Uncategorized

Right to Code? Tornado Cash Dev Roman Storm’s Money Laundering Trial Kicks Off Monday

NEW YORK, New York — Tornado Cash developer Roman Storm’s criminal money laundering is slated to begin in Manhattan on Monday morning, when Storm’s lawyers and prosecutors will begin to select a jury to oversee Storm’s four-week trial.

Storm was arrested in Washington state in 2023 and charged with conspiracy to commit money laundering, conspiracy to violate U.S. sanctions, and conspiracy to operate an unlicensed money transmitting business — charges which, if Storm is convicted, carry a maximum combined sentence of 45 years in prison. Storm’s fellow Tornado Cash developer, Russian national Roman Semenov, faces the same charges but remains at large. Another developer, Alexey Pertsev, was convicted of money laundering in the Netherlands in 2024 and sentenced to five years in prison, which he is currently appealing.

At the heart of Storm’s case lies Tornado Cash, a privacy-oriented cryptocurrency mixing service, which the government has alleged was used to launder over $1 billion in criminal proceeds by bad actors — including the Lazarus Group, North Korea’s state-sanctioned hacking operation, which they say constituted a violation of U.S. sanctions — while Storm and his colleagues turned a blind eye. Storm’s lawyers, meanwhile, have argued that he was simply a developer of open-source, decentralized software with legitimate, privacy-preserving uses who should not be held responsible for bad actors’ use of it.

“There’s certainly going to be a very vigorous defense here that they were writing code and that [Tornado Cash] was designed for privacy — that some people may have taken advantage of it, but [Storm and his colleagues] weren’t co-conspirators,” said Mark Bini, a partner in Reed Smith’s global regulatory and enforcement practice group. “Mixers have been very controversial because they’ve been used by lots of people doing bad things, no doubt about it, but the idea that some people would want to use them for privacy, that’s a legitimate argument as well. That’s going to make for a fierce battle here.”

Storm’s trial has drawn the attention of many in the crypto industry, who have raised concerns that, if Storm is found guilty, it could mean that developers down the line are on the hook for how people use their programs — something that could have devastating consequences for both the availability of privacy tools and the decentralized finance (DeFi) space as a whole. A host of major players in the industry, including investment firm Paradigm, and non-profit advocacy groups Coin Center and the DeFi Education Fund, have submitted amicus briefs in Storm’s defense.

Others, however, have been more reluctant to accept Storm’s privacy defense. Economics writer J.P. Koenig wrote in a 2024 blog post that, if Storm prevails at trial, it could «potentially mean that anyone who wants to facilitate illegal activities would have a strong incentive to copy Tornado Cash, effectively turning their operation into a ‘golem’ — a deathless artificial being run on smart contracts — and then throwing away the keys to avoid the law.”

Swiss blockchain analytics firm Global Ledger wrote in a blog post that there are, in general, “far more reasons why cyber criminals might want to use a mixing service than developers who legitimately want to obfuscate the movement of their personal funds.”

Shifting winds

Storm’s trial begins as the U.S. government continues to overhaul its approach to the crypto industry — particuarly crypto regulation. Under U.S. President Donald Trump, the White House has taken a friendlier stance towards the industry (which poured a whopping $130 million into congressional races in the 2024 elections and at least $18 million into Trump’s inaugural committee alone), nudging regulators and law enforcement to do the same.

Since Trump took office in January, the U.S. Securities and Exchange Commission — which had taken on a bogeyman-like status under former Chair Gary Gensler for its so-called practice of “regulation by enforcement» — has formed an industry-friendly Crypto Task Force and dropped a slew of open cases and investigations into crypto companies. In an April memo to staff, Deputy Attorney General Todd Blanche ordered U.S. Department of Justice (DOJ) staff to “narrow” their focus on crypto crime, instructing them that the agency would no longer be charging regulatory violations in cases involving crypto.

Though some speculated that prosecutors would back down from their case against Storm in the wake of Blanche’s memo, the government pressed forward, dropping just one part of one charge. Prosecutors also opted to continue with their case against Storm in March after the U.S. Treasury Department’s Office of Foreign Asset Control (OFAC) delisted Tornado Cash from their list of sanctioned entities, after a federal judge ruled that the agency could not sanction a smart contract.

“Frankly, I was kind of surprised it was going forward after we saw that [Tornado Cash] was taken off the OFAC list,” Bini said. “We don’t know the government’s evidence yet, but we’ve seen the Trump Administration really move away from these sort of regulatory-type cases. And this seems like one that is on the edges of that because the conspiracy to operate an unlicensed money transmitting business [charge] does seem like the type of regulatory case that perhaps the Administration is getting out of the business of.”

