Uncategorized

The Future of Crypto Enforcement in the U.S.

Having served as the first chief of the SEC’s crypto unit from 2017 to 2019, I’m often asked what kind of crypto enforcement we should expect to see from the new administration. My first answer is that I do not know. My second answer is that I believe it will be different, but it will not disappear.

To anticipate the future of crypto enforcement, we should begin by reviewing the past.

The beginning

The SEC’s crypto enforcement unit was formed in 2017 during the first Trump Administration. The early focus was on one, fraud, and two, core capital raising events. Regulation of capital raising is the principal purpose of the Securities Act of 1933. When an investor gives money to an entrepreneur who will use it in a business to generate profit, the investor is entitled to certain information about the business. Early crypto investigations were focused on this fundraising activity, which was usually in the form of an unregistered initial coin offering (“ICO”). The idea was that many ICOs at that time were not so different in substance than equity or debt offerings, and should be regulated similarly.

The industry responded responsibly and now, crypto entrepreneurs often raise money in compliance with the federal securities laws. In one of several options, some offerings are exempt from SEC registration because they are limited to accredited investors. The entrepreneurs then use the capital to build a blockchain protocol or other crypto product. Once built, sales of tokens probably are not securities offerings because people are not buying tokens as an investment in someone’s business. Even if there is hope for profit, that profit would come from the activities of the buyers and other participants, not the efforts of a central business manager.

The last four years

During the last four years, the SEC has focused more of its enforcement activity on secondary markets such as centralized trading platforms and decentralized protocols. It is less clear how the federal securities laws apply to these markets. These transactions generally do not involve a central entrepreneur collecting money from investors and using it in a business. Instead, there are thousands or even millions of crypto participants interacting with each other, sometimes anonymously via autonomous software. Token buyers might not know who sold them tokens and there may be no central actor that’s key to future success. Federal district courts have reached different conclusions and there are reports that the SEC might drop one of these key cases.

More broadly, enforcement became the dominant focus of SEC regulation. The SEC doubled the size of the crypto unit, creating new supervisory and trial attorney positions. It spent years and a tremendous amount of resources litigating several non-fraud cases. Many additional non-unit lawyers worked on crypto investigations, and crypto appeared to be the main focus of SEC enforcement.

This approach did not generate useful guidance to the industry. Many SEC rules have technical aspects that are incompatible with the anonymous decentralized ledger that is blockchain technology. Under the enforcement approach of recent years, the very premise of the technology was treated not as a feature, but as a bug. The result was existential enforcement risk to a burgeoning industry and economic activity being pushed offshore.

The future

I do not believe the crypto industry wants a Wild West of no regulation. They want a sensible rulebook that makes compliance feasible, and they also want regulators to crack down on fraud. No legitimate actor benefits from fraud in the industry.

What does this mean for the next four years of enforcement?

First, enforcement is just one component of regulation. We likely will see increased resources dedicated to the other parts of effective regulation — new guidance and rules that offer an achievable regulatory framework. Acting SEC Chairman Mark Uyeda recently announced a new crypto task force for developing a “sensible regulatory path,” and Commissioner Hester Peirce, who will lead the task force, included in her objectives “preserv[ing] industry’s ability to offer products and services.” The dedicated crypto unit also has been reduced in size and repurposed to cyber and emerging technologies, with many staff returning to general enforcement duties.

Second, we could see a renewed focus on fighting fraud. The Commission did not stop bringing crypto fraud cases during the last four years, but many headline cases were non-fraud regulatory disputes. That might change; as Commissioner Peirce said in her objectives speech, “We do not tolerate liars, cheaters, and scammers.”

Third, once there is a new rulebook, we can expect the SEC to enforce those rules. That will take time. We might see a transition period, with some non-fraud cases but more focus on writing the new rulebook. Once adopted, enforcement of that rulebook could come after a fair notice period for the industry to adapt to it.

Conclusion

I expect SEC crypto enforcement to continue, but with different priorities. Investor protection will be balanced with the SEC’s co-equal mandates of facilitating capital formation and maintaining orderly markets. The crypto industry is filled with good actors who want to be compliant; they just need a rulebook that makes compliance achievable. A renewed approach will allow the industry to grow without abandoning investor protection.

The SEC has been the most assertive crypto regulator so far, but it is not alone. Other federal agencies may emerge as co-equal regulatory leaders, either through legislation or otherwise, especially if the SEC no longer takes the position that every cryptocurrency (except Bitcoin) is a security. Some state authorities have been active in crypto, and that likely will continue or even increase.

