022 (like Genesis or Three Arrows Capital), but the firm has even refrained from posting its bitcoin holdings as collateral for loans — with the exception of a loan taken from Silvergate, which was repaid in 2023.

Even so, that does not necessarily mean that it’s blue skies ahead for MSTR investors, because under various scenarios, Saylor could be forced to issue more equity than the market can handle in order to maintain course.

“If he’s not paying dividends with Strategy’s cash flow, he’s going to issue more shares and wreck the stock price. But it’s no different than what he’s doing already. Every time the retail bids it up, he wrecks the stock price by issuing more shares. In the future, he will have to do that, and the flows might not go into bitcoin. They might go to repay these debtors, and it will hurt the share price,” Thompson said.

Saylor’s balancing act

Strategy currently employs three different methods for raising capital: it can issue equity, convertible notes, or preferred stock.

Issuing equity means that Strategy creates new MSTR shares, sells them on the market, and uses the proceeds to buy bitcoin. Naturally, that creates selling pressure on MSTR and can potentially push the stock downward.

Convertible notes have allowed Strategy to raise funds quickly without diluting MSTR stock. Typically, investors like these notes because they offer a solid yield, they benefit if the stock surges, and they can usually be redeemed in cash for an amount equal to the original investment in addition to interest payments. The tremendous volatility of Strategy’s convertible notes, however, has allowed the company to mostly issue them at a zero percent interest rate and still meet high demand from sophisticated market participants, who have made bank trading that volatility.

Finally, Strategy has begun deploying preferred stocks. These are instruments that tend to appeal to investors seeking lower volatility and more predictable returns through dividends. There are currently two offerings: STRK, which gives an 8% annual return; and STRF, which pays 10% annualized.

But why is Strategy issuing all of these different types of investment vehicles? The idea is to create demand for Strategy for all kinds of investors that may have different tolerances to risk, Jeffrey Park, head of Alpha Strategies at crypto asset management Bitwise, told CoinDesk in an interview.

“The convertible bond investors and the common equity investors were generally aligned in that they were both volatility seeking structures,” Park said. “Preferred equities are different. They actually are favored by investors who want to minimize volatility at all costs for a steady, reliable and high coupon that they feel is worth the credit risk.”

“Strategy’s capital structure is almost like a seesaw in a playground,” Park added. “The common shareholders and converts are on one side, the preferred equity holders are on the other side. As sentiment shifts, the weights move around, and it tilts the value between these securities. But no matter how the seesaw moves, its total weight — which is Strategy’s enterprise value — remains the same. It’s just a redistribution of people’s perceived value across the liabilities that exist on the company’s balance sheet.”

Risks

Even so, Strategy now finds itself in a situation where it must pay 8% dividends on STRK, 10% dividends on STRF, and a blend of 0.4% interest rate on its convertible bonds.

With Strategy’s software business providing very little cash flow, finding the funds to pay for all of these dividends might be tricky.

The company will likely need to keep issuing MSTR stock to pay the interest it owes, Thompson said. “It will hurt the share price. In the most extreme scenario, the stock could trade at a discount [from its bitcoin holdings], because he would be having to issue shares to pay interest and cover cash flow.”

“The really draconian scenario would be for the discount to get so wide, like 20% or 30%, like Grayscale’s GBTC [prior to its conversion into an ETF], that the shareholders riot and tell him to buy back shares and close the discount,” Thompson added. “Right now, he’s adding shareholder value by selling the stock at an elevated price and buying bitcoin, but in the future the reverse might be true, where the best way to add shareholder value would be to sell the bitcoin and buy the stock. But that’s quite far away.”

Saylor lost controlling voting power over the company in 2024 due to the continuous issuance of MSTR stock, meaning that the scenario above could theoretically happen, especially if activist investors decided to get involved.

Another potential risk for MSTR holders is that the 2x long Strategy exchange-traded funds (ETFs) issued by T-Rex and Defiance, MSTX and MSTU, have seen weirdly persistent demand despite the stock’s drawdown. Every time investors want to gain or increase their exposure to these ETFs, the issuers have to buy twice as many MSTR shares. The popularity of these ETFs has helped create constant buying pressure for MSTR — so far, they’ve accumulated over $3 billion in MSTR exposure.

The problem is that the music might stop someday. And if these ETFs begin to sell off their MSTR shares, the reaction on the stock price could be violent.

“I don’t know where the endless capital comes from to buy the dip. These ETFs have gotten obliterated. They’re down huge,” Thompson said. “I mean, this is not a structural move up in the demand curve that you should count on. It’s not something you should really bake into your 10-year predictions of bitcoin price, but as long as it’s existing, it’s important for bitcoin. So I’m continually amazed by it.”

For years, the crypto market has thrived on speculation, where excitement, hype and fleeting trends attract value instead of fundamentals. Investors have continually poured money into tokens fueled by viral moments, chasing rapid gains. Time and again, a select few of these investments soar to incredible heights, only to come crashing down. With over 33 million tokens in circulation, the competition to attract attention gets harder and harder and investor attention is ever more fleeting. But DePIN can change this. With compelling businesses attracting real customers and revenue built on well designed token economics, DePIN can set a new standard of fundamentals in crypto.