Storm on trial

During a pre-trial conference last week, District Judge Katherine Polk Failla of the Southern District of New York (SDNY) ruled that neither side could bring up the OFAC sanctions — either that Tornado Cash was sanctioned in the first place or that the sanctions were subsequently removed — during Storm’s trial, arguing that it would confuse the jury. Failla also ruled that neither party could mention the outcome of a related civil case, Van Loon vs. Department of the Treasury.

Bini told CoinDesk that Failla’s ruling to keep the OFAC sanctions out of the trial is likely to help the government’s case more than Storm’s.

If the defense was able to tell the jury that OFAC’s sanctions were later dropped, Bini said, “I think you’re more likely to have jurors say ‘gosh, I’m not sure of whether this is illegal or not.’ And if they’re not sure, well, then the defendant is not guilty. I think that ruling probably helped the government to some extent in making the case seem cleaner and less complicated.”

Bini said that, if the trial results in a conviction, Failla’s ruling presents potential grounds for Storm’s lawyers to appeal.

“The defense may say, ‘hey, we should have had the right to present that to the jury, we think that’s important evidence,’” he said. “This is the type of case where even if the government gets a conviction as they usually do, there really may be some legal infirmities.”

If the jury finds Storm guilty, Bini said that there might be another option beyond an appeal — a presidential pardon. Trump has pardoned a number of people in the crypto industry since taking office in January, including the co-founders of BitMEX and Silk Road founder Ross Ulbricht.

“Let’s say it results in a conviction, that doesn’t mean that the President might not get involved afterwards,” Bini said. “That’s a bit of a wild card that we could see play out here if the case results in a conviction.”

In a final pre-trial conference on Friday, Storm’s lawyers made a last-ditch effort to get the case dismissed after the government revealed that its theory of venue (basically, the prosecution’s justification to bring the case in the Southern District of New York) hinged on three pieces of evidence — Storm’s texts to a New York-based venture capitalist, Storm’s interview with a New York-based Bloomberg reporter and the fact that a hacker accessed Tornado Cash from New York.

Failla ultimately ruled against the defense’s motion, allowing the government’s case against Storm to proceed to trial.

The next four weeks

Storm’s trial, initially slated for two weeks, is expected to run a full month due to the sheer number of witnesses in the case. The government alone told the court it planned to call more than 20 people to testify, including a hacker who used Tornado Cash, a so-called “victim” witness and a host of expert witnesses.

Jury selection is expected to take two days, with opening arguments likely slated for Wednesday.

Storm has not yet indicated either way whether he will testify in his own defense, but Bini said it could be a big help for his defense.

“I think there’s a really good chance [Storm] will testify. If so, [he’s] going to have to withstand some really stiff cross [examination], but that could be really powerful in a case like this,” Bini said. “The burden is on the government, not the [defense], but they might want to take the stand and tell the jury their story.”

Good Morning, Asia. Here’s what’s making news in the markets:

Welcome to Asia Morning Briefing, a daily summary of top stories during U.S. hours and an overview of market moves and analysis. For a detailed overview of U.S. markets, see CoinDesk’s Crypto Daybook Americas.

Bitcoin (BTC) traded just above $115k in Asia Tuesday morning, slipping slightly after a strong start to the week.

The modest pullback followed a run of inflows into U.S. spot ETFs and lingering optimism that the Federal Reserve will cut rates next week. The moves left traders divided: is this recovery built on fragile foundations, or is crypto firmly back on track after last week’s CPI-driven jitters?

That debate is playing out across research desks. Glassnode’s weekly pulse emphasizes fragility. While ETF inflows surged nearly 200% last week and futures open interest jumped, the underlying spot market looks weak.

Buying conviction remains shallow, Glassnode writes, funding rates have softened, and profit-taking is on the rise with more than 92% of supply in profit.

Options traders have also scaled back downside hedges, pushing volatility spreads lower, which Glassnode warns leaves the market exposed if risk returns. The core message: ETFs and futures are supporting the rally, but without stronger spot flows, BTC remains vulnerable.

QCP takes the other side.

The Singapore-based desk says crypto is “back on track” after CPI confirmed tariff-led inflation without major surprises. They highlight five consecutive days of sizeable BTC ETF inflows, ETH’s biggest inflow in two weeks, and strength in XRP and SOL even after ETF delays.

Traders, they argue, are interpreting regulatory postponements as inevitability rather than rejection. With the Altcoin Season Index at a 90-day high, QCP sees BTC consolidation above $115k as the launchpad for rotation into higher-beta assets.

