Uncategorized

All Eyes on Bitcoin

Bitcoin saw explosive growth immediately after the recent U.S. presidential elections, rising and retaking the spotlight from former highs of $73,000 in March. Now the question is, will bitcoin (BTC) continue its uptrend, and at what point can a sharp reversal happen?

If we take a look at former BTC market cycles, which happen every four years, then we see that we are now just starting to go into new bitcoin price discovery areas, and BTC could top out at new all-time highs, which is practically anything greater than the current resistance of $92,000. Bitcoin could even potentially see highs of $140,000+ based on prior supply and demand — i.e. halving cycles. On the contrary, what makes this market cycle a bit different than others is the vanished principle of BTC being an inflation hedge or digital gold. In theory, it was supposed to be — that is, at least, likely what Satoshi intended since bitcoin was created after the 2008 financial crisis. From what we saw in the last cryptocurrency bear market cycle, BTC is not an actual inflation hedge and performs like all other risk-on assets, so sentiment could change once the inauguration happens in January.

As we’ve seen before, politics could potentially just be politics until we see actual regulatory rollouts and a more favorable U.S. stance on paper with policies and laws that the markets fully embrace. Things seem to be going in the right direction with the news of Gensler resigning come January 20, 2025. The question remains on who will be his replacement; the wrong person and the smallest sentiment change in the wrong direction could fully accelerate a drawdown in BTC. We’ve previously seen what every Fed meeting minute has done to the price action of crypto which has, up until recently, always been negatively perceived. In other words, we are not fully out of the woods just yet, especially until there is clarity on who could be Gensler’s replacement.

The BTC ETFs played a vital role this year in institutionalizing the cryptocurrency, which allowed for RIA and fiduciary investment in bitcoin, although in a turnaround market the same volumes that helped bitcoin get to the point it is at today can be the same volumes and outflows that present a downfall. This can lead to crippling sentiment as we all know the crypto bull market does not last forever and drawdowns of 70-80% can be expected.

Looking at prior BTC bull market cycles, BTC has seen drawdowns of 20-30%. Can the same be expected with all the new factors under the current and new market structure? Analysts assume less drawdown and volatility scenarios due to the BTC ETF options offered by iShares and others, although on the contrary, systematic strategies still seem to be sought after with investors taking bets on market volatility, which only recently (in 2022) saw an equity market-like expansion in the crypto markets where enough volume, market cap, and stability existed for the shorting functionality of some coins.

With more market participants and more avenues of shorting functionality across all crypto assets, including BTC, this can create more volatility in the short-term. Compared to the last market cycle, there are a lot more traditional finance (TradFi) players trading and market making in the space now, which in a way is offset by more institutional capital locked up (mostly in ETFs since the venture space in crypto dried up from the fast money of the last bull market). Although in a way, no matter how much institutional capital enters the space, the market cycle of BTC will follow volatility— it’s just in its decentralized nature.

Regardless of whatever outlook one has on the price of BTC, it’s important to realize that this is a different market than before. Gone are the days of quick “hot money” returns with the inevitable crypto risk factors ever present. One must remain cautious, but optimistic, on where things are going, if not bullish on the market cycle and structure alone. Regardless, for every type of investor, there is a huge opportunity due to the immense growth of the industry, and when that window will close is anyone’s guess — the only thing for certain is that the new market cycle is just getting started.

Good Morning, Asia. Here’s what’s making news in the markets:

Welcome to Asia Morning Briefing, a daily summary of top stories during U.S. hours and an overview of market moves and analysis. For a detailed overview of U.S. markets, see CoinDesk’s Crypto Daybook Americas.

Bitcoin (BTC) traded just above $115k in Asia Tuesday morning, slipping slightly after a strong start to the week.

The modest pullback followed a run of inflows into U.S. spot ETFs and lingering optimism that the Federal Reserve will cut rates next week. The moves left traders divided: is this recovery built on fragile foundations, or is crypto firmly back on track after last week’s CPI-driven jitters?

That debate is playing out across research desks. Glassnode’s weekly pulse emphasizes fragility. While ETF inflows surged nearly 200% last week and futures open interest jumped, the underlying spot market looks weak.

Buying conviction remains shallow, Glassnode writes, funding rates have softened, and profit-taking is on the rise with more than 92% of supply in profit.

Options traders have also scaled back downside hedges, pushing volatility spreads lower, which Glassnode warns leaves the market exposed if risk returns. The core message: ETFs and futures are supporting the rally, but without stronger spot flows, BTC remains vulnerable.

QCP takes the other side.

