Uncategorized

Tornado of Administrative Overreach: Challenging Sanctions of Crypto Mixing Services

Cryptocurrency transactions are often anonymous, but they’re not private. In fact, they’re quite public. Anyone with the right technical know-how can see every transaction ever made on most publicly accessible blockchains.

This radical transparency and traceability has made it easier (contrary to popular belief) for law enforcement to track stolen and laundered cryptocurrency across various transactions. But it has also made it easier for criminal crypto actors to trace certain transactions, and — by collecting enough data points — recognize the real-world identity of crypto users who would otherwise remain anonymous.

Dramatic stories abound about violent home invasions targeting those with large cryptocurrency holdings or hackers targeting those who donate to controversial causes. More mundanely, those who accept cryptocurrency as payment for goods or services might not want the person paying them to know their entire on-chain financial history with only a few clicks.

Recognizing these realities, crypto-mixing services sprung to life. The technical details can differ dramatically, but essentially these services act as intermediaries, mixing together crypto transactions to make them more difficult, if not impossible, to track. Some mixing services actually take custody of the cryptocurrency, mix the funds together, and then distribute them to pre-determined places. Others rely instead on smart contracts (pre-written computer code) to do this for them. Created in 2019, popular crypto-mixing service Tornado Cash falls into this latter category.

For the same reasons these services appeal to legitimate users (privacy and making transactions harder to track), they also appeal to criminals and hostile foreign state actors such as North Korea. Knowing this, the Treasury Department’s Office of Foreign Assets Control (OFAC) imposed sanctions that would prohibit “U.S. persons” from engaging in transactions with, or using, some of these mixing services, including Tornado Cash.

But does OFAC have the authority to do this, particularly when it comes to smart-contract-based services such as Tornado Cash?

In two similar lawsuits — one pending in the Fifth Circuit and one pending in the Eleventh Circuit — a series of plaintiffs are arguing that it does not, saying that OFAC’s decision involves “an unprecedented exercise of [its] authority.” To understand why, we need to back up and understand precisely what Congress has said.

For starters, it makes sense that Americans wouldn’t want criminals or foreign adversaries using the U.S. financial system to accomplish their nefarious goals. So, Congress empowered the president to use a panoply of broad economic tools to stop them from doing so. The president in turn delegated his authority to impose and exercise these economic sanctions to the Secretary of the Treasury who in turn delegated much of the responsibility to OFAC for implementing them.

As relevant here, Congress passed two laws that authorize the president and those to whom he has delegated authority, to act. The International Emergency Economic Powers Act (IEEPA) empowers the chief executive (who has delegated his authority all the way down to OFAC) to block “any property in which any foreign country or a national thereof has any interest” when certain other specified conditions are met. Another act, the North Korea Sanctions and Policy Enhancement Act, allows the president to sanction the “property and interest in property” of “any person” who engaged in specified conduct.

While national security concerns pervade the cases challenging OFAC’s actions, fundamentally the cases are about statutory interpretation. What do the terms “person,” “property,” and “interest in property” mean in plain English so that courts can decide whether Congress gave the President — and OFAC — the power to impose sanctions on Tornado Cash?

In the wake of the U.S. Supreme Court’s Loper Bright decision, courts must decide for themselves what these terms mean without giving deference to the agency’s interpretation.

Of course, the plaintiffs in these lawsuits argue that these aren’t obscure technical terms. And they argue that “text, precedent, and history” support their position that OFAC exceeded its authority in placing the Tornado Cash entity it designated on the sanctions list — largely because of how Tornado Cash operates and is structured.

They argue, essentially, that OFAC didn’t properly identify any person — which can include an entity (though they argue there isn’t one in this case) — didn’t properly identify any property because the open-source immutable smart contracts (computer code) at issue here aren’t capable of being owned, and didn’t properly identify any interest in property, as traditionally understood to mean a “legal or equitable claim to or right in property.”