As our DePIN Token Economics Report outlines, Decentralized Physical Infrastructure Networks (DePIN) offer a number of compelling businesses with fundamental value. Unlike typical crypto projects driven by speculation, DePIN offers a different approach. It uses blockchain technology to support real-world infrastructure, creating tangible value and generating real revenue. Instead of relying on hype, it builds a financial system based on actual demand, making it a more sustainable and practical model.

Rather than resembling major crypto networks like Bitcoin or Ethereum, DePIN operates more like capital-light marketplaces such as Uber and Airbnb, but with key distinctions. While both models connect providers with customers without funding infrastructure, DePIN providers are compensated in tokens that can appreciate in value, akin to Uber drivers or Airbnb hosts receiving equity. Additionally, most DePINs sell to businesses which eliminates the need for massive marketing expenses required in building a consumer brand.

DePIN offers a compelling business model and, unlike memes that come and go, it is the beginning of crypto’s transformation into a mature, revenue-generating industry.

From Hype to Revenue-Driven Models

At its core, DePIN represents a paradigm shift. Traditionally, blockchain-based businesses have relied on hype to attract buyers. In the absence of traditional fundamentals, the industry cycled through endless metrics such as TPS, TVL, Telegram channel size, followers on X and many others. Many projects have attempted to build decentralized ecosystems. But, without real customers paying for services, they have largely functioned as economies fueled by speculation rather than external demand.

DePIN changes this by integrating blockchain technology with physical and digital infrastructure, creating compelling services that generate revenue. Whether it is decentralized cloud computing, wireless networks, mapping or storage solutions, DePIN projects offer services like traditional businesses and with customers who pay for usage. When combined with the correct token economics, it creates a sustainable financial model.

As DePIN generates growing revenue, it is likely to draw institutional investors who have long been skeptical of crypto’s reliance on hype and speculation. The projects that successfully correlate the token demand to actual business growth will not only survive the current market but also set the standard for the next generation of blockchain companies

The report also highlights one of the most compelling aspects of DePIN, the use of buy-and-burn, which removes the need to have an expanding pool of new buyers. Instead, these projects use a portion of their revenue to repurchase and burn tokens, permanently reducing supply and potentially driving long-term price appreciation similar to stock buybacks.

This approach is in stark contrast to most of crypto which relies on new buyers to sustain and grow their value.The buy-and-burn model ensures that as DePIN businesses grow and generate more revenue, their token ecosystems become more resilient to market fluctuations. Some DePIN tokens are already demonstrating this by decoupling from broader crypto market trends, proving that real-world adoption can lead to price stability and long-term investor confidence.

Aligning Incentives for Sustainable Growth

While DePIN offers significant potential, it also comes with challenges. One major concern is transparency, as most projects lack traditional financial reports, audits, or clear revenue statements. However, blockchain itself provides a solution — on-chain verification through buy-and-burn mechanisms allows for real-time financial tracking, giving investors a clearer picture of a project’s health.

Another challenge is customer adoption. Many businesses and consumers remain concerned due to crypto’s volatility. To address this, DePIN projects are introducing fiat payment options and stablecoin rewards, making it easier for everyday users to interact with these decentralized services without needing prior crypto or Web3 experience.

For DePIN to succeed, its incentive structures must be designed to keep all stakeholders — providers, users, and investors aligned. One way to achieve alignment is through staking mechanisms, especially in cloud-based networks where service providers lock up tokens as collateral to guarantee reliability. Projects like Filecoin and Fluence already use this approach, ensuring accountability while strengthening network security. Others, such as Render and Livepeer, take a different route by distributing a share of network revenue to token stakers, creating a system similar to dividends that rewards long-term commitment.

Governance will also be critical as DePIN projects decentralize. To prevent large token holders from short-term profiteering for quick gains, new governance models like quadratic voting and weighted staking are emerging. These frameworks help keep decision-making balanced, ensuring that projects remain sustainable and fair as they evolve.

DePIN isn’t just another blockchain investment vehicle, it is laying the foundation for real, decentralized infrastructure. While meme coins have shown that crypto can generate hype, they rarely create lasting value. In contrast, DePIN is developing businesses that can compete with centralized companies by focusing on real-world utility.

With token models backed by revenue, deflationary supply mechanics, and increasing interest from institutional investors, DePIN is redefining how blockchain networks should function. The projects that successfully address capital efficiency, align incentives, and navigate regulatory challenges will be the ones that lead this next phase of decentralized technology.

As DePIN matures, its token models will continue to evolve. Optimizing capital efficiency through transparent buy-and-burn rates will ensure liquidity while maintaining long-term value. Governance structures will adapt to prevent short-term actors from derailing network growth. By 2026, DePIN will be recognized as the benchmark for sustainable blockchain economies, proving that crypto can function as more than a speculative asset class.