The Singapore-based desk says crypto is “back on track” after CPI confirmed tariff-led inflation without major surprises. They highlight five consecutive days of sizeable BTC ETF inflows, ETH’s biggest inflow in two weeks, and strength in XRP and SOL even after ETF delays.

Traders, they argue, are interpreting regulatory postponements as inevitability rather than rejection. With the Altcoin Season Index at a 90-day high, QCP sees BTC consolidation above $115k as the launchpad for rotation into higher-beta assets.

The divide underscores how Bitcoin’s current range near $115k–$116k is a battleground. Glassnode calls it fragile optimism; QCP calls it momentum. Which side is right may depend on whether ETF inflows keep offsetting profit-taking in the weeks ahead.

")

Market Movement

BTC: Bitcoin is consolidating near the $115,000 level as traders square positions ahead of expected U.S. Fed policy moves; institutional demand via spot Bitcoin ETFs is supporting upside

ETH: ETH is trading near $4500 in a key resistance band; gains are being helped by renewed institutional demand, tightening supply (exchange outflows), and positive technical setups.

Gold: Gold continues to hold near record highs, underpinned by expectations of Fed interest rate cuts, inflation risk, and investor demand for safe havens; gains tempered somewhat by profit‑taking and a firmer U.S. dollar

Nikkei 225: Japan’s Nikkei 225 topped 45,000 for the first time Monday, leading Asia-Pacific gains as upbeat U.S.-China trade talks and a TikTok divestment framework lifted sentiment.

S&P 500: The S&P 500 rose 0.5% to close above 6,600 for the first time on Monday as upbeat U.S.-China trade talks and anticipation of a Fed meeting lifted stocks.

Elsewhere in Crypto

Wall Street giant Citigroup (C) has launched new ether (ETH) forecasts, calling for $4,300 by year-end, which would be a decline from the current $4,515.

That’s the base case though. The bank’s full assessment is wide enough to drive an army regiment through, with the bull case being $6,400 and the bear case $2,200.

The bank analysts said network activity remains the key driver of ether’s value, but much of the recent growth has been on layer-2s, where value “pass-through” to Ethereum’s base layer is unclear.

Citi assumes just 30% of layer-2 activity contributes to ether’s valuation, putting current prices above its activity-based model, likely due to strong inflows and excitement around tokenization and stablecoins.

A layer 1 network is the base layer, or the underlying infrastructure of a blockchain. Layer 2 refers to a set of off-chain systems or separate blockchains built on top of layer 1s.

Exchange-traded fund (ETF) flows, though smaller than bitcoin’s (BTC), have a bigger price impact per dollar, but Citi expects them to remain limited given ether’s smaller market cap and lower visibility with new investors.

Macro factors are seen adding only modest support. With equities already near the bank’s S&P 500 6,600 target, the analysts do not expect major upside from risk assets.

Read more: Ether Bigger Beneficiary of Digital Asset Treasuries Than Bitcoin or Solana: StanChart