In part, this stems from the fact that there’s confusion over what exactly constitutes “Tornado Cash.” While the government referred to an amalgamation of entities and individuals, the plaintiffs say that “[n]obody besides the government call these people ‘Tornado Cash’” and others instead typically use Tornado Cash to refer to the smart contracts underlying the mixing service.

Essentially, there’s the (Ethereum) blockchain on which the smart contracts run , the developers who initially programmed the smart contracts, the smart contracts themselves, and a decentralized autonomous organization (DAO) that has many members that vote and takes actions related to the smart contracts but that doesn’t own or control the smart contracts themselves since they are unchangeable open-source software code.

The plaintiffs say that by allowing OFAC to break free from the traditional widely accepted understanding of “person,” “property,” and “interest in property,” OFAC’s “sanctions authority would be nearly limitless.” The plaintiffs say that if OFAC’s sanctions are allowed to stand, “every American citizen may be prohibited from executing those lines of code to make political donations, start business ventures, or develop new software features.” They also make clear that OFAC “cannot ban Americans from transacting only with fellow Americans or with their own property,” yet they say that’s exactly what has happened here.

Both district courts considering these issues disagreed and found that OFAC had acted lawfully in imposing the sanctions. At a recent oral argument in the Fifth Circuit case, however, the appellate judges seemed skeptical. And the appellate judges in the Eleventh Circuit case asked tough questions too.

Due process and First Amendment concerns have been brought up in varying degrees in both cases. There’s also questions about what role, if any, the rule of lenity and the Major Questions Doctrine should play. And, even more to the point, there’s questions with larger implications for the crypto community such as whether a smart contract (computer code) can be a unilateral contract and whether a DAO standing alone can be thought of as an unincorporated association or even a general partnership with liability for some or all of its members.

With all of these lingering questions, one thing is clear: Congress should be the entity to respond to the changing circumstances brought about by new technology rather than an administrative agency such as OFAC. Current law shouldn’t be stretched in new and novel ways beyond its proper bounds to fit new circumstances.

On that much, we should all agree. Otherwise, OFAC and other agencies will continue to assert even more constitutionally questionable authority.

Wall Street giant Citigroup (C) has launched new ether (ETH) forecasts, calling for $4,300 by year-end, which would be a decline from the current $4,515.

That’s the base case though. The bank’s full assessment is wide enough to drive an army regiment through, with the bull case being $6,400 and the bear case $2,200.

The bank analysts said network activity remains the key driver of ether’s value, but much of the recent growth has been on layer-2s, where value “pass-through” to Ethereum’s base layer is unclear.

Citi assumes just 30% of layer-2 activity contributes to ether’s valuation, putting current prices above its activity-based model, likely due to strong inflows and excitement around tokenization and stablecoins.

A layer 1 network is the base layer, or the underlying infrastructure of a blockchain. Layer 2 refers to a set of off-chain systems or separate blockchains built on top of layer 1s.

Exchange-traded fund (ETF) flows, though smaller than bitcoin’s (BTC), have a bigger price impact per dollar, but Citi expects them to remain limited given ether’s smaller market cap and lower visibility with new investors.

Macro factors are seen adding only modest support. With equities already near the bank’s S&P 500 6,600 target, the analysts do not expect major upside from risk assets.

Read more: Ether Bigger Beneficiary of Digital Asset Treasuries Than Bitcoin or Solana: StanChart