The crypto industry stands at a crossroads. Investors, developers, and institutions must choose between supporting unsustainable token models or supporting projects that create real value. For the space to mature, it needs to move beyond pure speculation, and DePIN is at the forefront of that transformation.

Market Recovery Amid Institutional Confidence

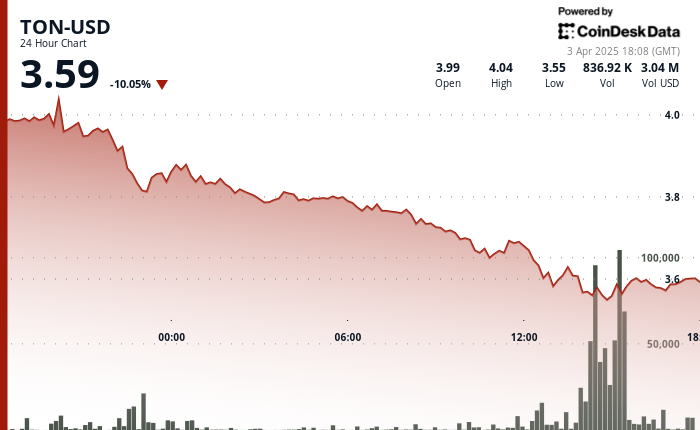

The cryptocurrency market remains in turbulent territory as Toncoin (TON) demonstrates both significant volatility and remarkable resilience.

After forming a head-and-shoulders pattern with strong resistance at $4.15, TON has recovered from its recent lows. It is now trading at $4.13 with a 12.5% weekly gain.

This recovery comes amid news that leading venture capital firms, including Sequoia, Ribbit Capital, and Benchmark, collectively hold over $400 million in TON, signaling institutional confidence in the blockchain’s future.

TON Technical Analysis Highlights

Price action formed a head-and-shoulders pattern with resistance at $4.15 and support at $3.60.

The support level at $3.60 was breached during the April 3rd selloff.

Volume analysis shows distribution phases coinciding with price peaks, suggesting institutional profit-taking.

Fibonacci retracement indicates potential stabilization around the 0.618 level at $3.58.

Cup-and-handle formation appeared during recovery with initial resistance at $3.58.

Strong buying pressure was observed during the 15:32-15:34 and 15:58 periods.

Price reclaimed the Fibonacci 0.382 level at $3.59, suggesting potential continuation toward $3.65.

Disclaimer: This article was generated with AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy. This article may include information from external sources, which are listed below when applicable.

TheNewsCrypto, “Toncoin (TON) Eyes $4 as Bullish Momentum Builds,” accessed April 3, 2025

CryptoNews, “Is This the Next Solana? Toncoin’s $400 Million VC Investment Surge Signals Explosive Upside,” accessed April 3, 2025

CryptoDaily, “AI Predicts 12,500% Gains for Remittix (RTX), 232% for Chainlink (LINK) — But to Sell Toncoin (TON), Shiba Inu (SHIB) Fast,” accessed April 3, 2025

TheNewsCrypto, “Toncoin (TON) Price Prediction,” accessed April 3, 2025

Bitcoin Sistemi, “Top Crypto Platforms: Binance Coin, BlockDAG, Tron, Toncoin Poised for Major Growth in 2025,” accessed April 3, 2025

Hidden Road, a prime broker that focuses on both crypto and traditional assets, has received an inbound takeover approach, according to two people with knowledge of the matter.

Takeover talks are ongoing with a crypto native company that wants to acquire Hidden Road, the people said, but there is no certainty that any deal will be done.

Hidden Road declined to comment.

The company has raised about $50 million in the last 12 months, from investors including crypto venture capital firm Dragonfly Capital, one of the people said.

One of the investors, a crypto native firm, has since made an approach to buy Hidden Road, the person added.

Dragonfly Capital didn’t respond to a request for comment by publication time.

Prime brokers are an essential part of the plumbing of financial markets. They provide trading, financing and custody services to large institutions.

Hidden Road raised $50 million in a Series A funding round in July 2022. The round was led by Castle Island Ventures, with participation from Citadel Securities, FTX Ventures, Uncorrelated Ventures, Greycroft, XBTO Humla Ventures, Wintermute, SLN Capital, Profluent Trading, Coinbase Ventures and Corner Capital.

The company was said to be weighing options including a potential sale or capital raise that could value the firm at more than $1 billion, according to a Bloomberg report last month.

-

Fashion6 месяцев ago

Fashion6 месяцев agoThese \’90s fashion trends are making a comeback in 2017

-

Entertainment6 месяцев ago

The final 6 \’Game of Thrones\’ episodes might feel like a full season

-

Fashion6 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment6 месяцев ago

The old and New Edition cast comes together to perform

-

Sports6 месяцев ago

Phillies\’ Aaron Altherr makes mind-boggling barehanded play

-

Entertainment6 месяцев ago

Disney\’s live-action Aladdin finally finds its stars

-

Business6 месяцев ago

Uber and Lyft are finally available in all of New York State

-

Sports6 месяцев ago

Steph Curry finally got the contract he deserves from the Warriors