A client recently reminded me that there will be another election in four years. The new regulatory approach, and the industry’s business and product decisions, must be durable. If they are not, the renewed approach to crypto over the next four years could be undone as easily as that of the last four years.

Wall Street giant Citigroup (C) has launched new ether (ETH) forecasts, calling for $4,300 by year-end, which would be a decline from the current $4,515.

That’s the base case though. The bank’s full assessment is wide enough to drive an army regiment through, with the bull case being $6,400 and the bear case $2,200.

The bank analysts said network activity remains the key driver of ether’s value, but much of the recent growth has been on layer-2s, where value “pass-through” to Ethereum’s base layer is unclear.

Citi assumes just 30% of layer-2 activity contributes to ether’s valuation, putting current prices above its activity-based model, likely due to strong inflows and excitement around tokenization and stablecoins.

A layer 1 network is the base layer, or the underlying infrastructure of a blockchain. Layer 2 refers to a set of off-chain systems or separate blockchains built on top of layer 1s.

Exchange-traded fund (ETF) flows, though smaller than bitcoin’s (BTC), have a bigger price impact per dollar, but Citi expects them to remain limited given ether’s smaller market cap and lower visibility with new investors.

Macro factors are seen adding only modest support. With equities already near the bank’s S&P 500 6,600 target, the analysts do not expect major upside from risk assets.

Read more: Ether Bigger Beneficiary of Digital Asset Treasuries Than Bitcoin or Solana: StanChart