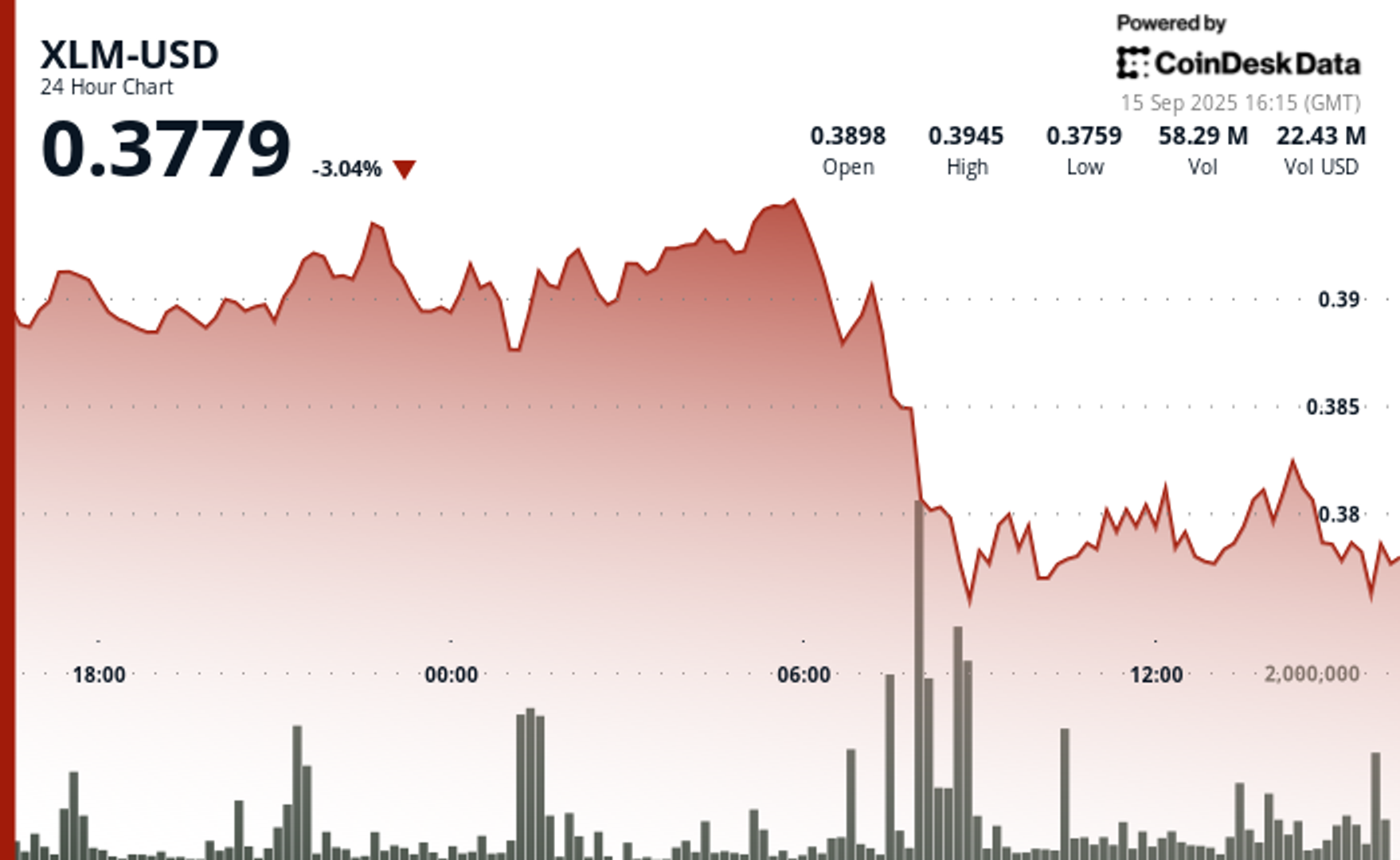

Stellar’s XLM token endured sharp swings over the past 24 hours, tumbling 3% as institutional selling pressure dominated order books. The asset declined from $0.39 to $0.38 between September 14 at 15:00 and September 15 at 14:00, with trading volumes peaking at 101.32 million—nearly triple its 24-hour average. The heaviest liquidation struck during the morning hours of September 15, when XLM collapsed from $0.395 to $0.376 within two hours, establishing $0.395 as firm resistance while tentative support formed near $0.375.