The divide underscores how Bitcoin’s current range near $115k–$116k is a battleground. Glassnode calls it fragile optimism; QCP calls it momentum. Which side is right may depend on whether ETF inflows keep offsetting profit-taking in the weeks ahead.

")

Market Movement

BTC: Bitcoin is consolidating near the $115,000 level as traders square positions ahead of expected U.S. Fed policy moves; institutional demand via spot Bitcoin ETFs is supporting upside

ETH: ETH is trading near $4500 in a key resistance band; gains are being helped by renewed institutional demand, tightening supply (exchange outflows), and positive technical setups.

Gold: Gold continues to hold near record highs, underpinned by expectations of Fed interest rate cuts, inflation risk, and investor demand for safe havens; gains tempered somewhat by profit‑taking and a firmer U.S. dollar

Nikkei 225: Japan’s Nikkei 225 topped 45,000 for the first time Monday, leading Asia-Pacific gains as upbeat U.S.-China trade talks and a TikTok divestment framework lifted sentiment.

S&P 500: The S&P 500 rose 0.5% to close above 6,600 for the first time on Monday as upbeat U.S.-China trade talks and anticipation of a Fed meeting lifted stocks.

Elsewhere in Crypto

Wall Street giant Citigroup (C) has launched new ether (ETH) forecasts, calling for $4,300 by year-end, which would be a decline from the current $4,515.

That’s the base case though. The bank’s full assessment is wide enough to drive an army regiment through, with the bull case being $6,400 and the bear case $2,200.

The bank analysts said network activity remains the key driver of ether’s value, but much of the recent growth has been on layer-2s, where value “pass-through” to Ethereum’s base layer is unclear.

Citi assumes just 30% of layer-2 activity contributes to ether’s valuation, putting current prices above its activity-based model, likely due to strong inflows and excitement around tokenization and stablecoins.

A layer 1 network is the base layer, or the underlying infrastructure of a blockchain. Layer 2 refers to a set of off-chain systems or separate blockchains built on top of layer 1s.

Exchange-traded fund (ETF) flows, though smaller than bitcoin’s (BTC), have a bigger price impact per dollar, but Citi expects them to remain limited given ether’s smaller market cap and lower visibility with new investors.

Macro factors are seen adding only modest support. With equities already near the bank’s S&P 500 6,600 target, the analysts do not expect major upside from risk assets.

Read more: Ether Bigger Beneficiary of Digital Asset Treasuries Than Bitcoin or Solana: StanChart