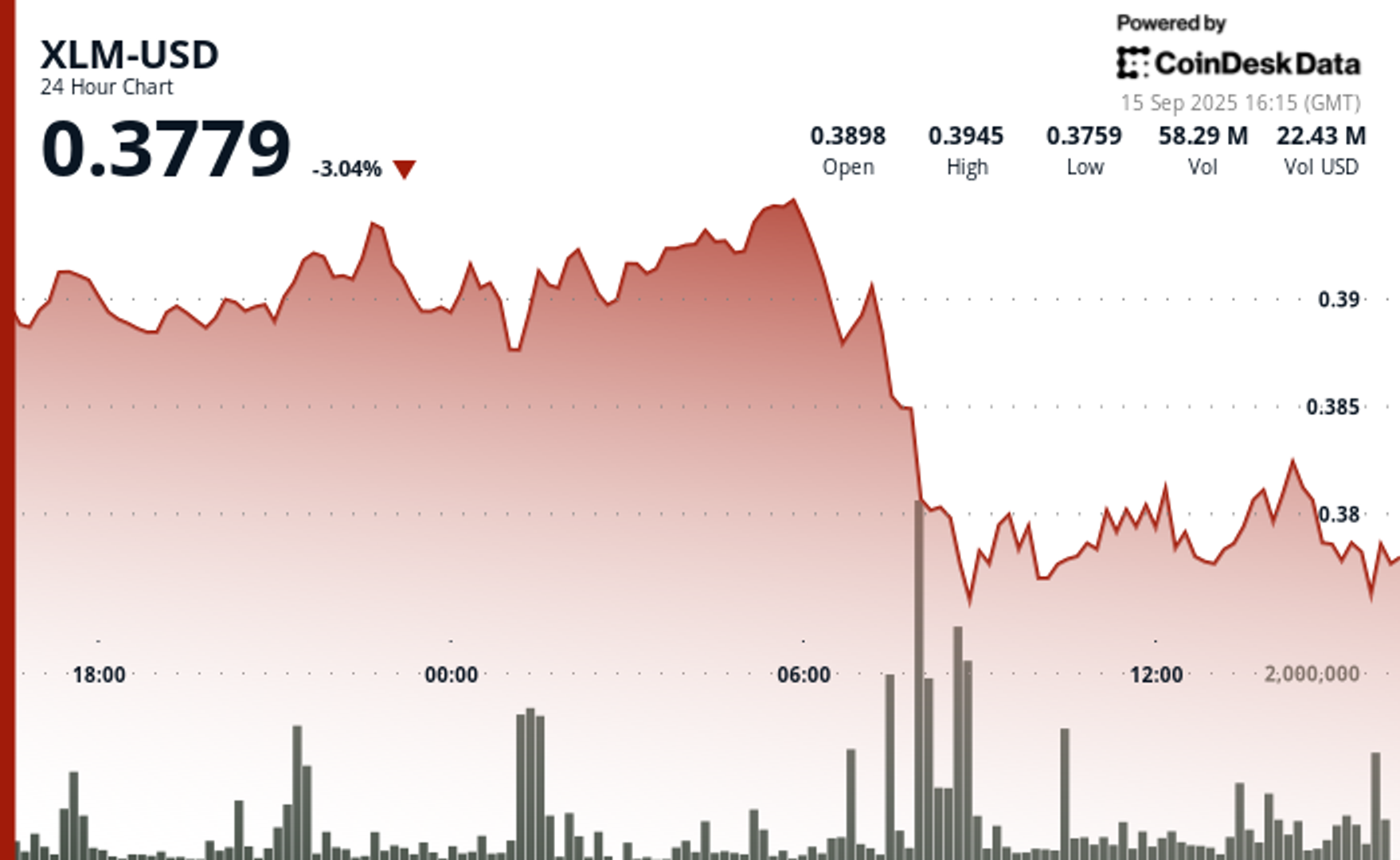

Stellar’s XLM token endured sharp swings over the past 24 hours, tumbling 3% as institutional selling pressure dominated order books. The asset declined from $0.39 to $0.38 between September 14 at 15:00 and September 15 at 14:00, with trading volumes peaking at 101.32 million—nearly triple its 24-hour average. The heaviest liquidation struck during the morning hours of September 15, when XLM collapsed from $0.395 to $0.376 within two hours, establishing $0.395 as firm resistance while tentative support formed near $0.375.

Despite the broader downtrend, intraday action highlighted moments of resilience. From 13:15 to 14:14 on September 15, XLM staged a brief recovery, jumping from $0.378 to a session high of $0.383 before closing the hour at $0.380. Trading volume surged above 10 million units during this window, with 3.45 million changing hands in a single minute as bulls attempted to push past resistance. While sellers capped momentum, the consolidation zone around $0.380–$0.381 now represents a potential support base.

Market dynamics suggest distribution patterns consistent with institutional profit-taking. The persistent supply overhead has reinforced resistance at $0.395, where repeated rally attempts have failed, while the emergence of support near $0.375 reflects opportunistic buying during liquidation waves. For traders, the $0.375–$0.395 band has become the key battleground that will define near-term direction.

")

Technical Indicators

- XLM retreated 3% from $0.39 to $0.38 during the previous 24-hours from 14 September 15:00 to 15 September 14:00.

- Trading volume peaked at 101.32 million during the 08:00 hour, nearly triple the 24-hour average of 24.47 million.

- Strong resistance established around $0.395 level during morning selloff.

- Key support emerged near $0.375 where buying interest materialized.

- Price range of $0.019 representing 5% volatility between peak and trough.

- Recovery attempts reached $0.383 by 13:00 before encountering selling pressure.

- Consolidation pattern formed around $0.380-$0.381 zone suggesting new support level.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