Despite the broader downtrend, intraday action highlighted moments of resilience. From 13:15 to 14:14 on September 15, XLM staged a brief recovery, jumping from $0.378 to a session high of $0.383 before closing the hour at $0.380. Trading volume surged above 10 million units during this window, with 3.45 million changing hands in a single minute as bulls attempted to push past resistance. While sellers capped momentum, the consolidation zone around $0.380–$0.381 now represents a potential support base.

Market dynamics suggest distribution patterns consistent with institutional profit-taking. The persistent supply overhead has reinforced resistance at $0.395, where repeated rally attempts have failed, while the emergence of support near $0.375 reflects opportunistic buying during liquidation waves. For traders, the $0.375–$0.395 band has become the key battleground that will define near-term direction.

")

Technical Indicators

- XLM retreated 3% from $0.39 to $0.38 during the previous 24-hours from 14 September 15:00 to 15 September 14:00.

- Trading volume peaked at 101.32 million during the 08:00 hour, nearly triple the 24-hour average of 24.47 million.

- Strong resistance established around $0.395 level during morning selloff.

- Key support emerged near $0.375 where buying interest materialized.

- Price range of $0.019 representing 5% volatility between peak and trough.

- Recovery attempts reached $0.383 by 13:00 before encountering selling pressure.

- Consolidation pattern formed around $0.380-$0.381 zone suggesting new support level.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