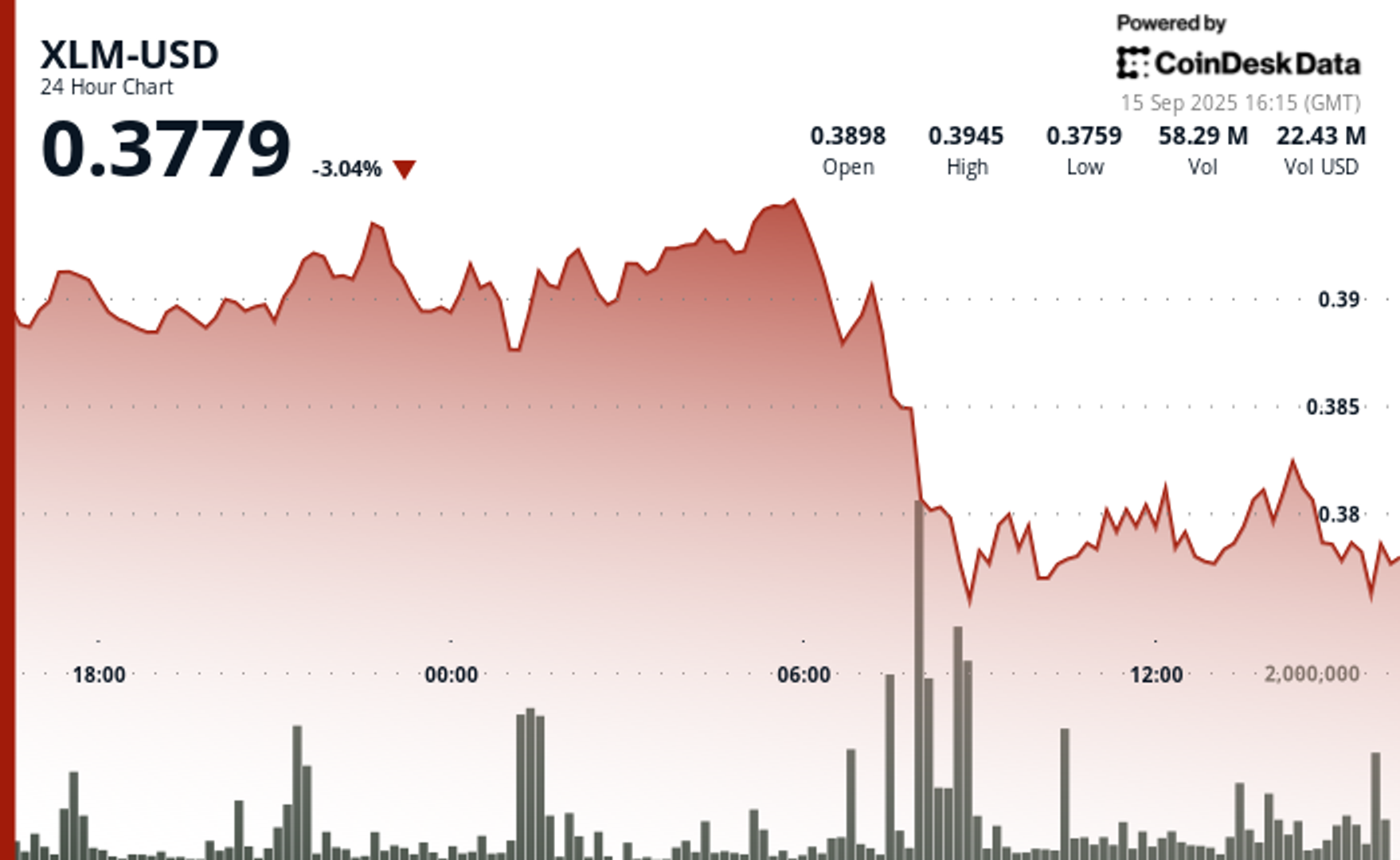

Stellar’s XLM token endured sharp swings over the past 24 hours, tumbling 3% as institutional selling pressure dominated order books. The asset declined from $0.39 to $0.38 between September 14 at 15:00 and September 15 at 14:00, with trading volumes peaking at 101.32 million—nearly triple its 24-hour average. The heaviest liquidation struck during the morning hours of September 15, when XLM collapsed from $0.395 to $0.376 within two hours, establishing $0.395 as firm resistance while tentative support formed near $0.375.

Despite the broader downtrend, intraday action highlighted moments of resilience. From 13:15 to 14:14 on September 15, XLM staged a brief recovery, jumping from $0.378 to a session high of $0.383 before closing the hour at $0.380. Trading volume surged above 10 million units during this window, with 3.45 million changing hands in a single minute as bulls attempted to push past resistance. While sellers capped momentum, the consolidation zone around $0.380–$0.381 now represents a potential support base.

Market dynamics suggest distribution patterns consistent with institutional profit-taking. The persistent supply overhead has reinforced resistance at $0.395, where repeated rally attempts have failed, while the emergence of support near $0.375 reflects opportunistic buying during liquidation waves. For traders, the $0.375–$0.395 band has become the key battleground that will define near-term direction.

")

Technical Indicators

- XLM retreated 3% from $0.39 to $0.38 during the previous 24-hours from 14 September 15:00 to 15 September 14:00.

- Trading volume peaked at 101.32 million during the 08:00 hour, nearly triple the 24-hour average of 24.47 million.

- Strong resistance established around $0.395 level during morning selloff.

- Key support emerged near $0.375 where buying interest materialized.

- Price range of $0.019 representing 5% volatility between peak and trough.

- Recovery attempts reached $0.383 by 13:00 before encountering selling pressure.

- Consolidation pattern formed around $0.380-$0.381 zone suggesting new support level.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

Asia Morning Briefing: Fragility or Back on Track? BTC Holds the Line at $115K

Wall Street Bank Citigroup Sees Ether Falling to $4,300 by Year-End

XLM Sees Heavy Volatility as Institutional Selling Weighs on Price

-

Business11 месяцев ago

Business11 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion11 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment11 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment11 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment11 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Business11 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment11 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton

-

Entertainment11 месяцев ago

Disney\’s live-action Aladdin finally finds its stars