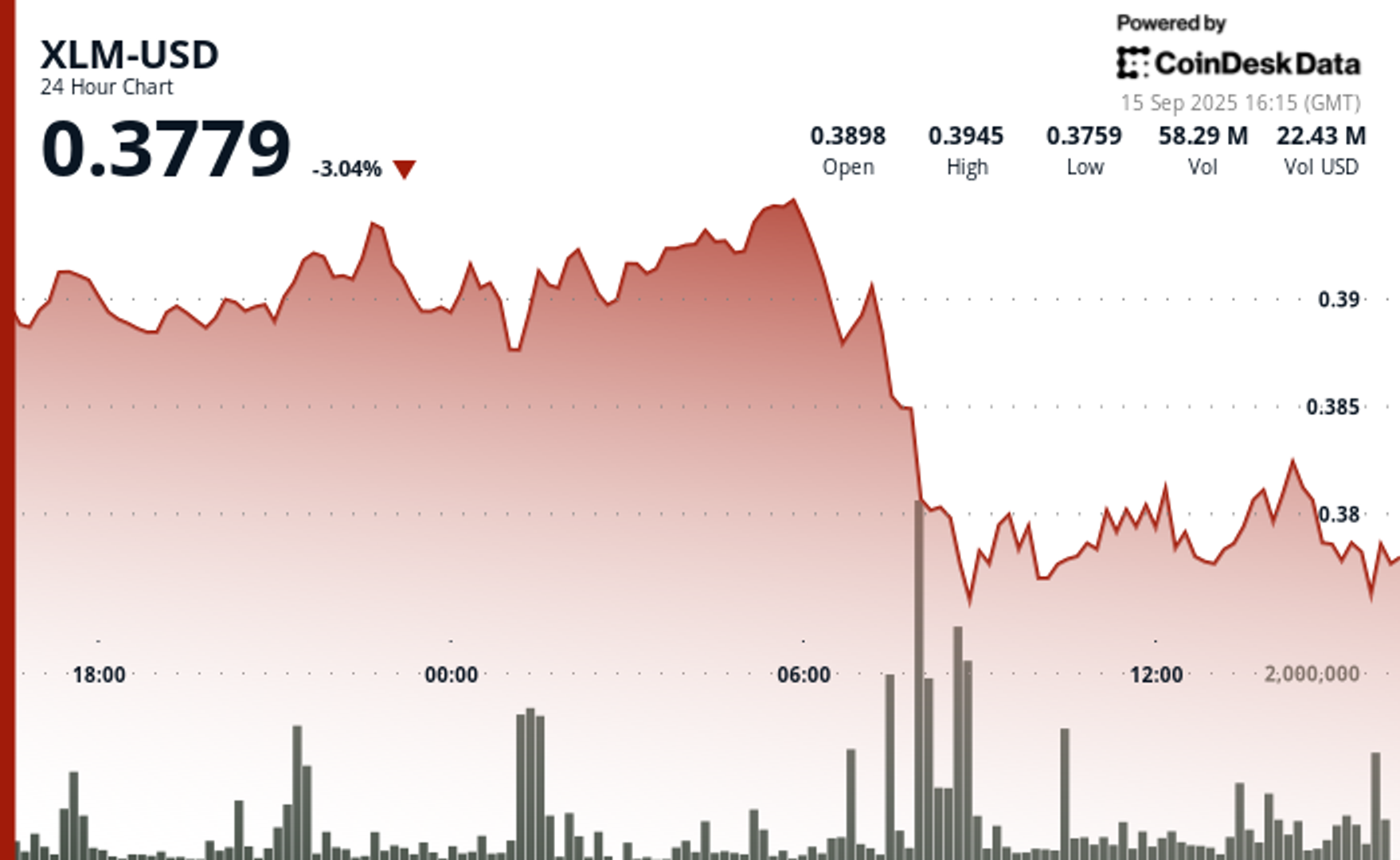

Stellar’s XLM token endured sharp swings over the past 24 hours, tumbling 3% as institutional selling pressure dominated order books. The asset declined from $0.39 to $0.38 between September 14 at 15:00 and September 15 at 14:00, with trading volumes peaking at 101.32 million—nearly triple its 24-hour average. The heaviest liquidation struck during the morning hours of September 15, when XLM collapsed from $0.395 to $0.376 within two hours, establishing $0.395 as firm resistance while tentative support formed near $0.375.

Despite the broader downtrend, intraday action highlighted moments of resilience. From 13:15 to 14:14 on September 15, XLM staged a brief recovery, jumping from $0.378 to a session high of $0.383 before closing the hour at $0.380. Trading volume surged above 10 million units during this window, with 3.45 million changing hands in a single minute as bulls attempted to push past resistance. While sellers capped momentum, the consolidation zone around $0.380–$0.381 now represents a potential support base.

Market dynamics suggest distribution patterns consistent with institutional profit-taking. The persistent supply overhead has reinforced resistance at $0.395, where repeated rally attempts have failed, while the emergence of support near $0.375 reflects opportunistic buying during liquidation waves. For traders, the $0.375–$0.395 band has become the key battleground that will define near-term direction.

")

Technical Indicators

- XLM retreated 3% from $0.39 to $0.38 during the previous 24-hours from 14 September 15:00 to 15 September 14:00.

- Trading volume peaked at 101.32 million during the 08:00 hour, nearly triple the 24-hour average of 24.47 million.

- Strong resistance established around $0.395 level during morning selloff.

- Key support emerged near $0.375 where buying interest materialized.

- Price range of $0.019 representing 5% volatility between peak and trough.

- Recovery attempts reached $0.383 by 13:00 before encountering selling pressure.

- Consolidation pattern formed around $0.380-$0.381 zone suggesting new support level.

Disclaimer: Parts of this article were generated with the assistance from AI tools and reviewed by our editorial team to ensure accuracy and adherence to our standards. For more information, see CoinDesk’s full AI Policy.

Asia Morning Briefing: Fragility or Back on Track? BTC Holds the Line at $115K

Wall Street Bank Citigroup Sees Ether Falling to $4,300 by Year-End

XLM Sees Heavy Volatility as Institutional Selling Weighs on Price

-

Business11 месяцев ago

Business11 месяцев ago3 Ways to make your business presentation more relatable

-

Fashion11 месяцев ago

According to Dior Couture, this taboo fashion accessory is back

-

Entertainment11 месяцев ago

10 Artists who retired from music and made a comeback

-

Entertainment11 месяцев ago

\’Better Call Saul\’ has been renewed for a fourth season

-

Entertainment11 месяцев ago

New Season 8 Walking Dead trailer flashes forward in time

-

Business11 месяцев ago

15 Habits that could be hurting your business relationships

-

Entertainment11 месяцев ago

Meet Superman\’s grandfather in new trailer for Krypton

-

Entertainment11 месяцев ago

Disney\’s live-action Aladdin finally finds its stars