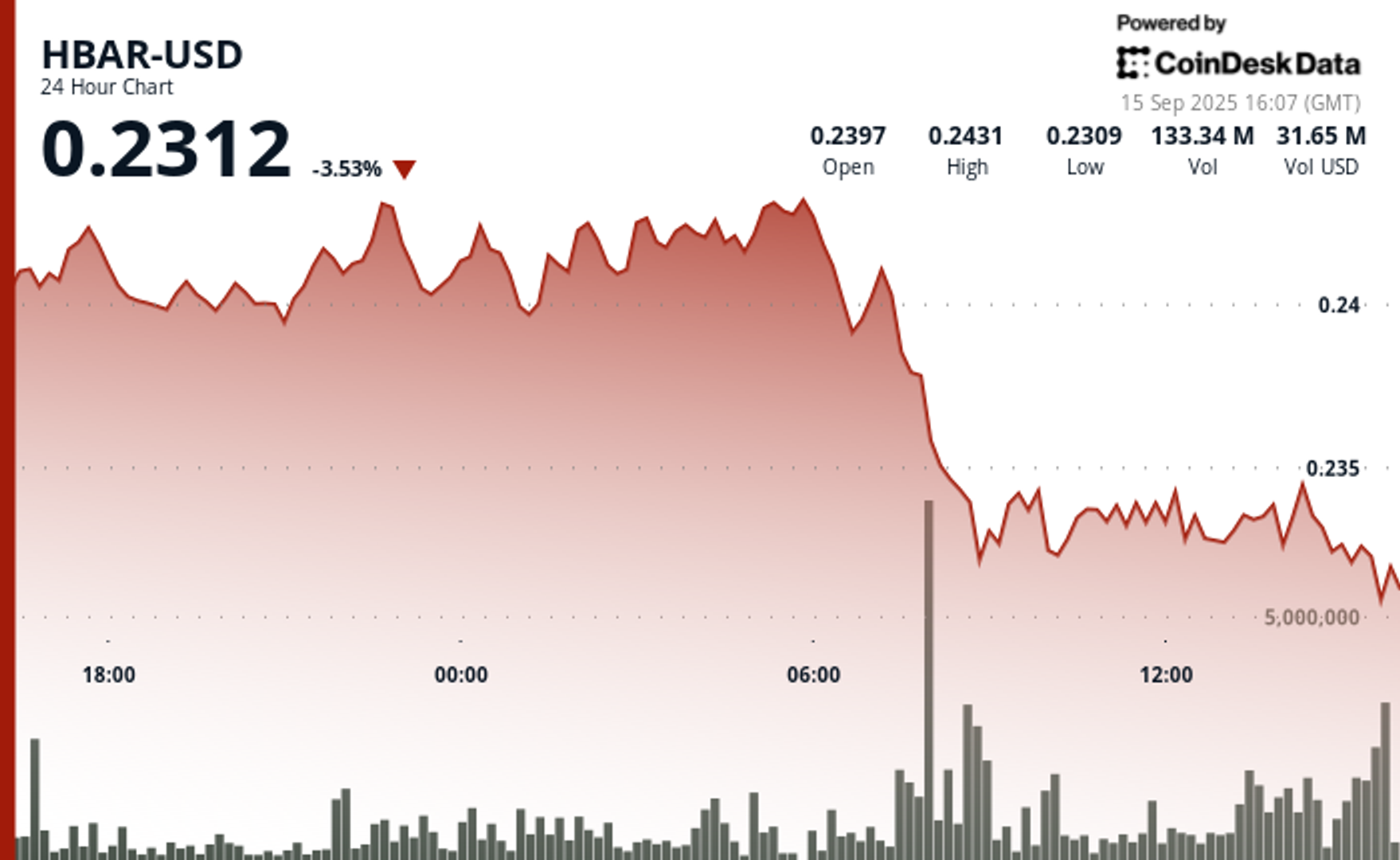

Hedera Hashgraph’s HBAR token endured steep losses over a volatile 24-hour window between September 14 and 15, falling 5% from $0.24 to $0.23. The token’s trading range expanded by $0.01 — a move often linked to outsized institutional activity — as heavy corporate selling overwhelmed support levels. The sharpest move came between 07:00 and 08:00 UTC on September 15, when concentrated liquidation drove prices lower after days of resistance around $0.24.

Institutional trading volumes surged during the session, with more than 126 million tokens changing hands on the morning of September 15 — nearly three times the norm for corporate flows. Market participants attributed the spike to portfolio rebalancing by large stakeholders, with enterprise adoption jitters and mounting regulatory scrutiny providing the backdrop for the selloff.

Recovery efforts briefly emerged during the final hour of trading, when corporate buyers tested the $0.24 level before retreating. Between 13:32 and 13:35 UTC, one accumulation push saw 2.47 million tokens deployed in an effort to establish a price floor. Still, buying momentum ultimately faltered, with HBAR settling back into support at $0.23.

The turbulence underscores the token’s vulnerability to institutional distribution events. Analysts point to the failed breakout above $0.24 as confirmation of fresh resistance, with $0.23 now serving as the critical support zone. The surge in volume suggests major corporate participants are repositioning ahead of regulatory shifts, leaving HBAR’s near-term outlook dependent on whether enterprise buyers can mount sustained defenses above key support.

")

Technical Indicators Summary

- Corporate resistance levels crystallized at $0.24 where institutional selling pressure consistently overwhelmed enterprise buying interest across multiple trading sessions.

- Institutional support structures emerged around $0.23 levels where corporate buying programs have systematically absorbed selling pressure from retail and smaller institutional participants.

- The unprecedented trading volume surge to 126.38 million tokens during the 08:00 morning session reflects enterprise-scale distribution strategies that overwhelmed corporate demand across major trading platforms.

- Subsequent institutional momentum proved unsustainable as systematic selling pressure resumed between 13:37-13:44, driving corporate participants back toward $0.23 support zones with sustained volumes exceeding 1 million tokens, indicating ongoing institutional distribution.

- Final trading periods exhibited diminishing corporate activity with zero recorded volume between 13:13-14:14, suggesting institutional participants adopted defensive positioning strategies as HBAR consolidated at $0.23 amid enterprise uncertainty.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

Wall Street Bank Citigroup Sees Ether Falling to $4,300 by Year-End

XLM Sees Heavy Volatility as Institutional Selling Weighs on Price

HBAR Tumbles 5% as Institutional Investors Trigger Mass Selloff

-

Business11 месяцев ago

Business11 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion11 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment11 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment11 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment11 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Business11 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment11 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton

-

Entertainment11 месяцев ago

Disney\’s live-action Aladdin finally finds its stars