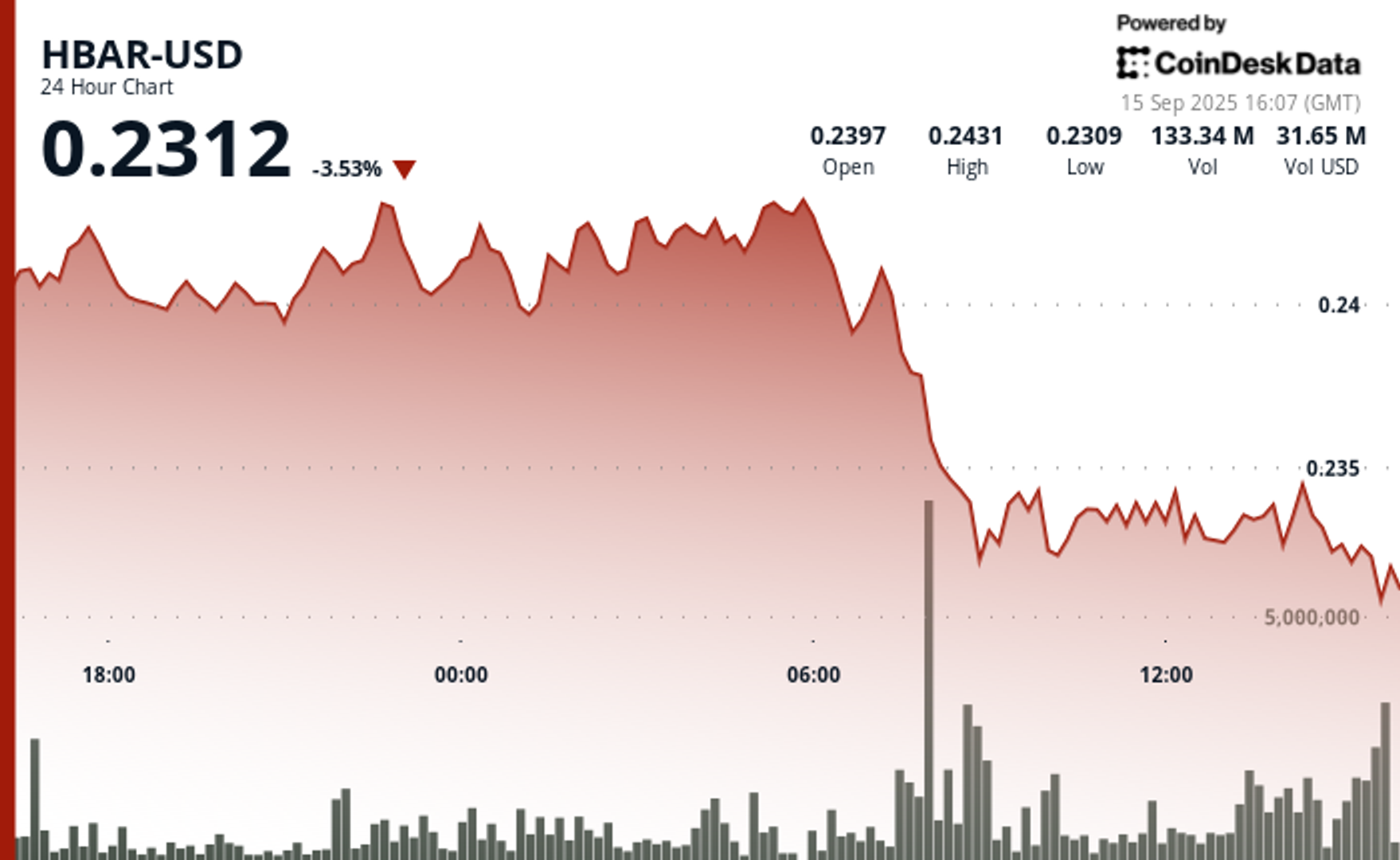

Hedera Hashgraph’s HBAR token endured steep losses over a volatile 24-hour window between September 14 and 15, falling 5% from $0.24 to $0.23. The token’s trading range expanded by $0.01 — a move often linked to outsized institutional activity — as heavy corporate selling overwhelmed support levels. The sharpest move came between 07:00 and 08:00 UTC on September 15, when concentrated liquidation drove prices lower after days of resistance around $0.24.

Institutional trading volumes surged during the session, with more than 126 million tokens changing hands on the morning of September 15 — nearly three times the norm for corporate flows. Market participants attributed the spike to portfolio rebalancing by large stakeholders, with enterprise adoption jitters and mounting regulatory scrutiny providing the backdrop for the selloff.

Recovery efforts briefly emerged during the final hour of trading, when corporate buyers tested the $0.24 level before retreating. Between 13:32 and 13:35 UTC, one accumulation push saw 2.47 million tokens deployed in an effort to establish a price floor. Still, buying momentum ultimately faltered, with HBAR settling back into support at $0.23.

The turbulence underscores the token’s vulnerability to institutional distribution events. Analysts point to the failed breakout above $0.24 as confirmation of fresh resistance, with $0.23 now serving as the critical support zone. The surge in volume suggests major corporate participants are repositioning ahead of regulatory shifts, leaving HBAR’s near-term outlook dependent on whether enterprise buyers can mount sustained defenses above key support.

")

Technical Indicators Summary

- Corporate resistance levels crystallized at $0.24 where institutional selling pressure consistently overwhelmed enterprise buying interest across multiple trading sessions.

- Institutional support structures emerged around $0.23 levels where corporate buying programs have systematically absorbed selling pressure from retail and smaller institutional participants.

- The unprecedented trading volume surge to 126.38 million tokens during the 08:00 morning session reflects enterprise-scale distribution strategies that overwhelmed corporate demand across major trading platforms.

- Subsequent institutional momentum proved unsustainable as systematic selling pressure resumed between 13:37-13:44, driving corporate participants back toward $0.23 support zones with sustained volumes exceeding 1 million tokens, indicating ongoing institutional distribution.

- Final trading periods exhibited diminishing corporate activity with zero recorded volume between 13:13-14:14, suggesting institutional participants adopted defensive positioning strategies as HBAR consolidated at $0.23 amid enterprise uncertainty.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

Wall Street Bank Citigroup Sees Ether Falling to $4,300 by Year-End

XLM Sees Heavy Volatility as Institutional Selling Weighs on Price

HBAR Tumbles 5% as Institutional Investors Trigger Mass Selloff

-

Business11 месяцев ago

Business11 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion11 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment11 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment11 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment11 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Business11 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment11 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton

-

Entertainment11 месяцев ago

Disney\’s live-action Aladdin finally finds its stars